Los Angeles County’s Commercial Real Estate Sales Market Adapts in Q3 2024

Despite Rising Cap Rates, Taxes, and Regulatory Hurdles, Key Sectors Show Promising Signs of Recovery and Investor Interest

On September 18, 2024, the Federal Reserve cut the federal funds rate by 50 basis points after four consecutive 25 basis point hikes in 2023. The central bank had kept rates elevated for most of 2024 to combat inflation, but concerns about a potential recession prompted the rate cut, bringing it down to a range of 4.75% to 5.00%. Fed Chair Jerome Powell cited a weakening labor market as a key factor in the decision, marking the first rate reduction since March 2020, when the pandemic triggered a 100-basis point cut.

These monetary policy changes, coupled with lingering economic effects from the pandemic, continue to affect Los Angeles County’s commercial real estate market. Sales are further limited by taxes and government fees, particularly Measure ULA, the property transfer tax in the City of Los Angeles that took effect on April 1, 2023. Initially dubbed the ‘Mansion Tax,’ Measure ULA imposes a 4% tax on real estate transactions over $5 million and a 5.5% tax on those exceeding $10 million. By June 30, 2024, these thresholds had increased to $5.15 million and $10.3 million. The tax has contributed to significant year-over-year sales declines across property types:

- Industrial: -63.2%

- Office: -45.1%

- Retail: -32.6%

- Multifamily: -14.8%

This led to a 39.8% year-over-year drop in sales, or $1.9 billion below last year’s total, in the City of Los Angeles.

Los Angeles County Commercial Real Estate Sales Market Q3 2024 Statistics

Heading into election season, multifamily investors are cautious about Proposition 33, which seeks to repeal the Costa-Hawkins Rental Housing Act and expand rent control in California. Proponents argue the measure will provide greater tenant protections, while opponents fear it could worsen the state’s housing shortage by discouraging development and lowering property values. If passed, cities could impose rent control on more housing types, including single-family homes and newer apartments, significantly impacting the multifamily market in Los Angeles County, home to nearly 10 million residents.

LA’s industrial market, centered around the ports of Los Angeles and Long Beach, gained national attention during the recent East Coast port strike. However, AB 98 now threatens this vital industry by imposing regulations that could stifle growth, limit warehouse development, and impact local jobs. Governor Newsom signed AB 98 on September 29th, with the new law taking effect on January 1, 2025.

Meanwhile, retail bankruptcies are on the rise, driven by revenue loss and aggravated by higher supply chain and labor costs. California’s fast-food minimum wage increase to $20 an hour is the latest hurdle. Since the wage hike took effect in April—representing a 25% increase from the previous $16 an hour—fast-food franchises have been cutting worker hours, raising concerns for investors in net-leased properties, typically considered stable investments.

Taxation and regulation are significant factors influencing investment decisions, but interest rates and borrowing costs are equally crucial as the Fed remains focused on controlling inflation. Industrial property prices, though resilient, have come down from all-time highs, as rising interest rates slow sales.

The multifamily sector faces a less optimistic growth outlook due to increased borrowing costs and government regulation, adding financial risks. Still, certain asset classes continue to see strong demand despite these challenges.

