Third Quarter 2024

Inland Empire Office Market Recovery Gains Momentum

Rising Occupancy, Stable Rents, and Reduced Sublease Space Signal Market Stabilization as Economic Trends Evolve.

Employment sectors that drive office space demand are showing signs of growth.

MARKET OVERVIEW

The Inland Empire office market is showing signs of recovery, with broad-based tenant demand driving higher occupancy levels. Landlords are proactively stabilizing asking rents to capitalize on the improving market environment. This renewed tenant activity is steadily reducing surplus office space, fostering optimism for continued growth.

In Q3 2024, total vacant office space, including sublease space, declined by 265,069 square feet year-over-year, signaling a potential market rebound. Vacant sublease space alone saw a robust 7.0% drop from the previous year.

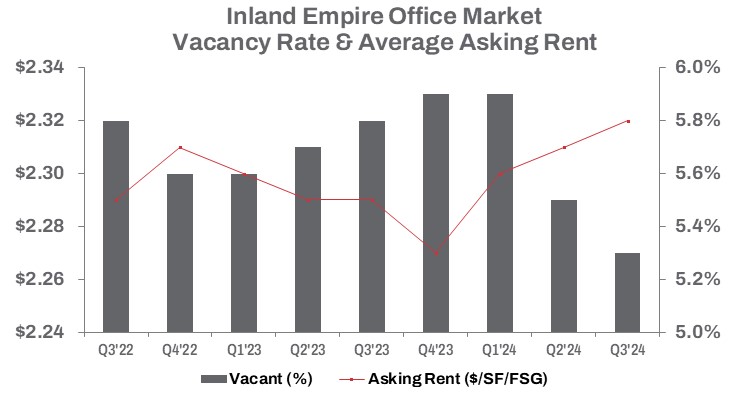

Vacancy rates have gradually improved throughout the second half of 2024, dropping by 50 basis points year-over-year to 5.3%. The stabilization of office vacancies has been supported by evolving remote work trends and shifting space utilization strategies. Since the economy reopened post-pandemic in Q3 2020, direct vacant office space has decreased by nearly 830,000 square feet, while occupied office space has grown, surpassing pre-pandemic levels by approximately 1.4 million square feet.

Vacant sublease space has seen a dramatic 52.9% reduction from pre-pandemic levels (approximately 84,000 square feet), reflecting the recovery trajectory of the office market, similar to trends seen post-Great Recession in 2013. This absorption has kept asking rents relatively stable, now at $2.32 per square foot on a full-service gross basis—up 1 cent quarter-over-quarter and 1.3% year-over-year. Leasing volume has also shown resilience, increasing 11.3% quarter-over-quarter and 9.4% year-to-date compared to the same period last year.

TRENDS TO WATCH

Tenants seeking value in buildings with vacant sublease space are facing limited opportunities. In Q3 2024, tenants subleased 8,629 square feet in the Inland Empire, a 16.1% decrease compared to the same period in 2023. The trend of offloading excess space through subleasing has diminished, with available sublease offerings dropping sharply by 12.8% quarter-over-quarter. This decline is particularly pronounced in the Riverside submarket, which experienced a 56.0% reduction in available sublease space, compared to a 40.3% decline in the South market.

As subleasing activity becomes more competitive, the average asking rent for sublease space in Q3 was $2.22 per square foot, offering only a 4.3% discount compared to direct lease space. With less sublease space available, sublessors appear less inclined to lower rents, particularly as much of the space has not been listed for extended periods.

Employment sectors that drive office space demand are showing signs of growth. According to September 2024 data from the California Employment Development Department, key sectors—including Professional and Business Services—continue to expand, despite a year-over-year increase in the Inland Empire’s unemployment rate. Over the past 12 months, Professional and Business Services—a key office-occupying sector—grew by 1.4% to 165,700 jobs. This growth serves as a stabilizing factor for office occupancy, bolstering demand.

Meanwhile, the average cap rate for office properties rose by 40 basis points year-over-year in Q3, reaching 6.8%. This increase contributed to a 23.4% decline in the average price per square foot of buildings sold, which fell to $171. However, total sales volume for the year through Q3 climbed by 20.9% to $242.2 million. Notably, the average size of buildings sold nearly doubled year-over-year, rising to 15,440 square feet. This trend reflects a shift toward larger transactions, which is expected to persist as the office market navigates its recovery phase.