Third Quarter 2024

Orange County’s Multifamily Real Estate Market Adapts to Shifting Trends in 2024

The Fundamentals Remain Steady as Economic Shifts and Transaction Volumes Decline.

Homeownership has become out of reach for many borrowers, further driving demand in the rental market.

MARKET OVERVIEW

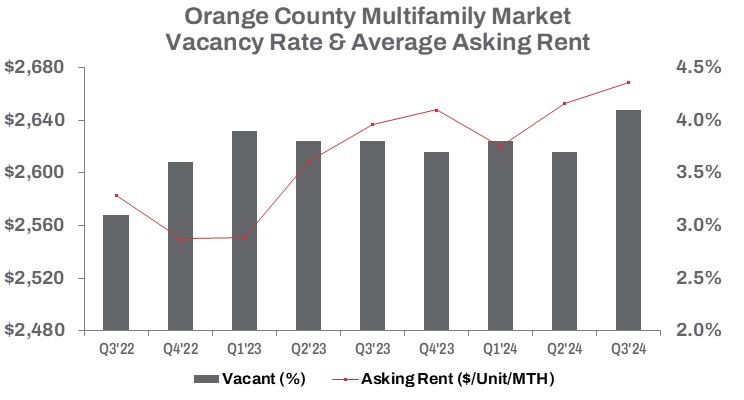

In Q3 2024, vacant multifamily housing units in Orange County increased by 10.4% quarter-over-quarter and 8.8% year-over-year, with the vacancy rate rising to 4.1%. Developers added 2,362 new units to the inventory during the quarter, a 97.0% increase compared to the same period in 2023. These trends reflect ongoing adjustments in demand and supply, with newly completed units contributing to higher average asking rents. Although the rent increase was modest—0.6% quarter-over-quarter and 1.2% year-over-year—the average rent reached an all-time high of $2,669 per unit per month.

Year-to-date, developers have delivered 3,294 units, underscoring the challenges facing multifamily development in expanding inventory. These challenges are evident in rising vacancy rates, which increased by 40 basis points quarter-over-quarter and 30 basis points year-over-year, reaching 4.1%. Additional constraints, such as high interest rates, rising construction costs, a slowing economy, and subdued rent growth, continue to slow new construction. As of Q3 2024, only 5,612 units were under construction—a sharp 29.6% decrease quarter-over-quarter and a modest 3.3% increase compared to Q3 2023.

Despite these headwinds, sales activity in Q3 2024 presented a mixed picture. Transaction volume fell sharply, down 49.9% quarter-over-quarter. However, year-to-date sales volume increased by a solid 19.9% compared to the previous year’s low, exceeding $1.2 billion. The average sale price per unit dropped by 30.6% quarter-over-quarter and 21.7% year-over-year, settling at $311,499. Regionwide, the total number of units sold year-to-date in Q3 2024 increased by 31.9% compared to the same period in 2023. Additionally, the average capitalization rate rose by 30 basis points year-over-year, reaching 4.5%.

TRENDS TO WATCH

The fundamentals in Orange County’s multifamily market will remain steady, adjusting to economic shifts, employment trends, and the lack of homeownership affordability, which continues to drive rental market growth, albeit at a slower pace. While rising borrowing costs have increased financial risks, demand persists in certain asset classes, though growth prospects appear more tempered.

In Q3, the Orange County multifamily market recorded only one sale of a building with over 100 units: The Arbors, a 160-unit apartment complex at 1100-1200 E. Fairhaven Ave. in Santa Ana, North Orange County. The property sold for $40.75 million in August, reflecting significant appreciation for the seller, who originally purchased it in 2013 for $28 million. However, transactions of this size have been on a downward trend, with four sales recorded in Q1, three in Q2, and four during the same period last year.

Investors are responding to the costs of borrowing, as reflected in the decline of the average deal size, which fell to $3,885,237 in Q3 2024—a 64.5% drop from the prior quarter and a 74.8% decrease year-over-year. With rents unlikely to drop, inflation continuing to moderate, and interest rates poised to come off recent highs, both investors and developers are becoming cautiously optimistic. The multifamily housing market will continue to adjust based on the direction of the overall economy and mortgage rates. With mortgage rates hovering near the highest levels since 2002 and prices rising, homeownership has become out of reach for many borrowers, further driving demand in the rental market. However, lower rent growth will impact pricing as investors adjust to new market realities.