In Q1 2024, the Multifamily Sector Leads the Commercial Real Estate Market in L.A. County

Multifamily Pricing Rises, While Industrial, Retail, and Office Lag Behind

Apartments line the Downtown Los Angeles skyline, set against the backdrop of the snow-capped Mount Baldy/San Gabriel Mountains

Apartments line the Downtown Los Angeles skyline, set against the backdrop of the snow-capped Mount Baldy/San Gabriel Mountains

April 2024 | J.C. Casillas, Managing Director, Research and Public Relations at NAI Capital Commercial

Throughout the first quarter of 2024, L.A. County’s commercial real estate market responded to prevailing economic trends by witnessing a predominant increase in vacancy rates, alongside declines in rents and sale prices across various sectors. However, the multifamily sector stood out, experiencing a simultaneous rise in both rent and sale prices per unit.

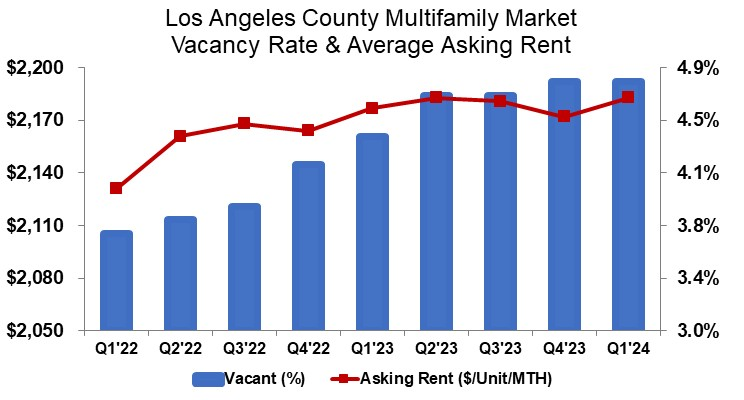

Multifamily

In Q1 2024, the vacancy rate in the multifamily sector remained steady at 4.8%, unchanged from the end of the previous year. The rise in newly completed units, particularly in the high-end market segment, contributed to an increase in the average asking rent per unit this quarter. Following a slight decline in Q4 2023, the average rent saw a half-percentage-point increase quarter over quarter and a three-tenths of a percent increase year over year, as 2,405 units were added to the market. This brought the average asking rent to a record high of $2,183 per unit per month in Los Angeles County.

Despite reaching historic highs in rent prices, multifamily investment has been affected by escalating construction costs, concerns about a slowing economy, high interest rates, and reduced rent growth. The number of units sold this quarter decreased by 59% compared to the previous year, totaling 3,041 units, with the average sale price per unit increasing by 1.4% year over year to $312,857. This marks a modest increase in the average sale price, although the number of units sold remains 41 units higher than in Q1 2009 during the Great Recession.

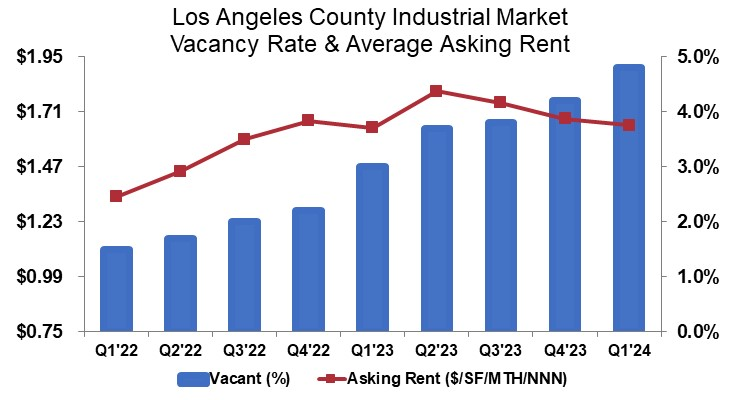

Industrial

In Q1 2024, the vacancy rate for industrial space rose by 60 basis points to 4.8%, while the average asking rent experienced its third consecutive quarterly decline, dropping by 1.8% quarter over quarter and falling just six-tenths below last year’s levels. Despite this, the average asking rent stood at $1.65 per square foot triple net, marking a 23.1% increase compared to Q1 2022.

Although the increase in vacant industrial space provided tenants with more options in 2024, high prices and elevated interest rates dampened sales of industrial buildings. Sales volume decreased by 33.1% quarter over quarter, plummeting by 56.1% compared to the previous year, to approximately 2.7 million square feet by the end of Q1 2024. However, the average sale price per square foot reached $326 in Q1 2024, reflecting a 5.9% decrease year over year.

