Fourth Quarter 2025

Inland Empire Retail Navigates Cost Pressures and Rising Vacancy as Leasing Outlook Improves

Vacancy dipped slightly in Q4 but remains elevated year over year, while pricing resets and steady tenant demand support investment and repositioning across the region.

Competition for prime retail locations is expected to remain steady heading into 2026.

MARKET OVERVIEW

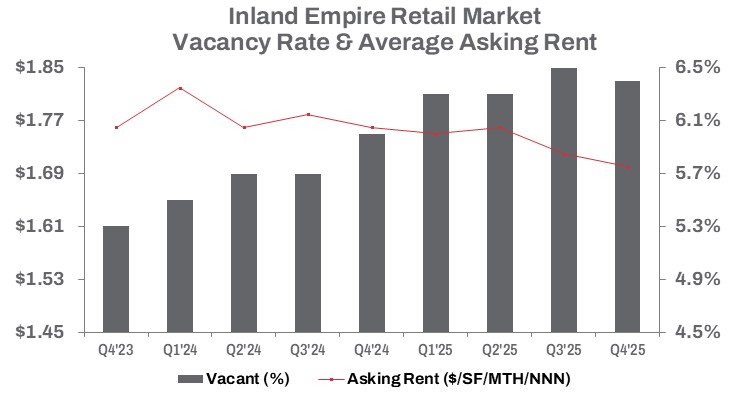

The Inland Empire retail market posted mixed results in late 2025 as the Federal Reserve held interest rates steady, keeping borrowing costs elevated for retailers and consumers in its effort to curb inflation. In Q4 2025, vacancy reached 6.4%, down 10 basis points from the prior quarter and up 40 basis points year over year. Leasing activity declined 32.1% quarter over quarter and slipped 9.6% year to date from 2024 to roughly 3.07 million square feet.

A wave of high-profile retail bankruptcies added pressure. Chains including JoAnn Fabric, Party City, Forever 21, and Rite Aid faced restructuring as declining revenue and rising labor costs proved difficult to sustain. Labor costs remained a key concern as California’s $20-per-hour fast-food minimum wage approached its one-year mark, while the statewide minimum wage increased to $16.90 per hour on January 1, 2026. Higher operating costs and menu price increases continued to test consumer spending.

Since Q4 2020, approximately 3.8 million square feet of retail space has been absorbed across the region, yet availability remained elevated at nearly 9.9 million square feet at year-end 2025. Cooling but persistent inflation and heightened competition continued to weigh on brick-and-mortar performance, prompting landlords to offer concessions to backfill space. Average asking rents held relatively flat at $1.70 per square foot triple net, slipping two cents from the prior quarter and 3.4% year over year.

Some investors shifted toward dispositions as pricing recalibrated, with quarterly sales volume rising 68.7% and year-to-date activity edging up 2.7% from 2024 to more than 4.2 million square feet. Facing higher operating costs and ongoing cost-of-living pressures, the Inland Empire retail market navigated a challenging but gradually stabilizing 2025.

TRENDS TO WATCH

Landlords across the Inland Empire will continue adjusting asking rents to improve cash flow and backfill vacancies. Riverside, the region’s largest retail market, is already seeing this play out. The submarket has roughly 2.8 million square feet of vacant retail space, the highest total in the region, following a 14.1% year-over-year increase. The average direct asking rent declined 1.7% from last year to $1.78 per square foot triple net, and the pricing reset has helped stimulate activity. Leasing rose 22.3% from 2024, while sales volume surged 72.0% in 2025, with approximately 1.3 million square feet trading. The investment uptick was driven by a 28.2% drop in the average sale price per square foot. Even with the increase in transactions, vacancy climbed 80 basis points from Q4 2024 to 7.1%, one of the highest rates in the Inland Empire.

Vacancy has also risen in the Airport submarket, but unlike Riverside, rents have held steady while activity has slowed. The submarket, home to the region’s highest-priced inventory, now has roughly 1.1 million square feet of vacant space, an 18.3% increase from a year ago. Direct asking rents barely budged, rising $0.02 quarter over quarter, and remain 2.7% higher than a year ago at $2.29 per square foot triple net. Leasing declined 32.9% year over year, and sales volume fell 36.4% to 409,618 square feet. The vacancy rate stands at 3.9%, still the lowest in the Inland Empire, though up 60 basis points year over year and slightly below pre-pandemic levels last seen in Q1 2020.

Despite these headwinds, expanding retailers continue to pursue well-located space, particularly second-generation storefronts vacated during recent store closures. Brands such as Dollar General, Aldi, and Tractor Supply are leading planned store openings for 2026.

At the same time, some retailers are contracting. Carter’s plans to close approximately 150 stores, with most closures expected as leases expire. The company has cited tariffs and cost pressures as ongoing challenges. In California, Carter’s operates roughly 24 locations, five of which are in the Inland Empire: Apple Valley, Corona, Chino, Cabazon, and Eastvale.

The quick-service restaurant sector is also seeing selective contraction. Yum! Brands plans to close roughly 250 underperforming Pizza Hut locations across the United States in the first half of 2026. Despite these reductions, Pizza Hut maintains a significant presence in California, with about 500 locations statewide, totaling 81 in the Inland Empire: 39 in Riverside County and 42 in San Bernardino County.

Looking ahead to 2026, competition for prime retail space is expected to remain steady, supporting continued market activity. As pricing continues to adjust, tenants and investors are finding new opportunities. While investment sales activity gained momentum in 2025, that imbalance is unlikely to persist. Strengthening tenant demand and a thinning pool of available properties are expected to redirect activity toward leasing in the year ahead.

As the sector continues to reposition, retailers, landlords, and investors are expected to remain active in pursuing well-located assets and strategic sites across the Inland Empire.