Third Quarter 2025

Momentum Builds in Inland Empire’s Office Market in Q3 2025

Positive absorption, stable rents, and limited sublease space highlight a steady tightening market.

Cap rates rose to 8.0% in Q3 2025 while the median price per square foot fell 38.4% year over year, reflecting market recalibration.

MARKET OVERVIEW

The Inland Empire office market is showing clear signs of recovery, with broad-based tenant demand driving higher occupancy levels. Landlords are proactively stabilizing asking rents to capitalize on the improving environment. Renewed tenant activity is steadily reducing surplus office space, fostering optimism for continued growth.

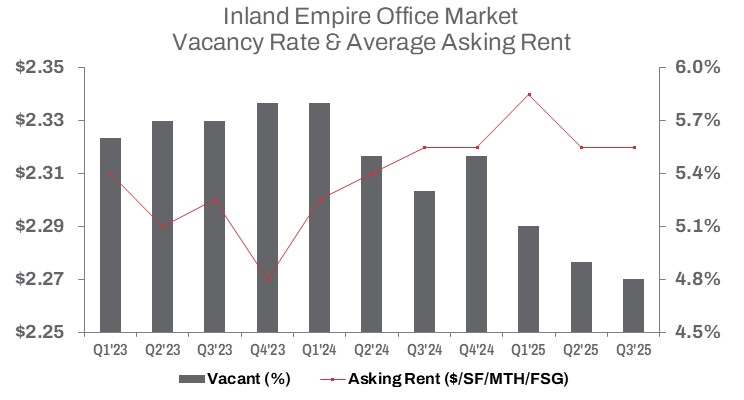

In Q3 2025, total vacant office space—including sublease space—declined by 332,726 square feet year over year, signaling the market’s rebound. This improvement pushed the overall vacancy rate down 80 basis points to 4.8%. The stabilization of office vacancies has been supported by evolving remote work trends and shifting space utilization strategies. Since the economy reopened post-pandemic, occupied office space has increased by nearly 1.7 million square feet, surpassing pre-pandemic levels from Q2 2020.

While total vacancy improved, sublease space saw a modest shift—down 0.8% from the prior quarter to 141,530 square feet—yet nearly double from last year, reflecting elevated caution among tenants shedding excess office space. However, compared to pre-pandemic levels (Q2 2020), vacant sublease space remains 17,199 square feet, or roughly 10.8%, below that benchmark.

Stabilization has helped keep asking rents firm. The average asking rent stands at $2.32 per square foot on a full-service gross basis—a level unchanged for the past year. However, leasing volume lost some momentum during the quarter, dipping 1.9% quarter over quarter. Year to date, leasing volume trails the same period last year by 21.3%, marking a cumulative slowdown in transactional activity.

TRENDS TO WATCH

Tenants seeking value in buildings with vacant sublease space are facing limited opportunities. In Q3 2025, tenants subleased 35,542 square feet in the Inland Empire year to date, a 117.7% increase compared to the same period in 2024. The trend of tenants picking up excess space through subleasing has accelerated, even as the pool of available sublease space has declined. This drop is particularly pronounced in the Riverside submarket, which saw a 61.4% reduction in available sublease space compared to a 43.8% decline in the West market. With fewer sublease options, sublessors appear less inclined to lower rents, particularly since much of the available space has not been listed for extended periods.

Employment sectors that drive office space demand are showing signs of contraction. Unemployment in the Inland Empire rose to 6.1% in August. Office-occupying sectors are underperforming. Due to the federal government shutdown, September employment figures are unavailable; the most recent data from the State of California Employment Development Department shows that Financial Activities lost 1,300 jobs, Real Estate and Rental and Leasing shed 700 jobs, and Professional and Business Services declined by 300 jobs. Core office-demand sectors have contracted year over year. Information sector employment, which includes a significant portion of tech jobs, fell by 300 positions over the past year. Overall, these sectors lost 2,600 jobs year over year. This slower job growth serves as a mitigating factor for office occupancy, tempering near-term demand.

Meanwhile, the average cap rate for office properties rose by 140 basis points year over year in Q3, reaching 8.0%. This increase contributed to a 38.4% decline in the median price per square foot of buildings sold, which fell to $152. Total sales volume through Q3 dropped 38.4% to $169.3 million. Notably, the average size of buildings sold decreased 21.4% year over year to 12,294 square feet, reflecting a shift toward smaller transactions—a trend expected to persist as the office market continues its recovery, signaling a bottoming-out phase.

The combination of modest rent adjustments, declining direct vacancy, and steady leasing activity has led to a 4.8% vacancy rate (above 95% occupancy), establishing the Inland Empire as a highly desirable, tightening market. This stability, coupled with the Inland Empire’s strong adaptation to workforce job growth, provides a strong base for continued business investment in the region.