Fourth Quarter 2025

Los Angeles County Multifamily Market Transitions as Development Activity Slows

A late-year construction pullback slowed supply growth, though rent growth and pricing remain constrained.

Cap rates expanded, development activity cooled, and rent growth remained limited across Los Angeles County.

MARKET OVERVIEW

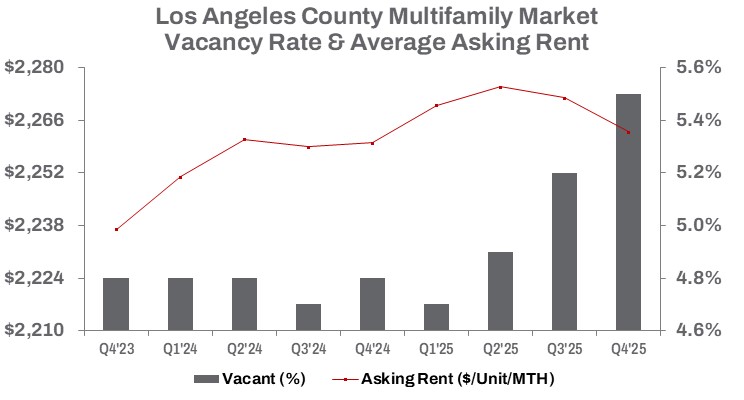

The influx of new multifamily construction intended to reshape Los Angeles County’s housing market appears to have run its course, at least for now. In Q4 2025, the vacancy rate climbed to 5.7%—a level not seen since the height of the pandemic shutdown in late 2020. This represents a 30-basis-point increase quarter-over-quarter and an 80-basis-point rise year-over-year, as a wave of recently completed projects met cooling demand, forcing a more gradual absorption across the county.

As credit conditions tightened, the multifamily market adjusted to higher borrowing costs, persistent inflation, a softer growth outlook, and elevated financial risk. These pressures contributed to a sharp 51.5% decline in completed construction quarter-over-quarter, bringing the year-to-date total to a 10.7% increase compared to the prior year, despite the late-year pullback. Developers have responded by slowing new activity, reflected in a 19.5% year-over-year decline in the number of units under construction.

Since Q1 2025, total occupied units have increased by just 0.1%, or 788 units. Meanwhile, the delivery of 15,406 newly completed units in 2025 has intensified competition among landlords. Average asking rents declined modestly by $9 quarter-over-quarter, ending Q4 2025 essentially flat at $2,263 per unit. On an annual basis, rents edged up only 0.1%, suggesting that pressure on rents is beginning to stabilize as construction activity slows.

On the investment side, transaction activity continued to build, with unit sales rising 5.4% quarter over quarter and year-to-date volume up 14.5% from 2024. This reflects investors adjusting to moderating financial and credit conditions, as well as ongoing pricing gaps between buyers and sellers. As a result, dollar sales volume posted a muted 2.3% increase in 2025. Average cap rates rose 40 basis points year-over-year to close at 5.6%, while the median sale price per unit declined 2.7%.

While addressing the housing needs of residents displaced by wildfires at the start of 2025 remained a critical social priority, the anticipated surge in market-wide demand failed to materialize. Rather than driving meaningful rent growth or reshaping broader market dynamics, the impact remained localized, leaving the market’s trajectory primarily defined by the ongoing lease-up of newly delivered inventory.

TRENDS TO WATCH

The Federal Reserve’s decision to maintain interest rates at current levels is expected to weigh on multifamily sales activity in the months ahead. Elevated borrowing costs for developers and refinancing investors continue to reshape market dynamics, increasing financial risk and constraining capital availability. Although the Fed implemented several rate cuts in late 2025, the current pause suggests further reductions may be delayed until late 2026 as policymakers await inflation’s return toward the 2% target.

The labor market remains relatively resilient despite signs of deceleration, with Los Angeles County unemployment hovering near 5.6%. This stability, combined with inflation that has leveled off but remains elevated due to recent trade tariffs, reduces the likelihood of a near-term rate cut. With job growth slowing and inflationary pressures proving sticky, many economists expect a return to materially lower rates only in the second half of 2026. These conditions, alongside muted rent growth, are expected to further suppress new multifamily construction starts.

Policy uncertainty adds another layer of complexity. Los Angeles voters could be asked as early as June 2026 to reconsider the city’s voter-approved “mansion tax” as City Council members advance proposed amendments to Measure ULA. The push for reform reflects concerns that the tax has slowed high-value transactions and discouraged private development. Since its adoption, Measure ULA has significantly reduced sales of properties priced above $5 million, prompting officials to seek adjustments that preserve housing objectives while supporting development feasibility.

Under the proposed changes, a 15-year exemption would apply to properties transferred within 15 years of receiving a certificate of occupancy for new construction or substantial rehabilitation. The measure would also grant the city authority to issue temporary three-year hardship exemptions following natural disasters, such as the 2025 Palisades fire, when property owners can demonstrate undue financial burden. If approved by the City Council, the proposal would appear on the June 2, 2026, ballot for voter consideration.

Beyond taxes, apartment investors face mounting challenges tied to rising insurance costs, particularly in wildfire-prone areas. Higher premiums and tighter underwriting requirements are increasing operating expenses, complicating deal underwriting, and pressuring returns. While the immediate post-disaster demand surge has largely passed, ongoing affordability constraints and elevated operating costs are expected to shape investment decisions and development activity through 2026.