Fourth Quarter 2024

Inland Empire Multifamily Market Adjusts Rents With New Supply Growth

Vacancies rise as new deliveries accelerate, while sales activity gains momentum in a shifting economic landscape.

Slower rent growth could moderate pricing as investors navigate these evolving conditions.

MARKET OVERVIEW

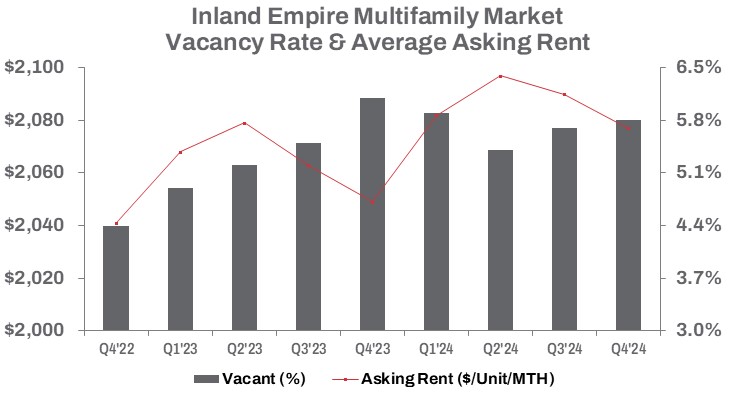

In Q4 2024, the Inland Empire’s multifamily housing market showed shifting trends. Vacant units rose 2.2% quarter-over-quarter but declined 3.4% year-over-year to 13,673 units. Developers added 728 new units during the quarter—down sharply from 2,255 units in Q3 but up from 483 units in Q4 2023. Year-to-date, 4,878 units were delivered, a 34.4% increase over the same period in 2023, highlighting an accelerated pace of inventory growth. This expansion pushed the vacancy rate to 5.7%, up 10 basis points from Q3 but down 40 basis points year-over-year.

Average asking rents dipped 0.6% quarter-over-quarter to $2,077 per unit but remained 1.4% higher year-over-year—a pullback from mid-2024’s all-time high. Moderated rent growth reflects heightened competition for tenants from newly completed apartments, while high interest rates and construction costs have curbed new development. As of Q4, 5,593 units were under construction, down 21.5% from the previous quarter and 38.2% year-over-year.

Sales activity presented a contrasting picture of the multifamily investment landscape. Transaction volume fell by nearly two-thirds quarter-over-quarter, yet year-to-date sales reached $962.2 million—a 52.2% increase from 2023’s low base. The average sale price per unit declined 6.3% from Q3 to $245,296, while the total number of units sold year-to-date surged 34.4% compared to 2023. Meanwhile, the average capitalization rate rose 50 basis points year-over-year to 5.5%.

These trends illustrate a shifting market—rising vacancies and slowing construction contrast with tempered rent growth and a resilient, albeit uneven, sales rebound.

TRENDS TO WATCH

How will the Inland Empire’s multifamily market fare as it navigates rising costs and shifting economics? Market fundamentals are expected to stay strong, adapting to economic changes, employment trends, and the persistent challenge of homeownership affordability. These forces continue to fuel rental market growth, while investment sales gain traction. Despite higher borrowing costs elevating financial risks, demand persists in select asset classes, with growth prospects especially robust in the Inland Empire.

In 2024, the market saw five sales of properties with over 200 units, up from three in 2023. Yet, the average deal size fell to $6,592,819, down 11.3% year-over-year—a decline likely tied to fewer high-value transactions as borrowing costs remain elevated. The Fed’s decision to hold interest rates steady suggests deal sizes may shrink further.

The demand for workforce-affordable housing is exemplified by one of Q4’s standout deals. Sagard Real Estate, Western National Group, and ArrowMark Partners acquired Vista Imperio, a 158-unit garden-style multifamily property in Riverside, California, from Blackstone Inc. for $49,850,000, or $315,506 per unit. Built in 2005 on a nearly 8-acre site, the apartment community offers one- and two-bedroom units with private garages. Its prime location near major employment hubs—like the University of California, Riverside, Sycamore Canyon Business Park, and March Air Reserve Base—sealed its appeal.

Investors are recalibrating strategies to balance rising borrowing costs with surging rental demand. Looking ahead, the multifamily market will continue adapting to broader economic shifts and financing trends. With mortgage rates nearing their highest levels since 2002 and home prices still climbing, homeownership remains out of reach for many, sustaining robust rental demand. However, slower rent growth could moderate pricing as investors navigate these evolving conditions.