First Quarter 2025

Q1 2025 Marks Orange County Multifamily Market in Transition

Declining sales volume and stable rents underscore market resilience as investors target long-term opportunities.

Sales activity declined sharply as elevated borrowing costs continued to challenge investors, leading to smaller average deal sizes.

MARKET OVERVIEW

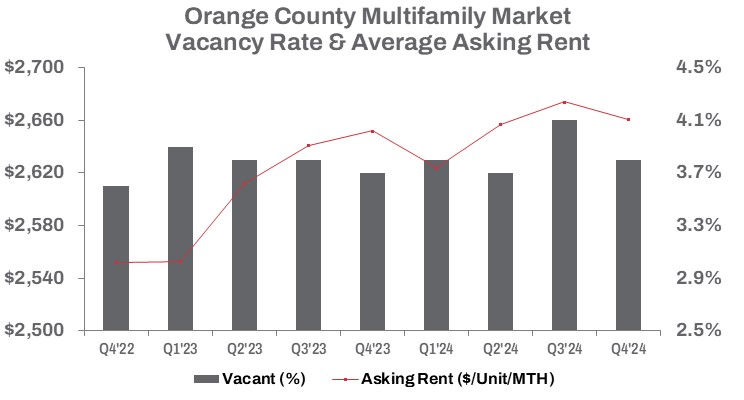

In Q1 2025, Orange County’s multifamily market showed signs of adjustment in response to economic shifts. The number of vacant units decreased 0.2% quarter-over-quarter to 12,199, but rose 4.2% year-over-year. The vacancy rate increased to 3.9%—10 basis points above the level a year ago. The modest quarterly shift in vacant units contrasts with the larger annual increase, suggesting steady but softening rental demand as new supply enters the market.

Despite new unit deliveries doubling quarter-over-quarter, developers delivered only 426 new units—a 31.5% drop from Q1 2024—highlighting continued supply constraints. Tighter financing and conservative builder sentiment, driven by demand uncertainty, contributed to the slowdown. Average asking rents fell 0.9% from Q4 to $2,684 per unit, yet remained 2.4% above last year’s peak. High interest rates, rising construction costs, and a cooling economy weighed on growth.

Currently, 6,328 units are under construction—up 1.4% from Q4 but down 20.1% year-over-year—signaling developer restraint in the face of high borrowing costs. Still, the active pipeline reflects confidence in sustained rental demand, underpinned by Orange County’s persistent homeownership affordability challenges.

Sales activity declined sharply. Q1 transaction volume dropped 59.0% from Q4 2024 and 57.9% year-over-year to $252 million. The number of units sold fell 21.4% from the previous quarter and 24.9% from a year ago. The average price per unit rose 0.3% from Q4 to $325,284 but was down 27.6% year-over-year. This softening in deal volume and pricing reflects investors stepping back and sellers adjusting expectations—though buyers remain focused on long-term rental growth opportunities.

TRENDS TO WATCH

Orange County’s multifamily market remains resilient, supported by employment trends and homeownership affordability challenges that maintain rental demand, though at a slower pace. Rising borrowing costs have increased financial risks, yet select asset classes continue to attract capital, even as growth prospects weaken.

In Q1 2025, multifamily transaction activity was subdued, but standout deals included the two largest sales by unit size. The largest was Park Vista, a 394-unit Class C complex in North Anaheim, built in 1958 and renovated in 2021. It sold to BLDG Partners, a national residential developer, for $274,112 per unit, highlighting the market’s appeal for stable returns and value-add opportunities. The seller, Aimco, a public REIT, purchased the property “as is” in 2000 for $69,337 per unit, reflecting significant value appreciation. The second largest sale by unit size was Alwood Garden, a 16-unit property at 9602-9612 Alwood Ave. in Garden Grove, sold in Q1 for $290,625 per unit. Acquired by a private investor, the property’s 2025 net operating income was $237,150, yielding a 5.10% cap rate. These transactions highlight the market’s appeal to diverse investors, from large-scale developers to private buyers, despite broader market challenges.

Elevated borrowing costs are challenging investors, with the average deal size dropping to $4,060,679 in Q1 2025—a 47.1% decline from Q4 2024 and 69.5% below Q1 2024’s $13,300,722, when capital markets were more robust. With rents stabilizing, inflation easing, and interest rates expected to decline, investors maintain measured confidence. However, mortgage rates near their highest since 2002 and elevated home prices continue to limit homeownership, supporting rental demand. Slower rent growth may pressure pricing, leading investors to focus on select assets and long-term fundamentals.