Second Quarter 2025

Inland Empire’s Industrial Market Cools in Q2 as Vacancy Climbs to 8.4%

Vacancy is rising, leasing and sales activity remain sluggish, and construction is slowing—pointing to a sustained market reset underway in 2025.

Developers pull back as rent growth stalls, while buyers remain selective in the face of elevated availability and interest rates.

MARKET OVERVIEW

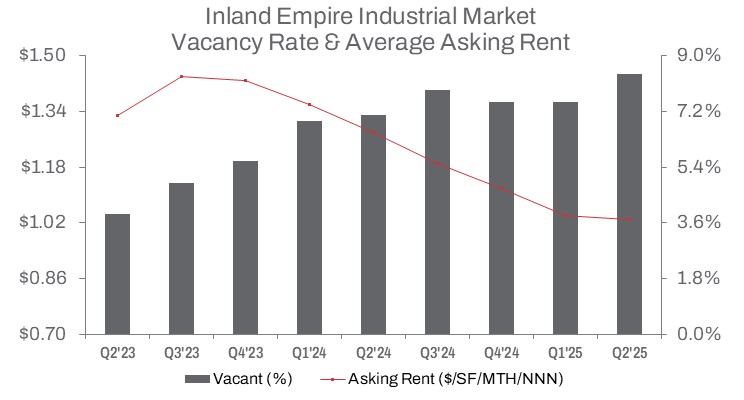

In Q2 2025, the industrial vacancy rate in the Inland Empire rose to 8.4%, up 90 basis points from the previous quarter and 130 basis points year-over-year. Over the past two quarters, the market added approximately 5.3 million square feet of completed construction, while net absorption registered negative 1.4 million square feet—evidence of the continued shift in the region’s industrial trajectory.

Although the pace of completions declined 8.4% quarter-over-quarter, it marked a sharp 71.1% year-to-date drop compared to mid-year 2024, signaling a notable slowdown in construction starts as developers respond to softening demand. The pipeline of industrial space under construction also shrank, down 21.0% year-over-year.

The once-robust rent growth—previously a major driver of new development—has noticeably cooled. The average asking rent fell 19.5% year-over-year to $1.03/SF triple net in Q2 2025, holding steady from the previous quarter.

Sales volume in Q2 declined 13.2% from an already sluggish Q1. Year-to-date, volume was down 33.6% from the first half of 2024, totaling roughly 3.5 million square feet. Despite the slowdown, pricing held firm, with the average sale price per square foot rising 3.3% quarter-over-quarter to $270, up 5.2% year-over-year. The increase reflects investor focus on well-located, high-quality assets that continue to trade at a premium, even as broader market demand softens.

Leasing activity also slowed, with volume falling 32.7% quarter-over-quarter. At mid-year, total leasing reached approximately 28 million square feet—down 14.9% from the same period in 2024.

TRENDS TO WATCH

The Inland Empire industrial market is navigating a shift that presents both challenges and opportunities. Declining leasing and sales activity signals a cooling environment, but the growing availability of warehouse space—reaching 8.4% vacancy in Q2 2025—offers tenants greater flexibility to negotiate favorable lease terms or secure space for logistics and distribution needs.

Sublease space remains a notable opportunity. Total vacant sublease space reached 11.5 million square feet in Q2 2025, up 3.0% from Q1 but down 5.4% year-over-year from its mid-2024 peak. Companies seeking cost-effective, short-term solutions may benefit—particularly in the largest, high-demand submarkets such as the West and East Inland Empire.

Strong port activity continues to support logistics demand. Inbound cargo volumes at the Ports of Los Angeles and Long Beach increased 6.2% year-to-date through June 2025, sustaining the need for distribution centers to support e-commerce and retail supply chains. This trend favors occupiers looking for facilities near key transportation corridors.

Looking ahead, elevated interest rates are expected to keep downward pressure on sales activity and pricing through late 2025. Total sales dollar volume declined 14.8% from Q1 and is down 26.4% year-to-date compared to the first half of 2024. While median sale prices declined 3.5% year-over-year to $275/SF, premium assets in strategic locations continue to command strong pricing. Investors will closely watch for distressed or undervalued opportunities, especially in submarkets with robust infrastructure and access to major freeways.