First Quarter 2025

Orange County Industrial Market Cools as Vacancies Rise and Rents Dip in Q1 2025

Despite persistent surges in sales and construction, softening leasing activity and economic uncertainty are signaling a shift toward a tenant-favorable industrial market.

Investment demand remains resilient even with high interest rates and elevated prices, while the rent growth that once fueled construction has moderated.

MARKET OVERVIEW

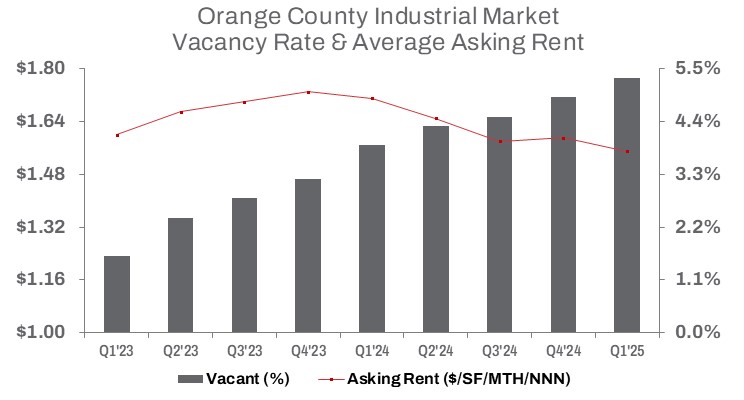

In Q1 2025, industrial vacancy rates in Orange County continued to climb, rising 40 basis points quarter-over-quarter to reach 5.3%—a 140-basis point increase from Q1 2024. Over the past two years, approximately 5 million square feet of new industrial space has been completed, while net absorption has been negative 4.7 million square feet, signaling a shift in the market’s trajectory.

Completed construction surged in Q1, more than tripling from the previous quarter and rising 4.0% year-over-year, with 652,424 square feet delivered. Goodman Group completed buildings 1 and 2 at Goodman Commerce Center Cypress, adding 390,268 square feet of vacant space. This pushed the West submarket’s vacancy rate up 110 basis points quarter-over-quarter to 5.3%. Demand for warehouse space remains largely driven by e-commerce, but leasing velocity has slowed. Meanwhile, space under construction increased 13.0% from Q4 2024 and 77.9% from a year ago, approaching 2.1 million square feet.

Rent growth, which previously fueled construction, has cooled. The average asking rent dipped 2.5% quarter-over-quarter to $1.55 per square foot triple net—a 9.4% decline year-over-year.

On the sales side, continued pent-up demand to own rather than lease, combined with more product coming to market, created buying opportunities. Sales volume rose 39.9% quarter-over-quarter and 60.4% year-over-year, totaling over 1.1 million square feet to start the year. The average sale price dipped 3.8% from Q4 2024 but was up 7.5% from Q1 2024, reaching $326 per square foot.

However, leasing demand softened. Volume fell 30.3% from the previous quarter and 19.7% year-over-year, with 2.2 million square feet leased in Q1 2025.

TRENDS TO WATCH

Tenants are gaining leverage to negotiate more favorable lease terms, signaling a shift in the market dynamic that challenges landlords who previously held more negotiating power. As leasing velocity slows, landlords are responding by offering concessions and more flexible lease arrangements.

E-commerce continues to drive demand, with companies seeking adaptable solutions to accommodate shifting logistics needs. Efforts to reduce excess warehouse space contributed to an 8.9% quarter-over-quarter drop in vacant sublease space. However, sublease availability remains elevated—up 25.9% year-over-year—totaling approximately 1.8 million square feet. This trend suggests opportunities for securing discounted sublease space persist, even as availability begins to tighten.

Ample supply across the market provides companies with options to meet their warehousing needs. Yet, uncertainty is influencing decision-making. According to the Ports of Los Angeles and Long Beach, combined inbound TEU cargo volumes—a key barometer of warehouse demand in Southern California—rose 14.4% year-to-date as of March 2025. Ongoing regulatory concerns, geopolitical tensions, and tariff negotiations with China and Hong Kong—Southern California’s largest trading partner—may prompt some tenants to delay leasing decisions.

Despite high interest rates and elevated pricing, investment demand remains resilient. Sales volume surged at the start of the year, climbing 33.5% quarter-over-quarter and 22.7% year-over-year, exceeding $364 million. A standout transaction in Q1 was the user acquisition by The Walt Disney Company, which purchased a warehouse at 1501–1601 E Cerritos Ave in Anaheim—just 2.9 miles from Disneyland—from JPMorgan Chase & Co. for $124 million, or $304.83 per square foot.

The median sale price per square foot decreased 9.8% quarter-over-quarter but was narrowly up 1.1% year-over-year, reaching $360. With elevated interest rates expected to persist, pricing trends may face further downward pressure in the second half of 2025.