Fourth Quarter 2025

The Inland Empire Industrial Market Navigates a Reset from Expansion to Equilibrium at Year-End 2025

While a sharp decline in new construction begins to stabilize vacancy, moderating rents and pricing adjustments create a strategic window for well-capitalized investors.

Inland Empire industrial vacancy dips to 8.9% as construction starts plummet 81.6%.

MARKET OVERVIEW

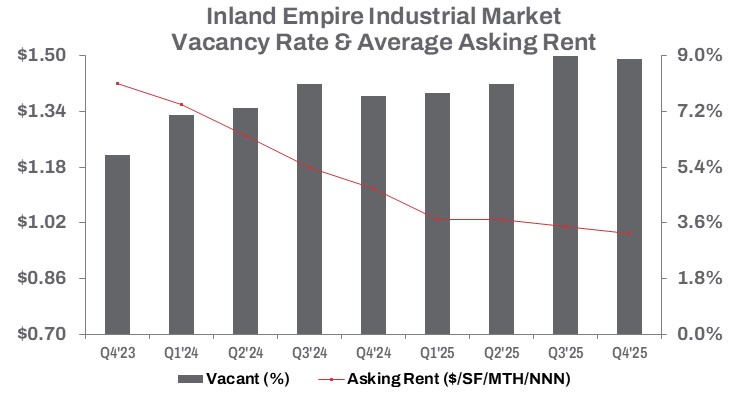

Brisk demand for industrial space in Q4 2025 pushed the Inland Empire’s vacancy rate down to 8.9%, a 10-basis-point decline quarter-over-quarter, though vacancy remained 120 basis points higher than the same period last year. Over the past four quarters, approximately 13.0 million square feet of completed construction entered the market, while net absorption, though positive, totaled about 2.5 million square feet, highlighting an ongoing supply–demand imbalance.

Completed construction declined sharply, falling 81.6% quarter-over-quarter and 50.9% year-to-date compared to Q4 2024, reflecting fewer new construction starts as warehouse demand moderates following the peak of e-commerce expansion. The volume of industrial space under construction also decreased 29.3% year-over-year. Rent growth, once a primary driver of development, continued to decelerate, with average asking rents in Q4 declining 2.0% quarter-over-quarter to $0.99 per square foot on a triple net basis, representing an 11.6% year-over-year decrease.

Sale volume increased 34.1% from Q3 2025 but declined 2.4% year-to-date compared to the same period in 2024, totaling approximately 10.1 million square feet by year-end. The average sale price fell 17.2% quarter-over-quarter to $207 per square foot, or 11.6% below last year’s level. Leasing activity slowed considerably, with quarterly leasing volume down 51.9% to approximately 8.2 million square feet. On a year-to-date basis, leasing volume declined 9.8% to 54.6 million square feet, signaling softer demand as the year concluded.

TRENDS TO WATCH

Shrinking lease and sale velocity continues to challenge transaction momentum, but expanding warehouse availability is creating selective opportunities for both tenants and investors. Sublease availability has eased, with newly vacated space declining 4.8% from Q3 2025, bringing total sublease inventory to approximately 9.6 million square feet. While still elevated, this represents the lowest level in two years and suggests excess space is gradually being absorbed.

Port activity remains a stabilizing force. Combined cargo volumes at the Ports of Los Angeles and Long Beach increased 0.1% in 2025, underscoring steady logistics demand that supports long-term fundamentals in the Inland Empire, even as near-term space availability remains abundant.

On the capital markets side, higher interest rates and moderating demand are driving continued repricing. Sales dollar volume rose 15.8% quarter-over-quarter in Q4, while year-to-date volume totaled $2.3 billion, down 18.6% from 2024. The median sale price declined to $242 per square foot, reflecting a 6.3% quarter-over-quarter decrease and a modest 1.2% year-over-year decline. Compared to Q4 2023, pricing was down 8.4%, confirming that valuation adjustments remain underway.

Industrial cap rates in the Inland Empire averaged 4.6% in Q4 2025, compressing sharply from 5.7% in Q3 2025 and settling 30 basis points below the 4.9% recorded in Q4 2024. This quarter-over-quarter compression reflects selective investor demand for stabilized, high-quality assets, even as broader transaction activity remains constrained by financing costs and softer fundamentals.

Looking ahead, pricing pressure is expected to persist into the first half of 2026. However, as construction slows and fundamentals gradually rebalance, the current environment may favor well-capitalized buyers positioned to navigate the reset and pursue quality assets at more defensible pricing.