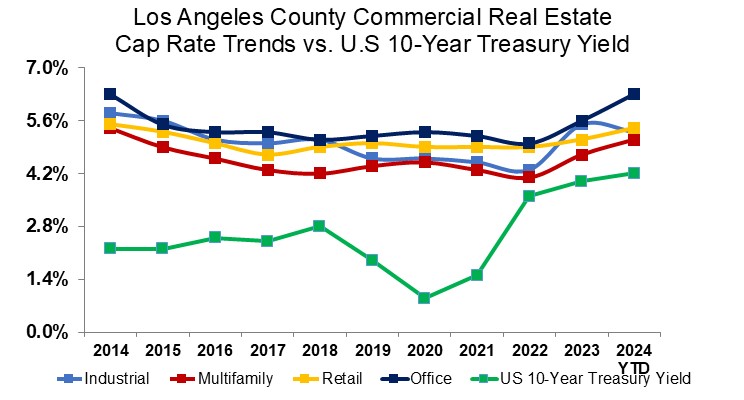

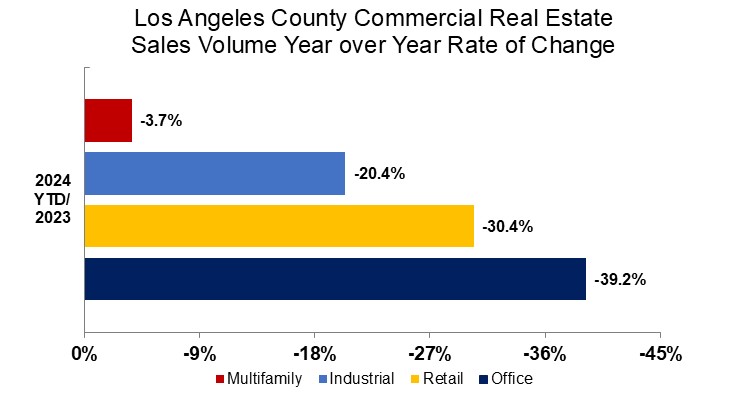

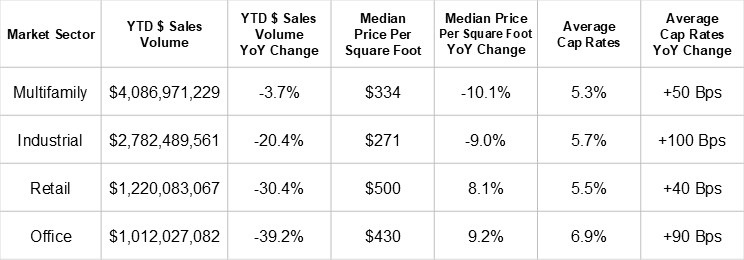

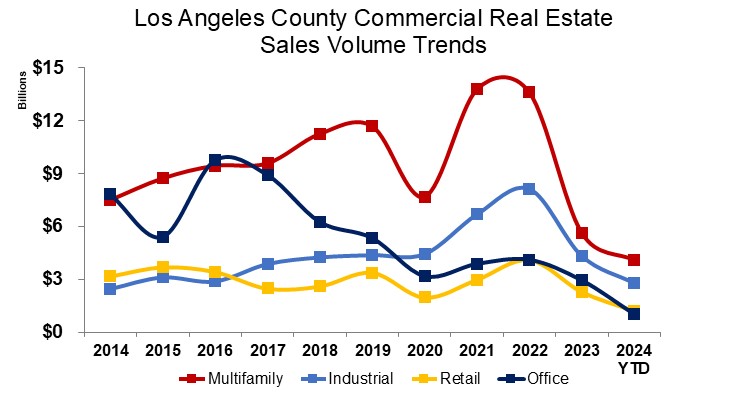

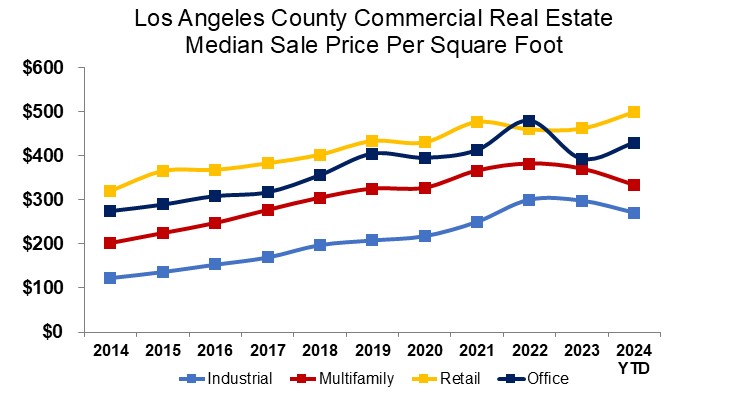

The median sale price per square foot for multifamily buildings declined by 3.3% quarter-over-quarter and 10.1% year-over-year. However, lower prices spurred a 25.0% increase in sales volume from the previous quarter, with year-to-date numbers just 3.7% below last year’s, indicating sustained investor demand for multifamily assets. The average capitalization rate also rose by 50 basis points compared to last year, now standing at 5.3%, as investors respond to price discovery and regulatory risks such as rent control.

