Third Quarter 2025

Industrial Market Adjustment Continues in Orange County Q3 2025

Rising vacancy and slower leasing defined the quarter, while sales activity remained steady.

Despite market cooling, investors and owner-users remain active, keeping prices stable for quality assets. Tenants continue to gain leverage as developers scale back new projects and construction activity trends lower.

MARKET OVERVIEW

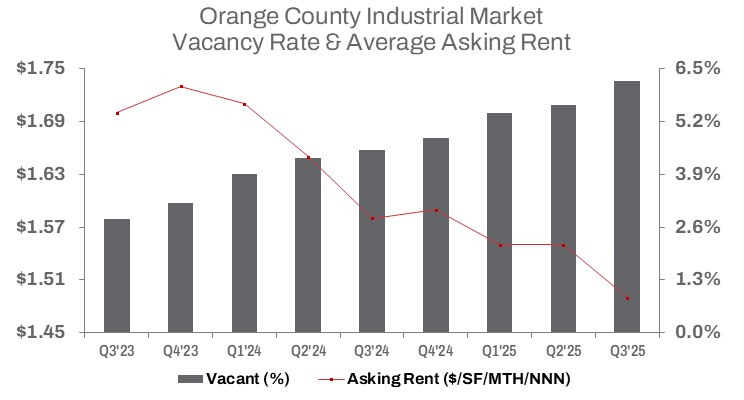

In Q3 2025, vacancy rates for industrial space in Orange County continued to climb, reaching 6.2%, up 60 basis points quarter over quarter and 170 basis points year over year. Net absorption remained negative at 690,229 square feet, contributing to a year-to-date total of 1,947,928 square feet of negative absorption, reflecting ongoing market adjustment after several years of slower growth.

Developers completed 651,931 square feet of new construction this quarter, bringing the year-to-date total to 1,440,573 square feet, a 17.3% quarterly decline and an 8.0% year-over-year decrease, signaling a continued slowdown in construction activity. Space under construction declined 19.7% from the previous quarter but increased 18.7% year over year, totaling 1,990,177 square feet, which underscores developer caution in the face of higher interest rates and softening absorption as the construction pipeline clears.

Rent growth has slowed considerably. The average asking rent edged down to $1.49/SF NNN, down 3.9% quarter over quarter and 5.7% year over year, suggesting landlords are moderating rents in response to softer leasing activity. Leasing volume totaled 2,094,856 square feet, down 40.5% from Q2 2025, with the year-to-date total of 8,076,724 square feet coming in slightly lower than last year’s pace.

Sales activity was mixed. Orange County’s industrial sales volume totaled $313.6 million this quarter, down 18.1% from Q2 2025, while the year-to-date figure of $1.06 billion marked a 64.6% year-over-year increase. The median sale price of $375 per square foot rose 8.8% year over year and 8.1% quarter over quarter, reflecting selective investor demand and price resilience for quality assets, particularly in the North and Airport submarkets, which commanded higher per-square-foot pricing despite broader market softness.

TRENDS TO WATCH

Tenant leverage continues to grow as market conditions shift. With negative absorption and elevated vacancy, landlords and sublessors are increasingly offering concessions and flexible terms to attract tenants. Sublease availability climbed to 1.75 million square feet, up 28.7% quarter over quarter and 3.6% year over year, indicating that while sublease growth has moderated, it rebounded this quarter as companies scaled back excess warehouse space.

High prices and elevated interest rates continue to weigh on industrial sales, though high-quality buildings still command premiums. Year-to-date sales volume on a square footage basis increased 32.2% from the prior year, signaling investors are selectively pursuing opportunities as pricing stabilizes.

A notable transaction this quarter involved Principal, a global financial investment management and insurance firm headquartered in Des Moines, Iowa, completing the sale of 1050 S. State College Blvd in Fullerton within the North Orange County market to Future Foam, the existing tenant. Future Foam, a family-owned company based in Middleton, Wisconsin, specializing in polyurethane foam products for bedding, furniture, carpet cushions, and mattresses, purchased the 417,320-square-foot industrial building for $145 million ($347 per square foot) and plans to continue operations at the site. The deal underscores the continued strength of the owner-user segment in Orange County’s industrial market.

According to the latest data from the Ports of Los Angeles and Long Beach, combined inbound TEU cargo volumes, a key driver of warehouse demand in Southern California, rose 3.7% year to date as of September 2025. While tariff concerns prompted importers to place orders earlier, cargo volumes have remained resilient. The window for securing sublease space remains open, and strong port throughput paired with elevated space availability continues to support warehouse demand. However, high interest rates and slowing absorption are tempering speculative investment. Prices are expected to stabilize in the coming quarters, with top-quality assets maintaining premiums while older or less ideally located properties face downward pressure.

Tenants are gaining leverage to negotiate favorable terms, marking a shift in a market long dominated by landlords. As leasing velocity slows, landlords are adjusting strategies to meet tenant requirements. The market will continue to be shaped by e-commerce warehousing demand and companies seeking flexible, cost-efficient space solutions.

The abundance of available industrial space ensures that tenants with warehousing needs still have a range of options, especially as port activity remains robust. The combination of high borrowing costs and moderating demand will likely continue to influence pricing in the near term.