Fourth Quarter 2024

Inland Empire Office Market Stable Despite Mixed Results in Q4 2024

Sales Growth and Reduced Sublease Space Highlight Market Adjustments.

The stabilization of office vacancies has been supported by evolving remote work trends and shifting space utilization strategies.

MARKET OVERVIEW

The Inland Empire office market continues to show signs of recovery, with broad-based tenant demand driving higher occupancy levels for vacant sublease space. While landlords are stabilizing asking rents to capitalize on the improving market environment, direct vacant space increased 2.3% quarter-over-quarter but declined 6.1% year-over-year. Vacant sublease space, on the other hand, saw a robust 8.6% decrease quarter-over-quarter and a 30.8% drop year-over-year. This renewed tenant activity is steadily reducing surplus office space, fostering optimism for continued growth.

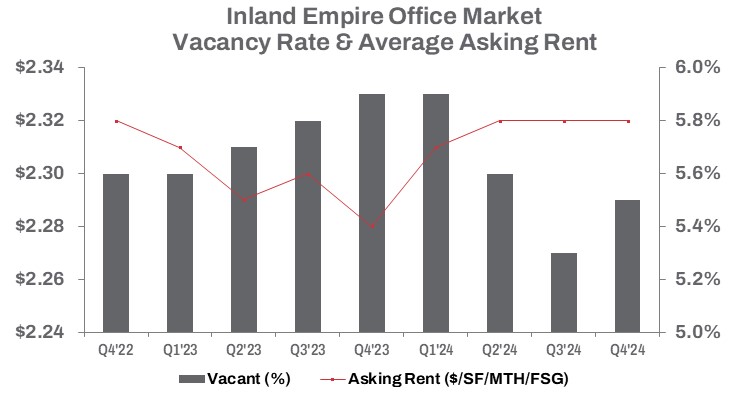

In Q4 2024, total vacant office space—driven by sublease activity—declined by 260,015 square feet year-over-year, signaling the ongoing market rebound. Although the vacancy rate ticked up 20 basis points quarter-over-quarter due to 80,119 square feet of direct office space coming on the market, it remains down 40 basis points compared to the same time last year.

The stabilization of office vacancies has been supported by evolving remote work trends and shifting space utilization strategies. Since the economy reopened at year-end 2020, direct vacant office space has decreased by 810,188 square feet, while occupied office space has grown, surpassing pre-pandemic levels by nearly 1.4 million square feet. Vacant sublease space has seen a dramatic 60.8% reduction from pre-pandemic levels, reflecting the office market’s recovery trajectory.

This absorption has kept asking rents stable quarter-over-quarter at $2.32 per square foot on a full-service gross basis—up 4 cents or 1.8% year-over-year. While leasing volume slowed in Q4, overall, 2024 leasing activity showed resilience, increasing 35.3% year-to-date compared to the same period last year.

TRENDS TO WATCH

Tenants seeking value in buildings with vacant sublease space are facing limited opportunities. In 2024, tenants subleased 31,918 square feet in the Inland Empire—a 38.4% increase compared to the same period in 2023. The trend of offloading excess space through subleasing has diminished, with available sublease offerings dropping sharply by 20.0% quarter-over-quarter. This decline was particularly pronounced in the Riverside submarket, which experienced a 56.6% reduction in available sublease space, compared to a 25.9% decline in the South market.

As subleasing activity becomes more competitive, the average asking rent for sublease space in Q4 was $2.22 per square foot, offering only a 4.3% discount compared to direct lease space. With less sublease space available, sublessors appear less inclined to lower rents, especially since much of the space has not been listed for extended periods.

The stabilization of the office market is driving activity on the sales side. The fourth quarter of 2024 reflected continued shifts, with a 30.7% year-to-date increase in square footage sold compared to the previous year, totaling approximately 540,000 square feet. Over the same period, the average sale price rose 1.4% year-over-year to $229 per square foot. The average building size sold also increased significantly by 25.0%, from 10,625 square feet in 2023 to 13,281 square feet in 2024. Sales volume grew 27.4%, closing the year at nearly $319 million. This quarter, the Citizens Business Bank corporate office and call center building at 9337 Milliken Ave. was sold in a sale-leaseback transaction, allowing the bank to unlock capital while continuing operations at the location. As market conditions evolve, other companies may explore similar strategies to enhance liquidity and operational flexibility.

This growth, despite elevated interest rates, suggests increasing confidence among owner/users and investors as they respond to a shifting office market. The rise in sales volume and average building size signals a market in transition, with investors refining acquisition criteria and viewing conditions as favorable for both buying and selling. These shifts underscore a period of adjustment as investors and tenants recalibrate their strategies to align with evolving market dynamics.