Fourth Quarter 2024

Los Angeles Multifamily Market Faces New Pressures Amid Construction Slowdown and Rising Demand

Vacancy rates hold steady for now as wildfires, tight credit, and inflation signal shifting market dynamics.

Heightened demand is expected to drive rental growth, accelerate rents, and reshape market dynamics, leading to significant changes in the months ahead.

MARKET OVERVIEW

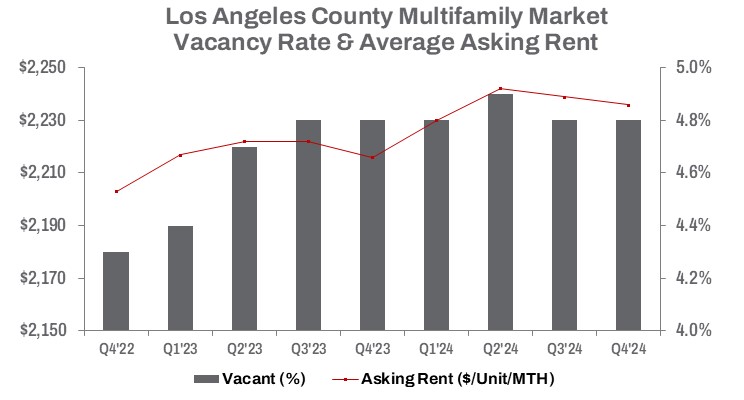

The influx of new multifamily construction aimed at reshaping Los Angeles County’s housing market appears to have run its course for now. In Q4 2024, the vacancy rate held steady at 4.8%, unchanged both quarter-over-quarter and year-over-year. This trend reflects the alignment of completed construction projects with demand.

As credit conditions tightened, the multifamily market adapted to higher borrowing costs, persistent inflation, a softer growth outlook, and heightened financial risks. These factors contributed to a significant 20.0% drop in completed construction quarter-over-quarter and a 24.3% decline year-over-year. Developers are slowing down, evidenced by a 10.1% annual decrease in the number of units under construction.

Since Q1 2024, the overall number of occupied units has increased by 0.8%, or 9,208 units. The addition of 12,464 newly completed units, primarily in the first half of the year, has fostered a more competitive rental environment. Despite this, the average asking rent recorded a modest decline of $3 from the previous quarter, ending Q4 2024 essentially flat at $2,236 per unit. However, this still represents a 0.9% increase compared to the same period last year. The slowdown in multifamily housing construction is starting to influence the rental market, with demand gradually catching up to supply.

Although the number of units sold retreated slightly by 0.57% from the previous quarter, year-over-year sales have increased significantly, up 18.4% year-to-date compared to 2023. This trend reflects the mixed financial conditions investors are currently facing. Many are grappling with a price disparity with sellers, driven by rising interest rates, tight credit, and softening market conditions. As a result, sales volume has experienced a slower 5.9% growth rate in 2024. The average cap rate increased by 30 basis points from last year, while the average sale price per unit saw a notable 8.1% drop.

TRENDS TO WATCH

The Federal Reserve’s plan to maintain current interest rates to curb economic activity and inflation is poised to significantly impact the multifamily sales market in the coming months. Higher credit costs for developers and refinancing investors are expected to gradually reshape market dynamics. As credit conditions continue to tighten, the multifamily market will likely face increased borrowing costs, persistent inflationary pressures, cautious growth prospects, and heightened financial risks.

The strong labor market and the potential for accelerating year-over-year consumer inflation suggest that the likelihood of a Federal Reserve rate cut remains low in the near term. With U.S. unemployment at 4.1% and robust payroll growth persisting, a rate cut before mid-2025 appears improbable. Inflation is projected to stay elevated, potentially delaying rate reductions until late 2025, when inflationary pressures are expected to ease.

Tightening credit conditions and sustained inflation are anticipated to further slow the multifamily construction pipeline. Recent wildfires in Los Angeles County are expected to compound these challenges, with preliminary estimates indicating that over 12,000 structures were damaged or destroyed in densely populated areas of Pacific Palisades, Altadena, and Pasadena—home to approximately 66,000 residents collectively. This devastation is expected to intensify housing demand, placing further strain on the multifamily market.

Apartment investors in California will face additional hurdles due to rising insurance costs and challenges in securing coverage in wildfire-prone areas. Increased premiums and stricter insurance requirements in high-risk zones are likely to elevate operational expenses, complicate underwriting, and impact investor returns and property valuations.

Meeting the urgent housing needs of displaced residents will be a critical priority for the multifamily market. This heightened demand is expected to fuel rental growth, accelerate rents, and reshape market dynamics, driving significant changes in the months ahead.