In Q1 Inland Empire’s Industrial Market Surges with a New All-Time High in Available Sublease Space

Sublease Space is Now Four Times Greater Than During the Great Recession

MARKET OVERVIEW

The Inland Empire’s industrial market started 2024 by slowing construction momentum. Approximately 7.4 million square feet of completed construction in the first quarter were added to the market, marking a 45.4% decrease from the previous quarter, which saw the largest amount delivered in a single quarter for the Inland Empire. Over the past two years, the region has added approximately 55.3 million square feet of completed construction to the market, while absorption has resulted in a positive 11.8 million square feet during the same timeframe, indicating an imbalance in the supply-demand trajectory.

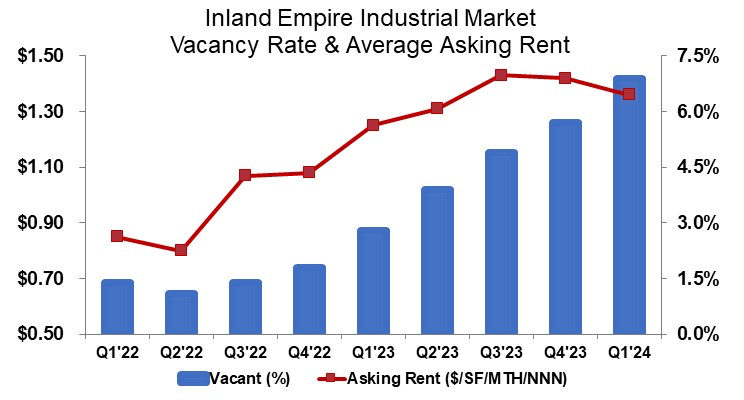

Moreover, space under construction decreased by 19.8% compared to last quarter, representing a 35.1% drop from the prior year at 26.3 million square feet. Developers, who previously raced to meet the demand for warehouse space spurred by e-commerce, have now hit the brakes on development. The once double-digit rent growth, which was the primary driver in the push for new construction, has indicated that the average asking rent in Q1 dropped by 4.2% from the previous quarter to $1.36/SF triple net, still holding on to an 8.8% increase from Q4 2023. Slowing demand has impacted leasing volume, which, while up 6.0% quarter over quarter, is down 25.5% year over year at 10.3 million square feet.

Inland Empire Industrial Market Q1 2024 Statistics:

On the sales side, volume on a square foot basis declined by 64.3% from last year, marking the weakest start to the new year for building sales since Q1 2009 during the Great Recession. Additionally, the average price per square foot is down 24.3% from this time last year.

TRENDS TO WATCH

The abundance of industrial space remains a concern for landlords while offering leverage to tenants in negotiating favorable deals. However, the surge in options for e-commerce warehousing is driving the market as companies pursue flexible solutions to meet evolving demands.

Companies actively reducing excess warehouse space have led to a significant increase in available sublease space, up by 28.2% since the end of 2023 and a staggering 176% higher than Q1 2023, totaling over 20.2 million square feet—a new all-time high. In the Inland Empire, available sublease space is now four times greater than Q1 2009 during the Great Recession, providing ample options for companies with warehousing needs as port cargo remains positive.

Inbound TEU cargo volumes—a key driver of warehouse space demand in Southern California—have increased by 32% year-to-date as of February 2024, according to the latest figures from the Ports of Los Angeles and Long Beach.

While growth rates are expected to slow, elevated prices and interest rates will impact industrial building sales, with well-located, quality space still commanding a premium. In the West submarket neighboring Los Angeles County, along the Ports transportation corridor, the average sale price per square foot increased by 12.9% year over year. In contrast, the East saw a 43.6% drop in the average sale price per square foot, indicating volatility.

The combination of elevated interest rates and slowing demand will continue to stabilize pricing in the first half of the year as opportunities arise in the marketplace.