Fourth Quarter 2024

In Q4 2024, LA County’s Retail Market Continued Its Slow Recovery as Bankruptcies Surged Four Years After the Pandemic

Declining prices and increased concessions defined the final quarter of 2024.

Expanding retailers, however, are actively pursuing well-located retail spaces, particularly those available for sublease or vacated during the “retail apocalypse.”

MARKET OVERVIEW

While the economy is humming along, it has posed challenges for landlords in Los Angeles County’s retail market. Demand for retail space has resulted in mixed yet broadly positive trends, with excess inventory gradually being absorbed.

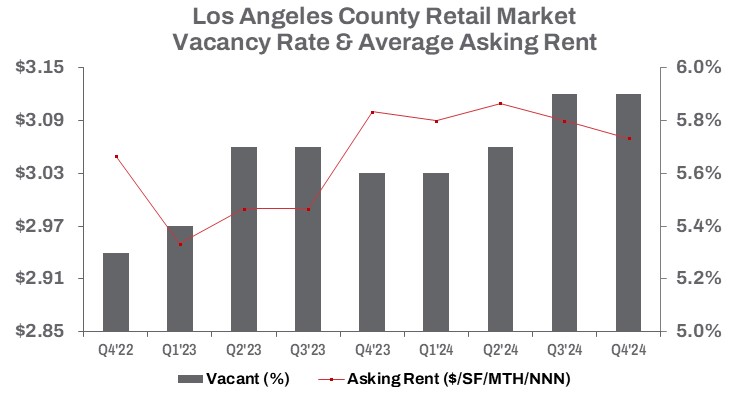

Bankruptcies in 2024 caused the closure of several popular retail chains. However, many retailers seized opportunities to pivot back to brick-and-mortar stores, backfilling spaces vacated by defunct brands. As a result, retail space occupancy increased by only 53,903 square feet quarter-over-quarter but remained nearly 1.5 million square feet below Q4 2023 levels. Total vacant space declined from its peak last quarter, ending the year at 18.8 million square feet. While this progress was encouraging, the market still has significant ground to cover before vacancy levels could return to pre-pandemic norms.

Minimal occupancy gains prompted landlords to offer concessions and lower asking rents. Some investors, shifting to a selling strategy, accepted reduced prices to close deals. The average sale price for retail space dropped to $413 per square foot, a 19.5% decline from the previous quarter. This price adjustment fueled a 121.2% increase in square footage sold during Q4, exceeding 3.8 million square feet—the highest fourth-quarter total since 2021. This translated to a quarter-over-quarter sales volume increase of 31.6%; however, total sales volume for 2024 remained 17.1% lower than in 2023, totaling approximately $1.9 billion.

Meanwhile, the average asking rent for direct space dipped slightly, decreasing 0.5% quarter-over-quarter and 1% year-over-year to $3.07 per square foot triple net. Leasing activity also softened, with year-to-date totals for 2024 coming in 11.3% below the previous year.

TRENDS TO WATCH

Landlords and sublessors will continue adjusting asking rents to improve cash flow and fill available retail space. LA West, which holds approximately 5.1 million square feet of available retail space—the most in the region—experienced a 4.3% year-over-year decrease in asking rents for direct space, dropping to $4.68 per square foot triple net. This decline has spurred some improvement in demand, with many sublessors offering competitive sublease terms.

Despite being home to Los Angeles County’s most prestigious retail market, LA West recorded 219,176 square feet of negative absorption in 2024. While this represents an improvement from 2023, it still contributed to a 10-basis-point year-over-year increase in the vacancy rate, which rose to 7.9%. Sublease space underwent significant adjustments, with average rents declining by 34.2% year-over-year by the end of 2024. High-priced retail sublease space faced substantial reductions, while vacant sublease inventory decreased by 4.7% over the same period. Property owners are expected to continue offering incentives to attract replacement tenants, but filling large, vacated spaces remains a challenge. Expanding retailers, however, are actively pursuing well-located retail spaces, particularly those available for sublease or vacated following the “retail apocalypse.”

The South Bay, home to the Del Amo Fashion Center—the largest shopping center in the western United States, with a 99% occupancy rate—serves as a bellwether for the Los Angeles County retail market. As one of the region’s largest retail submarkets, the South Bay experienced a 0.8% year-over-year decline in average asking rents for direct space, while sublease rents dropped by 21.1%, ending the year at $2.88 per square foot triple net.

In Q4 2024, the average sale price per square foot for retail properties in the South Bay fell to $421, marking a 24.2% decrease compared to Q4 2023. However, this price adjustment drove a 219.5% increase in square footage sold throughout 2024, reaching nearly 2.3 million square feet—the highest sales activity in Los Angeles County for the year.

Looking ahead to 2025, competition for well-located retail space is expected to remain strong, driving market activity. Investors are seizing opportunities, as reflected by the average sale price per square foot for retail buildings sold in Q4 2024, which increased by 2.3% year-over-year to $481 per square foot. Retailers, sublessors, landlords, and investors are poised to aggressively compete as the retail sector continues its recovery.