Third Quarter 2025

L.A. County Multifamily Market Shows Stable Rents, Rising Vacancy, and Stronger Investment Activity in Q3 2025

Elevated interest rates and declining development pipelines reshape multifamily fundamentals as investors pursue opportunities in the midst of tax-driven pressures and a tightening supply outlook.

Median prices are down, fueling a surge in investment activity as acquisition and development strategies adjust.

MARKET OVERVIEW

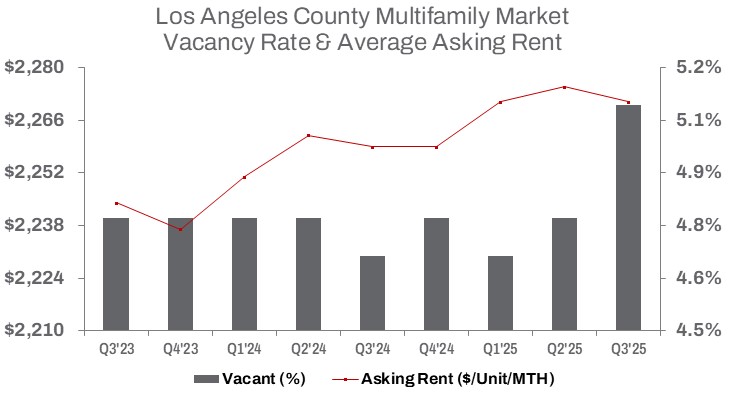

In Q3 2025, Los Angeles County’s multifamily market displayed early signs of stabilization. The average asking rent dipped 0.2% quarter over quarter but remained 0.5% higher year over year at $2,271 per unit. Moderating rent growth indicates a market gradually moving toward equilibrium between ongoing supply additions and tenant demand.

Vacancy increased 30 basis points quarter over quarter and 40 basis points year over year, reaching 5.1%, driven in part by slowing household formation and affordability constraints. Although vacancy remains below its pandemic peak of 5.7% in Q3 2020, the continued uptick reflects recalibrating demand as economic uncertainty influences renter behavior while new units enter the market.

This quarter delivered 5,663 units, bringing year-to-date completions to 12,572 units, 17.8% above the prior year total. The additional inventory suggests that available supply will be absorbed gradually as new space leases up. New construction activity continues to contract, with units under construction declining 10.5% quarter over quarter and 21.9% year over year, marking a notable retreat from the post-2020 development peak.

Transaction activity accelerated meaningfully compared with the prior quarter. Sales volume reached $2.45 billion, up 26.3% from Q2, although year-to-date volume remained 9.4% lower year over year at $5.91 billion. The median sale price declined 4.7% quarter over quarter and 4.2% year over year to $257,321 per unit, underscoring ongoing price revisions as investors adjust to borrowing costs and evolving underwriting standards.

Cap rates dipped 10 basis points quarter over quarter yet held flat year over year at 5.4%, reinforcing the measured repricing trend across the region. Unit sales increased 32.5% quarter over quarter to 9,401 units, with year-to-date totals up 13.5% to 21,482 units sold, reflecting renewed investor appetite supported by discounted opportunities and more flexible deal structures.

TRENDS TO WATCH

High interest rates continue to shape investment behavior by increasing the cost of capital and suppressing asset valuations. Although elevated mortgage rates create persistent barriers to homeownership and support baseline rental demand, they also restrict investor leverage and complicate refinancing strategies.

Development starts remain constrained due to construction financing challenges and persistent materials and labor costs. With under-construction inventory falling sharply year over year, Los Angeles County is entering a pipeline slowdown that will eventually restrict availability, especially in attainable and workforce housing categories.

Regulatory influences remain a defining consideration for investors. Measure ULA, Los Angeles’ property transfer tax on assets above $5.3 million—5.5% for properties sold at $10.6 million or more—continues to weigh on high-end sales activity within the city. As a result, deal activity has increasingly shifted toward suburban municipalities outside Los Angeles to mitigate ULA’s incremental tax exposure. This dynamic has constrained transaction volume at the upper end of the market, influencing pricing, investment strategies, and capital deployment decisions within the city. Still, large investors remain undeterred. This quarter, Hines, a global real estate investment manager, acquired Runway at Playa Vista, a 630,000-square-foot mixed-use property, for $428.1 million. Runway features 420 luxury residences, which Hines acquired as part of the deal for $283,652,219, or approximately $675,362 per unit, along with marquee retail, dining, and medical office space anchored by Whole Foods.

Q3 2025 reflected a transitional period in the regional multifamily market. Slower rent growth, mild vacancy increases, and falling construction volumes signal recalibration following multiple years of supply expansion. Investment activity improved quarter over quarter as pricing adjusted toward market expectations, with suburban markets outperforming Los Angeles’ core due to reduced tax exposure and stronger capital receptivity.

The market remains fundamentally supported by long-term housing demand, though policy outcomes and capital constraints will continue to steer both investment strategy and development decision-making over the next 12 to 24 months.