Third Quarter 2024

Inland Empire Multifamily Market Adjusts Rents With New Inventory Expansion

Vacancies Rise as New Deliveries Accelerate, While Sales Activity Gains Momentum in a Shifting Economic Landscape.

Investors are recalibrating their strategies to balance the impact of borrowing costs with the heightened demand for rental housing.

MARKET OVERVIEW

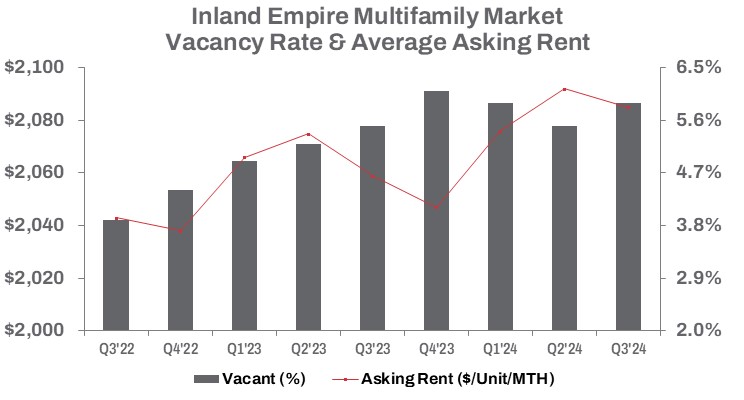

In Q3 2024, the Inland Empire’s multifamily housing market exhibited shifting dynamics. Vacant units rose by 6.9% quarter-over-quarter and 9.1% year-over-year, totaling 13,872 units. Developers added 1,778 new units during the quarter, significantly higher than the 623 units delivered in the prior quarter and up from 762 units in Q3 2023. Year-to-date, 3,101 units were delivered—a 63.0% increase compared to the same period in 2023—underscoring the accelerated pace of inventory expansion. This growth has contributed to a vacancy rate of 5.8%, up 30 basis points both quarter-over-quarter and year-over-year.

Average asking rents declined slightly by 0.3% quarter-over-quarter but increased by 1.3% year-over-year, reaching $2,085 per unit. This represents a decline from last quarter’s all-time high. Moderated rent growth is driven by competition for tenant demand, while elevated interest rates and construction costs have slowed new development activity. As of Q3 2024, 6,876 units were under construction—a sharp 16.3% decrease quarter-over-quarter and 31.9% year-over-year.

Sales activity painted a mixed picture. Transaction volume more than doubled quarter-over-quarter, driving year-to-date sales volume to $783 million—a 40.3% increase compared to the prior year’s low. The average sale price per unit rose by 14.7% year-over-year to $233,738. Regionwide, the total number of units sold year-to-date surged 93.5% compared to the same period in 2023. However, the average capitalization rate dropped by 30 basis points year-over-year to 5.3%.

These trends reflect a multifaceted market, where increasing vacancies and slowing construction contrast with moderated rent growth and improving sales performance.

TRENDS TO WATCH

The Inland Empire’s multifamily market fundamentals are expected to remain strong, adapting to economic shifts, employment trends, and the ongoing challenge of homeownership affordability. These factors continue to drive rental market growth, while investment sales have gained momentum. Although rising borrowing costs have increased financial risks, demand persists in select asset classes, with growth prospects particularly pronounced in the Inland Empire.

In Q3 2024, the market recorded six sales of properties with over 100 units. The largest transaction was The Ashton Apartments, a 492-unit complex at 2178 Stoneridge Drive in Corona, within the Riverside submarket. The property sold for $136.5 million in September, equating to $277,439 per unit for an asset built in 1986. The average monthly asking rent per unit is $2,243, representing a 5.8% premium over the average asking rent in the Riverside submarket.

Investors are recalibrating their strategies to balance the impact of borrowing costs with the heightened demand for rental housing. This shift is evident in average deal sizes, which rose to $10,757,052 in Q3 2024—a 50.1% increase from the previous quarter and a 34.1% rise year-over-year.

Looking ahead, the multifamily housing market will continue to adapt to broader economic conditions and mortgage rate trends. With mortgage rates near their highest levels since 2002 and home prices climbing, homeownership remains out of reach for many borrowers, further sustaining demand in the rental market. However, slower rent growth is expected to influence pricing as investors adjust to evolving market realities.