Fourth Quarter 2024

Orange County Multifamily Sees Steady Fundamentals, Shifting Dynamics

Investors fueled a Q4 sales boom as developers hit the brakes on new projects.

Sales activity told a different story. Q4 transaction volume soared 182.8% quarter-over-quarter, and year-to-date sales climbed 19.9% to nearly $1.9 billion

MARKET OVERVIEW

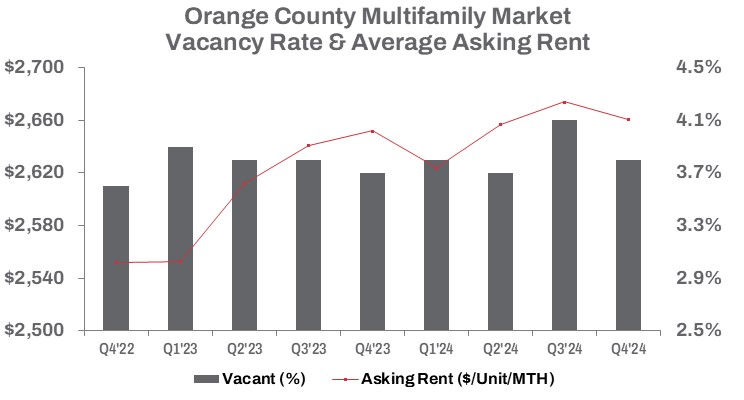

In Q4 2024, Orange County’s multifamily market showed signs of adjustment. Vacant units fell 6.9% quarter-over-quarter to 11,902 but rose 3.9% year-over-year. Developers added just 86 new units during the quarter—a 60% drop from Q4 2023—highlighting supply constraints. This slowdown reflects not only tighter financing conditions but also a cautious approach from builders facing uncertain demand signals. Vacancy rates reflected this push-and-pull, dipping 30 basis points from Q3 to 3.8%, yet up 10 basis points from last year. Despite the quarterly dip, the annual uptick suggests rental demand, while still solid, is softening slightly amid new deliveries.

Average asking rents eased 0.5% from Q3 to $2,661 monthly per unit, down from the prior quarter’s peak, with a modest 0.3% gain year-over-year. Year-to-date, 3,380 new units hit the market, but high interest rates, rising construction costs, and a cooling economy slowed momentum. Only 6,316 units remain under construction—down 1.1% from Q3 and 4.2% from Q4 2023. Developers are grappling with elevated borrowing costs, slowing new multifamily projects. Still, the pipeline, though shrinking, signals confidence in long-term rental demand driven by Orange County’s persistent affordability challenges.

Sales activity told a different story. Q4 transaction volume soared 182.8% quarter-over-quarter, and year-to-date sales climbed 19.9% to nearly $1.9 billion. As investors snapped up units and sellers adapted to a shifting economic landscape, units sold year-to-date surged 32.3% over 2023. The average price per unit settled at $380,897—down 3% from Q3 but up a robust 16.8% year-over-year. This Q4 sales spike was fueled partly by institutional buyers targeting well-located assets, betting on sustained rental growth despite economic headwinds.

TRENDS TO WATCH

The fundamentals in Orange County’s multifamily market remain steady, adjusting to economic shifts, employment trends, and persistent homeownership affordability challenges that continue to drive rental demand—albeit at a slower pace. Rising borrowing costs have heightened financial risks, yet demand persists in select asset classes, even as growth prospects moderate.

In Q4, the market recorded just two sales of buildings with over 100 units. One standout was The Royce Park Place, a 520-unit complex built in 2018 in Irvine, which traded to MetLife for $475,962 per unit—demonstrating the market’s appeal to capital seeking stable returns. Another key deal was Horizon Apartment Homes, a 406-unit property at 2414 N Tustin Ave. in Santa Ana, sold for $129.2 million in October. The seller, a private equity firm, saw a significant gain, having purchased the property in 2007 for $74.3 million. While these transactions reflect resilience, deal volume for properties over 100 units rose 80% year over year, increasing from 10 in 2023 to 18 in 2024.

Yet, investors are feeling the strain of higher borrowing costs. The average deal size dropped to $8,367,218 in 2024—a 64.5% decline from 2023 and 38.9% below the 2022 peak of $13,704,147, when interest rates were at historic lows. With rents stable, inflation moderating, and interest rates set to ease, investors and developers remain pragmatically hopeful. However, with mortgage rates near their highest since 2002 and home prices still elevated, homeownership remains out of reach for many, sustaining rental demand. Still, slower rent growth will weigh on pricing as investors adjust to evolving market conditions, emphasizing select assets and long-term fundamentals.