Industrial building sales, though resilient, declined 20.4% year-to-date, driven by falling lease rates, higher borrowing costs, and a slowing economic outlook that led owner-users, small businesses, and investors to reconsider transactions. The median sale price per square foot for industrial buildings dropped 16.6% quarter-over-quarter and fell 9.0% year-over-year. This market adjustment pushed the average capitalization rate up by 100 basis points from last year, now at 5.7%.

Retail building sales, as brick-and-mortar stores continue their recovery, recorded $1.22 billion in year-to-date sales volume—still 7.7% below 2020’s pandemic low. The retail sector has a long way to go to reach “normal” levels, with mixed outlooks across product types. The median sale price per square foot dropped 1.5% quarter-over-quarter but rose 8.1% year-over-year, reflecting the varied performance within retail.

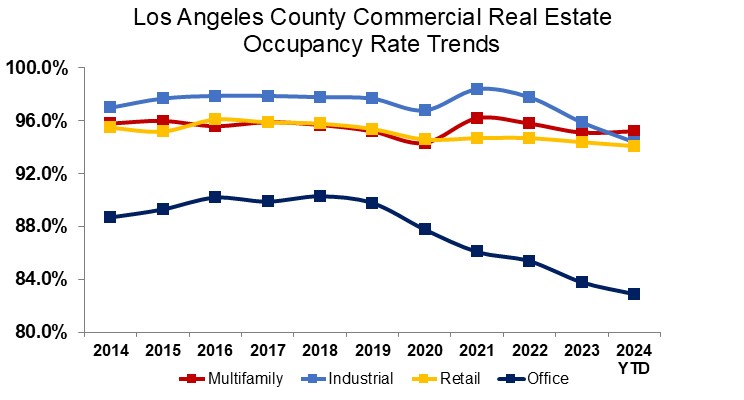

The office market in Los Angeles County continues to face a slow recovery. Landlords are offering substantial concessions, such as rent reductions and tenant improvement allowances, to attract tenants, further eroding market values. Year-to-date office building sales dropped by 55.4% compared to Q3 2020, totaling $1.01 billion, making it the worst-performing asset class in Los Angeles County. Despite this, the median sale price per square foot rose 9.2% year-over-year, and the average cap rate of 6.9% suggests the office sector may be approaching its trough as it adjusts to risk and interest rates.

According to Thomas Preston, Senior Managing Director, and Head of Capital Markets at NAI Capital Finance, “The Fed plays an important role in monetary policy, which is highly visible to property owners. However, unemployment, inflation, and geopolitical events also influence consumer confidence, even in a favorable rate environment. Banks and institutional lenders still face challenges in resolving the office space crisis—it is a crisis. Balance sheets are under pressure with limited solutions for half-empty office towers. Aside from these ‘Black Swan’ office buildings, commercial real estate is in good health. Retail has rebounded, industrial remains strong despite mild value adjustments, multifamily is highly sought after, and construction remains active despite higher borrowing rates. Investment sales professionals will need to adjust as monetary and fiscal policies continue to evolve.”

Though the labor market had been cooling, with unemployment in Los Angeles County rising to 5.6% in August 2024 from 5.5% in July, the U.S. Labor Department’s September data shows stronger-than-expected job growth, with the national unemployment rate at a three-month low of 4.1%, alongside accelerated wage growth. These factors reduce the likelihood of another significant Fed rate cut in November. While this may deter further reductions, upward pressure on cap rates suggests continued pricing challenges in the commercial real estate market. As Los Angeles County’s commercial real estate sector adapts to these evolving challenges, investors are closely monitoring key regulatory developments and economic fundamentals shaping the outlook as 2024 ends and 2025 comes into focus.