First Quarter 2025

Los Angeles County Office Market Shows Recovery Signs in Q1 2025 with Rising Occupancy and Sublease Demand

Occupied space rose as vacancy fell to 16.7%, with a tenants’ market driving subleases and cost savings.

While challenges persist in achieving a full post-pandemic return to the office, improving occupancy is helping stabilize rents.

MARKET OVERVIEW

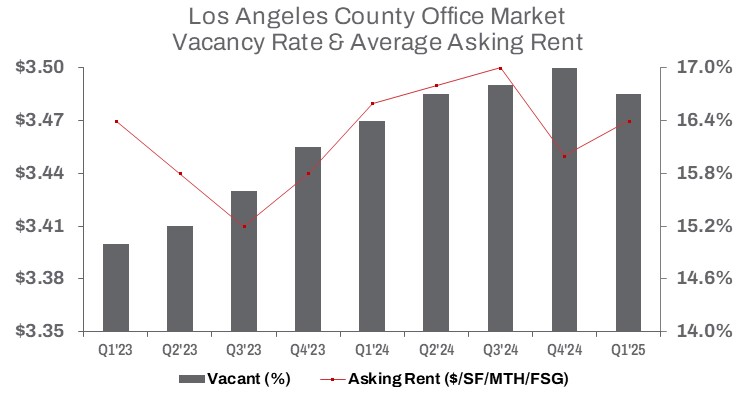

During the first quarter of 2025, the Los Angeles County office market showed signs of recovery, with occupied space increasing by 348,604 square feet quarter-over-quarter. This growth pushed the vacancy rate down to 16.7%, a 30-basis-point decline from the previous quarter, though still 30 basis points higher year-over-year. Total occupied space reached more than 332 million square feet. For perspective, in Q1 2020—prior to the pandemic—occupied office space stood at approximately 355 million square feet, highlighting how much the market still needs to regain.

A gradual return-to-office trend—shaped by mandates, workplace flexibility, and evolving space needs—supported a strong quarter of positive net absorption, totaling approximately 230,383 square feet on a direct basis. Sublease activity also played a critical role, contributing an additional 118,221 square feet of net absorption, marking a solid start to 2025. Available sublease space declined slightly by 2.7% from the previous quarter and fell 4.3% year-over-year to 10.9 million square feet—contracting at a faster rate than direct space availability, as companies either sublet excess space or returned it to landlords.

In contrast, direct availability rose 1.0% quarter-over-quarter and 1.1% year-over-year to approximately 66 million square feet.

By the end of Q1, the market recorded approximately 1.6 million square feet in office sales volume, a 56.4% decline from Q4 2024, but a 42.6% increase compared to the sluggish first quarter of last year. The average sale price dropped 5.3% from the prior quarter and 36.2% year-over-year to $249 per square foot.

While challenges persist in achieving a full post-pandemic return to the office, improving occupancy is helping stabilize rents. The average asking rent increased by $0.02 from the prior quarter to $2.47 per square foot on a full-service gross basis, though it remains down 0.3% from a year ago. Leasing volume reached nearly 4.8 million square feet in Q1—down 7.4% from Q4 2024 and 5.0% from the same period last year. Landlords remain hesitant to reduce asking rents, but many continue to offer concessions and flexible lease terms. The market remains tenant-favorable, defined by a lack of consistent new leasing activity and a trend of tenants renewing or rightsizing their office footprints.

TRENDS TO WATCH

Sublease leasing activity for office space in Los Angeles County gained momentum in 2025, rising 42.1% year-to-date compared to the same period in 2024. In contrast, direct leasing activity continued to lag, down 8.5% year-to-date. While tenants leased close to half a million square feet of sublease space—compared to 4.3 million square feet of direct space in Q1 —the increased demand for subleases reflects a search for value, as sublease asking rents to have dropped 8.9% year-over-year.

The high cost of tenant improvements continues to present challenges for owners, creating opportunities for tenants willing to adapt to existing sublease spaces—particularly as the flight to quality persists. The LA West submarket, home to the largest concentration of Class A office space, is well-positioned to capture this demand, accounting for 35.4% of the county’s available sublease space, or 3.9 million square feet. Asking rent for sublease space in LA West averages $4.01 per square foot on a full-service gross basis—16.6%, or $0.80, lower than direct space—highlighting potential savings for tenants seeking premium office space at a discount.

With a significant amount of office space available, signs of a positive shift are emerging as tenants increasingly pursue subleases to reduce costs. Countywide, the average asking rent for sublease space is $2.75 per square foot—20.7%, or $0.72, lower than direct space—creating meaningful opportunities to optimize expenses and secure favorable lease terms. For tenants focused on value, the Tri-Cities submarket stands out, where sublease asking rents average $2.25 per square foot—40.3%, or $1.52, below direct space. This rent gap reflects a broader trend that’s likely to stimulate demand as sublessors approach lease expirations and look to offset sunk costs.

On the sales side, the first quarter of 2025 reflected ongoing shifts, with square footage sold declining 55.6% from the previous quarter to 1.6 million square feet. However, that figure was nearly double the volume recorded in Q1 2024, which marked one of the lowest points since the financial crisis. Over the same period, the average building size sold dropped 34.2% quarter-over-quarter to 30,629 square feet. Sales volume also fell, down 56.4% to nearly $392 million.

This trend toward smaller, more manageable properties suggests evolving preferences among owner/users and investors in response to economic conditions. The sharp declines in both sales volume and average building size point to a market in transition, with buyers refining acquisition strategies and waiting for more favorable conditions. Together, these shifts underscore a period of recalibration, as both tenants and investors adapt to changing market dynamics.