Fourth Quarter 2025

Tenant-to-Owner Shift Becomes Part of Stabilization Taking Shape in L.A. County’s Office Market

Availability remains high, yet renewed investment and tenant-to-owner conversions highlight long-term confidence across key submarkets.

A rebound in sales activity is creating new opportunities for tenants and investors entering 2026.

MARKET OVERVIEW

The recovery of Los Angeles County’s office market remains sluggish, constrained by elevated vacancy and soft tenant demand. New construction continues to expand market inventory, with 237,887 square feet completed in 2025. However, roughly 39.0% of this space remains vacant as landlords hesitate to materially reduce published asking rents.

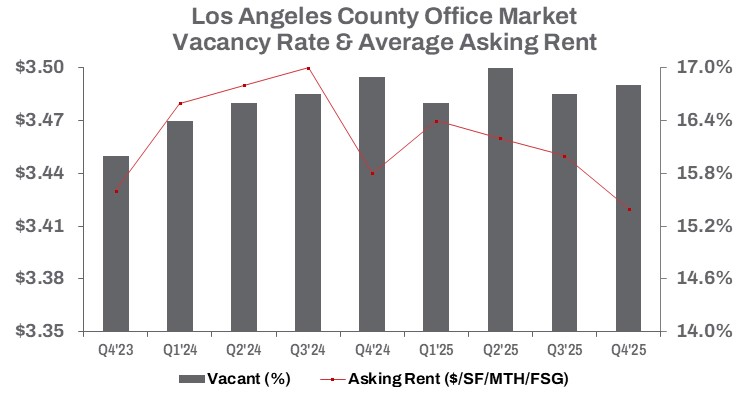

Vacancy fluctuated throughout 2025, ending Q4 at 16.8%. While this represents a slight 10-basis-point increase quarter-over-quarter, it sits 10 basis points below the same period last year. These modest shifts suggest the market may be approaching a stabilization point following several years of rapid vacancy growth.

Available office space reached a record 75.8 million square feet in the previous quarter, a historic high. Although the pace of increase has slowed, the availability rate has remained above 18% since Q1 2023. This level continues to exceed that seen during the Great Recession, indicating the market is still working through a deep occupancy trough.

Sublease space, while still significant, has begun to moderate. Total sublease inventory declined 7.7% quarter-over-quarter and 21.5% year-over-year to 8.3 million square feet. Even so, the current total remains 71.1% above pre-pandemic levels six years later. Some of this decline reflects space being absorbed or returned to landlords and reintroduced as direct availability. While sublease inventory peaked in mid-2024, it continues to weigh on overall market conditions.

Despite these headwinds, asking rents have held relatively firm. The average full-service gross asking rent declined just three cents quarter-over-quarter to $3.42 per square foot, essentially flat year-over-year. Rather than reducing face rates, landlords continue to rely on concessions to attract tenants, even as year-to-date leasing volume fell 8.7% compared to 2024.

Overall, while vacancy growth has slowed, elevated availability and lingering sublease space point to muted demand momentum. The market shows early signs of stabilization, though the path to a full recovery remains gradual.

TRENDS TO WATCH

Los Angeles County’s office market is moving through a phase of measured recalibration, with tenants and investors continuing to seek long-term value. Although availability has eased from its peak, it remains elevated enough to attract occupiers looking to secure space at adjusted pricing. A growing number of tenants are also transitioning into owner-users, signaling confidence in the region and contributing to a pickup in investment activity.

Year-end sales activity reflected this renewed momentum. The average sale price per square foot rose 3.5% quarter-over-quarter in Q4 2025 to $291, approximately 11.1% higher than a year earlier. Year-to-date sales volume reached $3.8 billion, up 69.1% from 2024. At the same time, the broader market continues to reprice. The annual median cap rate for office assets increased 30 basis points year-over-year to 6.2%, while the annual average price per square foot declined 3.4% to $411. On a square-foot basis, total sales reached 13 million square feet for the year, the highest level in seven years and 45.4% above 2024. Together, these figures point to an active but value-driven investment environment.

Recent transactions illustrate how both owner-users and investors are responding. In West Los Angeles, Hudson Pacific Properties sold a 282,395-square-foot campus to Riot Games for a combined $231 million, or roughly $818 per square foot. The transaction included $150 million for the real estate and an additional $81 million to terminate Riot’s existing lease, allowing the longtime tenant to secure the property for continued operations.

In Beverly Hills, an 82,886-square-foot office building at 8942 Wilshire Boulevard traded off-market for $90 million, or $1,086 per square foot, to Alo. The property was vacant at closing, and the buyer plans to occupy the building as its headquarters, reinforcing the continued role of owner-user acquisitions in prime locations.

Pasadena also recorded a notable sale, with a 164,101-square-foot office and flex property at 2964 Bradley Street acquired by Amazon for $78.76 million, or about $480 per square foot. Originally developed as a telecom data center and later converted to flex office space, the property’s infrastructure and proximity to research institutions made it well suited for advanced computing and cloud-related operations. The purchase reflects a broader trend of technology users acquiring facilities to support long-term operational needs.

As 2026 begins, the office market remains in transition. Pricing adjustments, higher cap rates, and sustained availability continue to create openings for tenants and investors seeking value. At the same time, owner-user demand and selective acquisitions are helping to stabilize activity. These dynamics are expected to persist into the coming year, shaping a more balanced market as Los Angeles County’s office sector continues its gradual recovery.