Third Quarter 2024

L.A. County Retail Market Faces Slow Recovery Amid Economic Pressures and High Vacancy

Retail sector grapples with rising vacancies, ongoing bankruptcies, and shifts in leasing dynamics.

Investor interest in prime locations remains strong despite overall challenges.

MARKET OVERVIEW

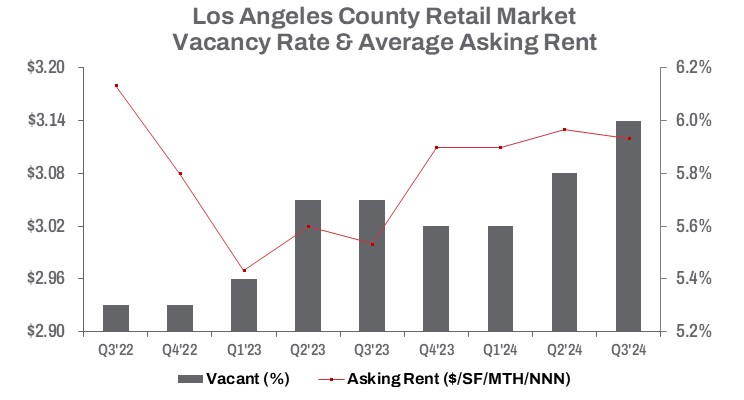

Four years after the pandemic, L.A. County’s retail market recovery continues at a slow pace. In Q3 2024, retail vacancies rose by 20 basis points from the previous quarter and 30 basis points year-over-year, reaching 6.0%. Leasing volume declined by 35.5% quarter-over-quarter to 4,299,625 square feet, marking a 25.1% drop compared to the same period last year.

Bankruptcies among popular retail chains, including 99 Cents Only Stores, Rite Aid, Big Lots and following suit The Franchise Group Inc., the owner of retail chains The Vitamin Shoppe, Pet Supplies Plus and Buddy’s Home Furnishings just filed for Chapter 11 bankruptcy. Retail bankruptcies have become exceedingly common, compounded by revenue loss and further aggravated by higher supply chain and labor costs. California’s fast-food minimum wage increase to $20 an hour is the latest challenge. Since the wage mandate took effect in April, representing a 25% increase from the statewide $16 an hour minimum, California fast-food franchises have been cutting worker hours. Rubio’s Coastal Grill, citing rising business costs, abruptly shut down 48 restaurants in California. The move came two months after the state’s $20 an hour minimum wage took effect for fast-food employees.

Major restaurant chain Red Lobster filed for bankruptcy protection in May after abruptly closing sites, joining other food and retail household names forced to announce closures this year. The tough economic climate and cost-of-living crisis have left many retailers struggling, shedding space. Vacant retail space remains more than 2.8 million square feet above post-pandemic levels from Q3 2020. The total vacant space on the market, exceeding 18.9 million square feet in the third quarter of 2024, represents an all-time high, highlighting the retail market’s ongoing struggle to return to ‘normal’ vacancy levels.

Discount retailer Big Lots plans to close 35 to 40 stores this year, citing “elevated inflation” and decreased consumer spending. This marks the latest chain with a large footprint in California to possibly file for bankruptcy, joining Red Lobster, Rite Aid, and Bed Bath & Beyond. June saw the highest level of bankruptcies since the early days of the COVID-19 pandemic, according to S&P Global. In 2024, the U.S. economy continues to face macroeconomic challenges, including elevated inflation, which has adversely impacted consumer buying power.

TRENDS TO WATCH

As the economy evolves, the demand for retail space is shifting. Despite challenges, investor interest, especially in prime locations, remains strong. The average sale price for retail space increased by 39.3% to $567 per square foot compared to the previous year, while the average asking rent for direct space rose by 4.0% over the same period. Deal velocity suggests that bid and ask prices are stabilizing. Although the sale volume on a square footage basis increased by 56.9% quarter-over-quarter, it showed 43.7% drop year to date compared to the previous year-to-date figures at this. The backfilling of retail space vacated by bankrupt retailers is expected to help maintain occupancy levels. In June, Dollar Tree Inc. announced it acquired leases and assets from 99 Cents Only Stores across the western United States. This acquisition should help stabilize vacancy rates, though increasing occupancy will require organic growth, which may take time.

Retail real estate fundamentals are expected to remain resilient. U.S. retail sales grew solidly in October, highlighting consumer spending as a key driver of economic growth. Recent economic reports underscore a robust economy, with the Conference Board’s latest consumer confidence index posting its largest monthly gain since 2021. The U.S. economy has exceeded growth expectations since the spring, driven by resilient consumer spending—the backbone of economic activity.

Looking ahead, the National Retail Federation projects holiday spending in November and December to increase by 2.5% to 3.5% compared to last year, signaling sustained consumer activity and strong demand for retail real estate. Retail vacancies and rents have been impacted by shifting consumer behaviors and retailer bankruptcies, but demand is increasingly focused on smaller, more efficient retail spaces, creating opportunities for agile businesses.