Third Quarter 2025

Inland Empire Multifamily Market Balances Slowing Development with a Strong Rebound in Investment Sales in Q3 2025

Vacancy tightens, construction activity cools, and investor demand accelerates as the region’s long-term rental fundamentals remain resilient.

A shrinking pipeline, steady demand, and rising sales volume define the Inland Empire’s multifamily market in Q3 2025.

MARKET OVERVIEW

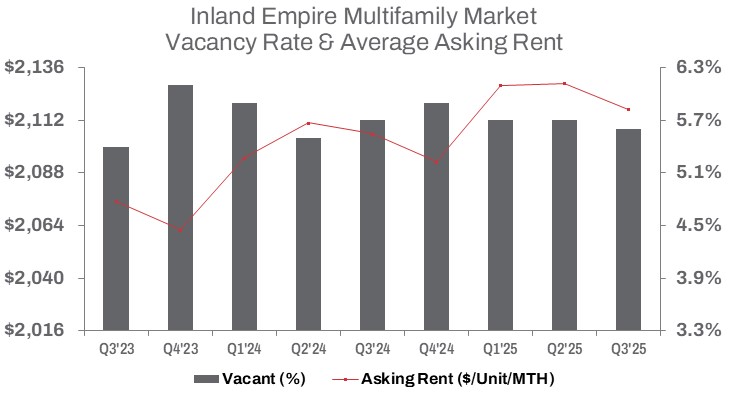

In Q3 2025, the Inland Empire’s multifamily housing market presented a dynamic environment, characterized by a strong rebound in investment sales and a contraction in the development pipeline. Vacant units fell 1.6% quarter-over-quarter but posted a modest 0.7% increase year-over-year, totaling 13,530 units. This reduction helped stabilize the market, with the vacancy rate decreasing by 10 basis points both quarter-over-quarter and year-over-year to settle at 5.6%.

Developers delivered 545 new units during the quarter, a sharp reduction from the 1,414 units delivered in the prior quarter and the 1,929 units delivered in Q3 2024. Year-to-date, deliveries reached 3,379 units, representing only a 0.8% increase from the same period in 2024, signaling a sustained but slowing pace of inventory expansion as the cooling pipeline continues to temper future supply.

Average asking rents declined slightly by 0.6% quarter-over-quarter but posted a modest 0.5% year-over-year increase, reaching $2,117 per unit. This moderated growth reflects increased competition for tenants. Elevated interest rates and construction costs continue to weigh on development activity. As of Q3 2025, 4,536 units were under construction, a notable 10.7% decrease quarter-over-quarter and a significant 41.6% decline year-over-year.

Sales activity rebounded sharply, underscoring renewed investor appetite. Transaction volume more than doubled quarter-over-quarter, up 130.2%, pushing year-to-date sales volume to $913.17 million, a substantial 14.2% increase compared to the same period in 2024. The average sale price per unit rose 32.9% year-over-year to $289,829. Regionwide, the total number of units sold year-to-date increased 5.0% from the same period in 2024. Meanwhile, the average capitalization rate rose 60 basis points year-over-year to 6.0%, reflecting the continued influence of higher borrowing costs on pricing and return expectations.

Together, these trends point to a multifaceted market, where a constricting development pipeline and stable vacancy conditions contrast with robust gains in sales volume and pricing, signaling improved investor sentiment toward the Inland Empire’s long-term fundamentals.

TRENDS TO WATCH

The Inland Empire’s multifamily fundamentals are expected to remain resilient, adapting to macroeconomic shifts, employment patterns, and the ongoing challenge of homeownership affordability. These structural forces continue to support rental demand, even as elevated borrowing costs introduce greater financial caution. Investor interest persists, particularly for high-quality and well-located assets.

In Q3 2025, sales activity was driven by larger, institutionally attractive transactions, including the sale of newly constructed and townhome-style properties.

A standout example is the sale of The Venue at Orange, a 328-unit apartment community located at 1610 Orange Avenue in Redlands. LuxView Properties LLC and Essex Property Trust sold the property to Sentinel Real Estate Corporation for $148.4 million, or $452,439 per unit. The asset’s appeal is reinforced by strong local demographics: within a three-mile radius, the population totals 79,050 across 28,648 households, with a median age of 37 and a median household income of $92,268. Additionally, 42,804 daytime employees within the same radius highlight the employment-driven demand supporting the San Bernardino submarket.

Another notable transaction was the sale of the Ontario Town Square Townhomes, where MG Properties sold 140 large-format townhome units to Green Lead Capital Partners for $60.5 million, or $432,142 per unit. The buyer was drawn to the exceptionally spacious floor plans, which average 1,494 square feet and are the largest in Ontario, as well as the community’s proximity to major employment centers and the suburban-style amenities of the West Inland Empire.

As investors recalibrate strategies to balance borrowing costs with demand for rental housing, rising cap rates reflect the need for higher yields to offset elevated financing and operating expenses.

Looking ahead, the Inland Empire’s multifamily market will continue adjusting to broader economic conditions and mortgage rate trends. With homeownership remaining out of reach for many prospective buyers, rental demand is expected to remain strong. Meanwhile, the slowdown in new deliveries and the steep decline in units under construction will help ease competitive pressure on both occupancy and rents over the medium term as investors and developers adjust to evolving market conditions.