Third Quarter 2025

L.A. County Retail Market Faces Elevated Vacancies and Price Correction in Q3 2025

Asking rents softened, availability remained high, and investors focus on cost-conscious strategies as sales stabilize.

Despite returning shoppers and steady demand in prime locations, elevated vacancy and slower leasing are shaping retail fundamentals across Los Angeles County.

MARKET OVERVIEW

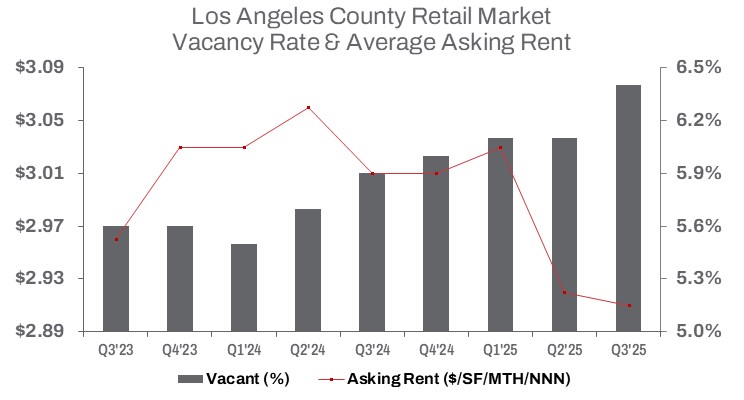

Los Angeles County’s retail market continued to navigate a slow and uneven recovery in Q3 2025. While shoppers have largely returned to brick-and-mortar locations, demand has not fully rebounded to pre-pandemic levels. Vacancies edged higher once again, rising to 6.9%, up from 6.7% last quarter and 6.2% a year ago, as retailers remain cautious and select chains continue to close under economic pressure. Total vacant space reached an all-time high of 19.8 million square feet, pushing the market further above typical vacancy levels.

Availability also rose quarter-over-quarter, now sitting at 21.2 million square feet — the highest level of space marketed for lease in this cycle — reflecting slower leasing decisions and growing sublease options. Net absorption remained negative at 789,520 square feet for the quarter, bringing year-to-date absorption to –1.5 million square feet, indicating store closures continue to outpace new commitments.

Construction has slowed dramatically, with only 557,900 square feet underway across the County — helping prevent a deeper imbalance between supply and demand. Just 40,172 square feet delivered this quarter, the lowest level in years, as developers remain cautious about financing and future tenant demand.

Pricing trends reflect the tempered retail environment. The countywide average asking rent decreased to $2.91 per square foot NNN, a modest decline year-over-year, as landlords continue offering concessions to retain tenants and attract new users. On the investment side, the average sale price reached $253 per square foot, below both last quarter and a year earlier. Despite financing headwinds, retail sales volume increased to $660.5 million this quarter following a slower start to 2025, as buyers remain value-focused and capital markets pressures persist. Year-to-date, sales volume is up 14.1%, approaching $1.7 billion.

Despite these challenges, leasing activity demonstrated signs of resilience quarter-over-quarter, totaling 1.5 million square feet and bringing year-to-date leasing volume to nearly 4.6 million square feet — still 17.6% slower than last year.

TRENDS TO WATCH

Landlords continue to offer concessions to attract tenants, particularly in submarkets with higher vacancy or aging retail centers where differentiation is more difficult. Sublease availability is moderating, yet high-priced listings are seeing continued downward adjustments as retailers negotiate for more affordable terms. Expansion-driven users remain focused on well-located spaces, fueling demand in prime submarkets. Construction remains limited, keeping new supply growth in check, while opportunistic investors capitalize on pricing disparities across the County.

Owners are increasingly prioritizing cost-conscious reinvestment strategies. Cosmetic upgrades and targeted tenant improvements are being deployed where they directly support occupancy — refreshing storefronts, updating signage, enhancing outdoor seating, and improving visibility and customer experience. Instead of high-cost redevelopments, capital is being directed toward “right-sizing” spaces and accelerating leasing readiness — especially for smaller footprints favored by QSR, personal services, and neighborhood-oriented retailers.

Conversely, owners who defer reinvestment risk falling behind as tenants demand higher-quality space and competition intensifies. Aging assets without upgrades often require deeper concessions and endure prolonged vacancy, eroding cash flow and asset value, particularly in secondary locations where rents are softening. A deliberate ‘divest and reinvest’ strategy, selling weaker assets and redeploying capital into higher-performing properties, is becoming increasingly common as pricing adjusts.

There remains a risk of over-investment if landlords overshoot tenant needs. Incremental improvements with clear leasing payoff remain the most effective strategy, particularly in Los Angeles where high land costs make new development less feasible. Repurposing underperforming units for non-traditional uses — medical, coworking, entertainment, and community-centric concepts — is gaining traction, offering diversification and stronger resilience with moderate retrofit costs.

Overall, Q3 2025 reflects a measured recovery. Leasing demand is stabilizing, rent adjustments remain moderate, and disciplined capital strategies are shaping performance across Los Angeles County. While fundamentals continue to improve at a gradual pace, elevated availability suggests the market will need more time to restore balance as consumer spending and retailer expansion plans evolve heading into 2026.