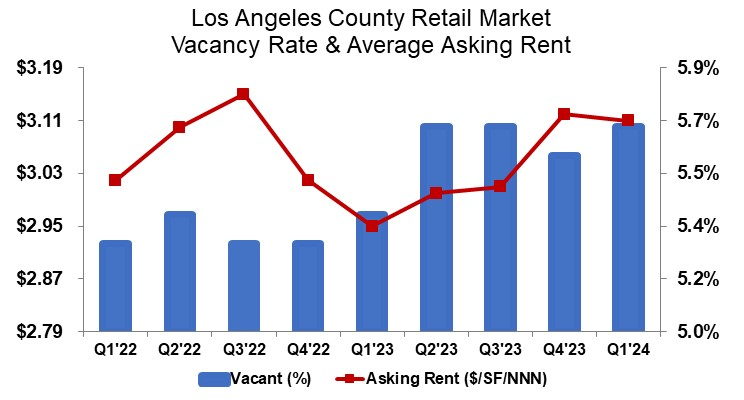

Retail

In Q1, the retail sector witnessed a setback in its pivot back to brick-and-mortar establishments as retailers continued to shutter underperforming locations, resulting in a rise in the vacancy rate to 5.7%. This increase of 10 basis points quarter over quarter and 30 basis points from Q1 2023 reflects the ongoing challenges faced by the industry. The average asking rent slightly decreased by 1 cent from the prior quarter, settling at $3.11 per square foot triple net in Q1. Although the average asking rent saw a 5.4% increase from last year, landlords persisted in adjusting rent to enhance cash flow and occupy available retail space.

Despite the persistent competition for well-located retail space, lackluster rent growth may have prompted cautiousness among investors in retail properties. Sales volume declined by 66% compared to last year, falling just shy of one million square feet. Additionally, the average sale price per square foot dropped by 11.4% from the end of 2023 to $358 per square foot, indicating a challenging market environment for retail property investors.

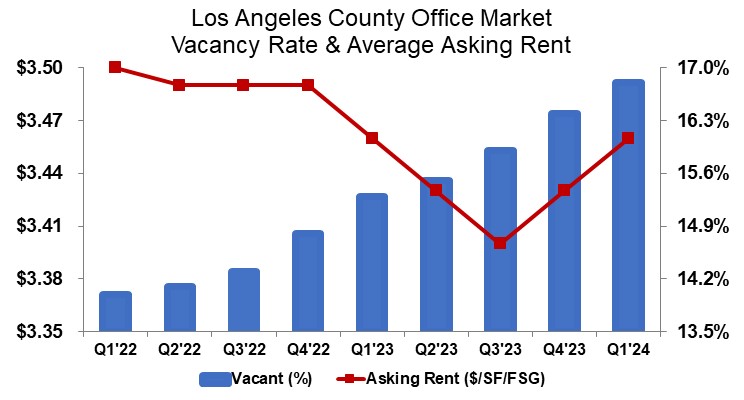

Office

The office space market began 2024 in a weakened state, as companies continued to shed excess space, resulting in a vacancy rate increase to 16.8% in Q1. This uptick of 40 basis points quarter over quarter and 150 basis points from Q1 2023 reflects ongoing challenges within the sector. Surprisingly, the average asking rent saw a rise of 3 cents from its yearend 2023 level, remaining flat from a year ago at $3.46 per square foot full-service gross.

Despite the availability of office space for lease reaching an all-time high of more than 77.4 million square feet—a staggering 28.5% higher compared to the peak of the Great Recession—demand for leasing office space remained low.

In Q1 2024, the surplus of office space significantly impacted the sale of office buildings. Sales volume plummeted by 78.4% quarter over quarter, marking an 81.3% decline from a year ago, attaining only about 1.3 million square feet—a level not seen since the Great Recession. Additionally, the average sale price dropped by 5.6% from Q4 2023 to $402 per square foot.

Figures for Q1 2024 indicate a significant shift in economic conditions. Despite the Federal Reserve maintaining steady interest rates at their March meeting, elevated borrowing costs persisted, posing challenges for commercial real estate. Los Angeles County’s commercial real estate markets are facing ongoing pressure to adapt to these changes, impacting real estate values.