First Quarter 2025

L.A. County’s Multifamily Market Rebalances Under Pressure in Q1 2025

Rents hit new peak while sales slide in the face of ULA tax and economic headwinds.

Heightened demand is expected to drive rental growth, accelerate rents, and reshape market dynamics, leading to significant changes in the months ahead.

MARKET OVERVIEW

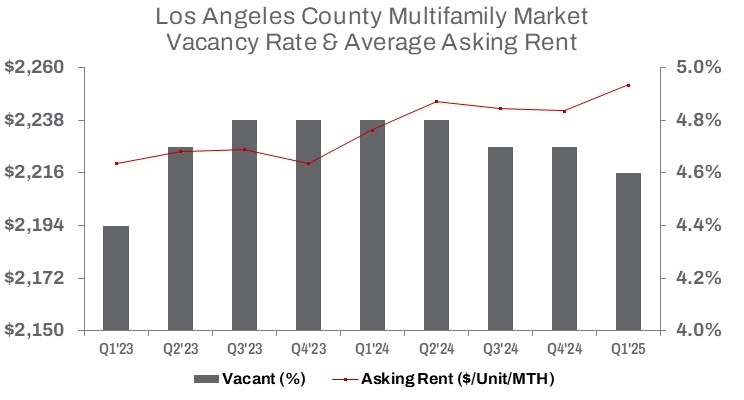

In Q1 2025, the multifamily housing market saw a vacancy rate of 4.6%, down 10 basis points from the end of the previous year and 20 basis points from Q1 2024. An increase in newly completed units, particularly in the high-end segment, helped drive the average asking rent higher this quarter. After a slight decline in 2024, the average rent rose by 0.5% quarter over quarter and 0.9% year over year, with 3,462 units added to the market. While the rent growth appears modest, it pushed the average asking rent to a new record high of $2,253 per unit per month—following a brief reprieve in mid-2024, before the Palisades and Eaton wildfires displaced residents seeking housing.

Despite historically high rent levels, multifamily investment continues to face significant headwinds. Elevated interest rates, concerns about a slowing economy, rising construction and maintenance costs, and limited rent growth have contributed to a more challenging investment environment. The City of Los Angeles’s “ULA Tax”—now in its second year—has further dampened investor appetite, particularly for high-value sales. In Los Angeles, sales volume for apartment properties exceeding the $5,150,000 threshold that triggers the ULA Tax fell by 63.3% quarter over quarter and 42.1% year over year.

In the latest quarter, the impact was evident: the number of units sold declined 38.3% from the previous quarter, totaling 4,864 units. At the same time, the average sale price per unit increased by 8.5% to $292,371—a modest 0.7% increase from the average at this time last year.

Total sales dollar volume countywide dropped by 33.3% quarter over quarter to $1.4 billion. The average capitalization rate held steady at 5.3%, up 30 basis points from the prior year. Buyers and sellers continue to navigate a pricing gap driven by elevated borrowing costs, tight credit, volatile conditions, and softening demand—contributing to the slowdown in deal activity.

TRENDS TO WATCH

The Federal Reserve’s strategy of maintaining elevated interest rates to combat inflation has had a profound impact on multifamily sales. Investment demand has softened, and credit costs for both developers and investors have increased. However, with credit conditions beginning to ease, some financial pressures may subside. Still, higher operating expenses—including rising insurance costs—and a more cautious economic outlook are expected to temper any near-term recovery.

By the end of Q1 2025, completed units surged by 23.7%, while units under construction dropped by 19.1% year over year—signaling a rebalancing in the development pipeline as supply adjusts more closely to current demand.

In the City of Los Angeles, the “ULA Tax” continues to weigh on investor sentiment. Since its implementation in Q1 2023, sales volume for apartment buildings subject to the tax has plummeted—down 81.3% compared to pre-tax levels. Reports indicate that Mayor Karen Bass has considered a temporary suspension of Measure ULA, the so-called “mansion tax,” to assist residents recovering from recent wildfires in the Pacific Palisades.

In the East submarket, where the Eaton Fire occurred, the number of vacant units dropped 5.5% quarter over quarter, while the average asking rent rose 0.7% to $2,068—a record high for the area and up 1.4% from a year ago. In the West submarket, impacted by the Pacific Palisades Fire, the average asking rent rose 0.5% to $2,712—also a record and up 0.9% year over year.

Following the governor’s January 7, 2025, emergency declaration for Los Angeles County, California’s anti-price gouging law was automatically triggered, temporarily capping rent increases at no more than 10% above pre-emergency levels. That protection expired on March 8, 2025.

In Q1 2025, the East submarket completed construction on 559 units—up 32.8% quarter over quarter and a notable 133.6% year over year. The West submarket completed 545 units, a 10.8% quarterly increase but down 33.1% from the same period last year. However, units under construction declined year over year—down 38.6% in the East and 18.6% in the West.

As the multifamily market works to meet the urgent housing needs of residents displaced by the fires, supply and demand are rebalancing. Government regulation continues to play a significant role. This heightened demand is expected to fuel further rent growth and reshape market dynamics heading into the critical spring and summer leasing seasons.