Third Quarter 2024

Orange County Industrial Market Faces Shifts as Vacancy Rates Climb and Construction Slows

As vacancy rates rise and demand softens, industrial space leasing shows mixed results, while sublease activity and price adjustments signal changing dynamics in Q3 2024.

Tenants are gaining leverage to negotiate favorable deals, reflecting a shift in the market.

MARKET OVERVIEW

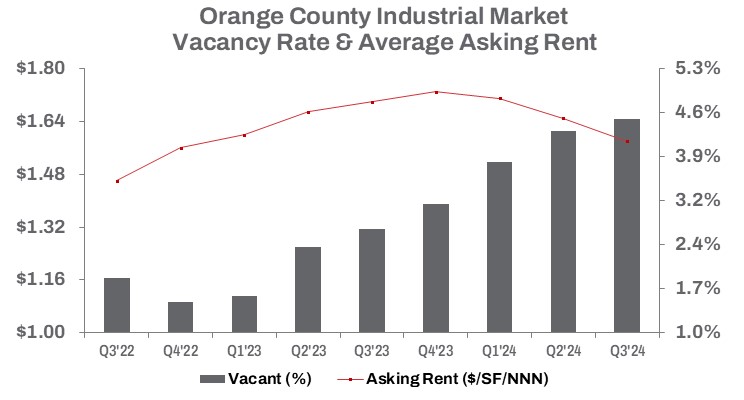

In Q3 2024, the rise in vacancy rates for industrial space in Orange County continued, with a 20-basis point increase quarter over quarter, bringing the rate to 4.5%—180 basis points higher than Q3 2023. Over the past two years, Orange County has added approximately 5.3 million square feet of completed construction, while absorption has resulted in a negative 2.4 million square feet during the same period, signaling the shift in the industrial market’s trajectory.

Space under construction has decreased by 37.4% compared to last year, and dropped by 10.2% from the prior quarter. Completed construction in Q3 2024 also saw a significant decline, down 66.3% quarter over quarter and 2.7% year-to-date, adding just 1.6 million square feet. Developers, once focused on meeting e-commerce-driven demand for warehouse space, have scaled back capacity in response to slowing market conditions.

Once-strong rent growth, which had fueled new construction, has also slowed. The average asking rent in Q3 fell by 4.2% from the previous quarter, reaching $1.58/SF triple net, a decrease of 7.1% year over year.

Opportunities driven by pent-up demand in the first half of the year subsided in Q3, leading to a 27.3% drop in sales volume on a square-foot basis compared to the prior quarter, while the average price per square foot dropped 24.7%. On the leasing side, demand showed mixed results. Leasing volume was up 1.4% quarter over quarter but down 3.2% year over year, totaling 7.9 million square feet year to date—an increase of 2.7% compared to Q3 2023.

TRENDS TO WATCH

Tenants are gaining leverage to negotiate favorable deals, reflecting a shift in the market that poses new challenges for landlords, who have historically driven leasing terms. With leasing velocity slowing, landlords are increasingly adapting to meet tenant needs. The market will continue to be driven by increased options for e-commerce warehousing, with companies seeking flexible solutions to meet evolving demand. Companies actively reducing excess warehouse space have led to a significant rise in vacant sublease space, which increased 22.3% quarter over quarter, though it is only 0.6% higher than Q3 2023, totaling approximately 1.5 million square feet. This suggests the rate of increase in sublease space is slowing compared to a year ago.

The abundance of available industrial space indicates that companies with warehousing requirements still have a variety of options, especially as cargo throughput at the ports remains strong. According to the latest data from the Ports of Los Angeles and Long Beach, combined inbound TEU cargo volumes—a major driver of warehouse demand in Southern California—have increased by 21.4% year-to-date as of September 2024. However, the window for securing sublease space may be slowly closing.

Despite the strong demand, elevated prices and interest rates are affecting industrial building sales, though high-quality space continues to command a premium. Sales dollar volume dropped 45.4% from the previous quarter, driven by market opportunities. A notable transaction this quarter involved Bain Capital, in partnership with L.A.-based Staley Point Capital, acquiring a fully leased 161,738-square-foot manufacturing building in North Orange County for $30.1 million. Built in 1959 and once owned by Hughes Aircraft Company, the property sold for just $2.5 million in 1997, reflecting significant appreciation. The price per square foot of $186 was 35.6% below the average sale price for Orange County industrial space this quarter.

Notably, the average price per square foot declined 24.7% quarter over quarter and saw a 14.5% year-over-year decrease, reaching $289 per square foot. The combination of high interest rates and slowing demand will likely continue to influence pricing.