Fourth Quarter 2024

Inland Empire Retail Market Faced New Challenges in Q4 as Vacancy Rises and Economic Pressures Mount

Retail bankruptcies, rising costs, and shifting demand reshape the market as landlords adapt to a competitive landscape.

While landlords offer incentives to attract tenants, filling larger vacated spaces remains a challenge.

MARKET OVERVIEW

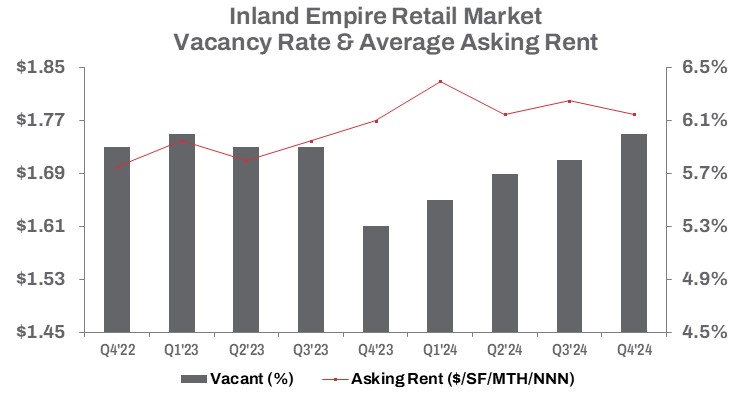

The Inland Empire retail market showed a mixed performance in late 2024 as the Federal Reserve kept interest rates steady, sustaining high borrowing costs for retailers and consumers in its ongoing push to tame inflation. In Q4 2024, vacancy rates rose to 6.0%, up 20 basis points from the prior quarter and 70 basis points year-over-year. Leasing activity declined 2.9% quarter-over-quarter but showed resilience year-to-date, increasing 7.4% from 2023 to nearly 3.5 million square feet.

A series of high-profile retail bankruptcies intensified challenges. Major retail chains—including TGI Friday’s, Denny’s, Ruby Tuesday, Rubio’s Coastal Grill, and Red Lobster—succumbed to declining revenues, escalating supply chain costs, and rising labor expenses, with Hooters of America exploring bankruptcy by year-end. California’s $20-per-hour minimum wage for fast-food workers, effective April 1, 2024, approached its one-year anniversary. This measure further strained quick-service and fast-casual operators, driving menu prices higher against persistent inflation and rising food costs, curbing consumer spending.

Despite navigating past the initial pandemic disruption, with approximately 3.5 million square feet occupied since Q4 2020, the Inland Empire retail market faced fresh headwinds in 2024. Total vacant retail space remained elevated, approaching 9.3 million square feet at year-end, as inflation and intensified competition constrained consumer spending at brick-and-mortar retail. This spurred landlords to continue offering concessions, while average asking rents held flat year-over-year at $1.78 per square foot triple net. Meanwhile, some investors pivoted to selling, boosting year-to-date sales volume by 27.1% from 2023 to over 4.1 million square feet.

Under rising operational costs, economic uncertainty, and an ongoing cost-of-living challenge, the Inland Empire retail market endured a turbulent 2024.

TRENDS TO WATCH

Landlords and sublessors will likely keep adjusting rents to boost cash flow and fill vacancies, especially as vacant sublease retail space dropped 11.6% year over year while direct availability climbed 15.3%. In this shifting landscape, the Riverside submarket—with 2.5 million square feet of available retail space, the highest in the region—slipped to second place in asking rent after a 2-cent quarter-over-quarter decline to $2.26 per square foot triple net. This drop aligned with 60,975 square feet of negative net absorption in Q4, pushing the submarket’s year-to-date negative absorption to 189,341 square feet and lifting the vacancy rate to 6.2%—a 60-basis-point rise from a year ago.

Meanwhile, the Airport submarket moved into the top spot for asking rent, rising 9.1% year over year to $2.28 per square foot triple net. Despite recording 67,368 square feet of negative net absorption in Q4, the submarket ended 2024 with a net positive absorption of 74,247 square feet. The vacancy rate ticked up 40 basis points to 3.4%—still the lowest in the region—amid a 39.9% year-over-year decline in sublease inventory. With limited sublease availability, the Airport submarket—home to Ontario Mills, Southern California’s premier outlet and value retail destination, and a key indicator of consumer spending resilience—continues to be a bellwether for Inland Empire retail.

These submarket shifts are unfolding against a backdrop of retailer upheavals and economic pressures. Craft and sewing retailer Joann, citing sluggish consumer demand and inventory shortages, is going out of business and closing all its stores following its second bankruptcy in less than a year. Liquidation sales will begin at all locations, underscoring the ongoing challenges brick-and-mortar retailers face. Joann’s closure affects eight Inland Empire locations, totaling 195,072 square feet.

Retail expansion will be focused on high-growth areas, with the South Inland Empire—Menifee, Perris, Wildomar, and Temecula—experiencing strong demand alongside new construction. This region accounts for 36.6% of the 473,079 square feet under development, primarily in Murrieta.

Landlords and tenants face increased competition. With prime retail space in high demand, competition for well-positioned properties is intensifying. While landlords offer incentives to attract tenants, filling larger vacated spaces remains a challenge.