Second Quarter 2025 Trends

L.A. County’s Retail Market Faces Price Correction in Q2 2025

Vacancy remained at a historic high, asking rents declined, and investors shifted strategy as sales volume pulled back from a strong first quarter.

While job growth and spending support retail demand, excess space and falling prices continue to challenge landlords in Los Angeles County.

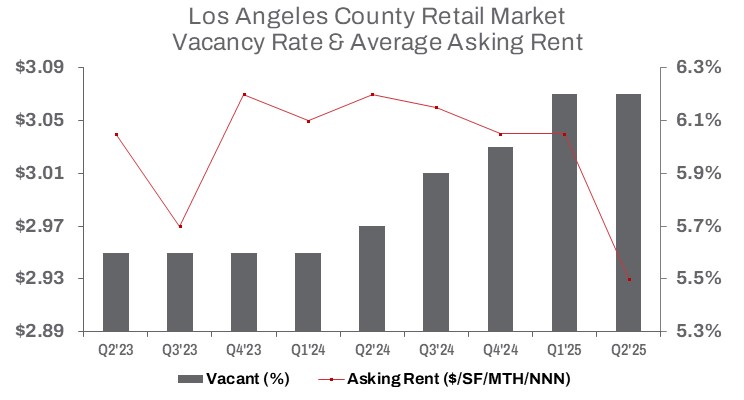

The vacancy rate held at 6.2% quarter-over-quarter, up 50 basis points from Q2 2024. The slow pace of improvement underscores how far the market still has to go to return to pre-pandemic norms.

Average asking rents for direct space declined again—down 3.6% quarter-over-quarter and 4.6% year-over-year to $3.04 per square foot, triple net. Leasing activity also softened, with just under 1.3 million square feet leased in Q2, representing a 25.2% drop from Q1 2025. Year-to-date leasing volume was down 26.9% compared to the first half of 2024.

Persistent occupancy challenges have pushed landlords to continue offering concessions and lowering asking rents. Some investors, anticipating further pricing erosion, opted to sell. Despite that, total sales volume fell 47.4% from Q1, with just 1.5 million square feet sold—signaling a broader slowdown following a strong start to the year. At the same time, the average sale price for retail space declined to $375 per square foot—down 22.0% quarter-over-quarter and 27.8% year-over-year—evidence of a continuing price correction.

Still, when combined with a strong first quarter, total square footage sold year-to-date rose 75.1% compared to the first half of 2024. And despite the quarter-over-quarter dip, retail sales volume reached approximately $1 billion in Q2—up 11.9% from the same period last year. Opportunistic investors drove much of this activity, capitalizing on the current pricing environment and focusing on well-located assets.