Fourth Quarter 2025

Fundamentals Hold Steady as Growth Moderates in Orange County’s Multifamily Market

A sharp pullback in new construction stabilized vacancy, while rents eased and late-year sales activity reflected selective investor confidence.

Vacancy stabilized, rents pulled back slightly, and institutional buyers remained active in well-located assets.

MARKET OVERVIEW

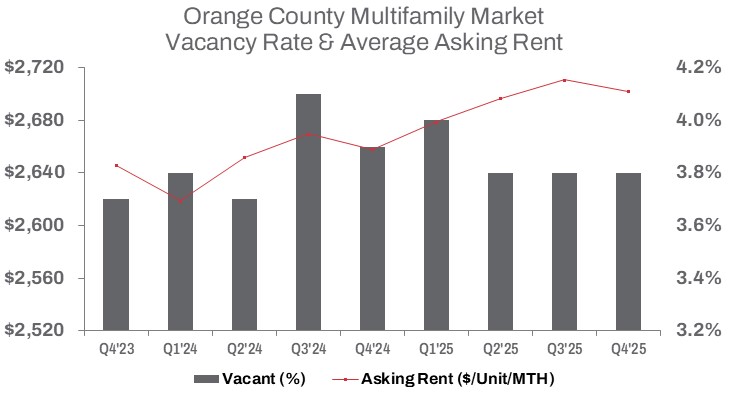

In Q4 2025, Orange County’s multifamily market showed clear signs of adjustment. Vacant units inched up 0.1% quarter-over-quarter to 11,926 but declined 1.6% year-over-year, reflecting a gradual easing in supply pressure. Developers delivered just 430 new units during the quarter, a 26.2% drop from Q3 2025, bringing year-to-date deliveries down 43.1% to 1,979 units. This slowdown reflects tighter financing conditions and a more cautious development posture as builders respond to mixed demand signals.

Vacancy rates mirrored this supply restraint, holding flat at 3.8% from Q3 while improving 10 basis points year-over-year. The limited movement suggests rental demand remains intact, even as absorption softened slightly alongside new deliveries.

Average asking rents edged down $9.00 from Q3 to $2,702 per unit, retreating from the prior quarter’s peak, though rents still posted a 1.7% year-over-year increase. For context, 3,475 new units were delivered year-to-date in 2024, compared with 3,277 units in 2023, underscoring that last year marked a recent development peak. Since then, higher interest rates, rising construction costs, and a cooling economy have slowed momentum. Only 4,775 units remain under construction, down 11.1% from Q3 and 14.4% from Q4 2024, signaling continued pressure on the future pipeline. Still, the remaining development activity reflects long-term confidence in Orange County’s rental demand, supported by persistent affordability challenges.

Sales activity told a mixed story. Q4 transaction volume rose 18.1% quarter-over-quarter, while year-to-date sales declined 15.2% to nearly $1.9 billion. Investors acquired 5,231 units during the year, though units sold were down 9.9% compared to 2024 as sellers adjusted to shifting pricing expectations. The average price per unit settled at $386,605, down 11.1% from Q3 but up 1.7% year-over-year. The late-year sales pickup was driven in part by institutional buyers targeting well-located assets, betting on long-term rent growth despite ongoing economic headwinds. Notably, 11 transactions of 100 units or more closed in 2025, compared with 10 in 2024.

TRENDS TO WATCH

The fundamentals in Orange County’s multifamily market remain steady as the sector adjusts to economic shifts, employment trends, and persistent homeownership affordability challenges that continue to support rental demand, albeit at a slower pace. Rising borrowing costs have elevated financial risk, yet demand persists for select asset classes even as growth prospects moderate.

In Q4, the market recorded just four sales of properties with more than 100 units. One notable transaction highlighting Orange County’s affordability pressures was the sale of a 333-unit senior housing community by LOMCO and Las Palms Housing to Redwood and Hearthstone Housing Foundation for $160 million, or $480,480 per unit. The property exclusively serves residents aged 62 and older, with all units restricted to households earning up to 60% of area median income (AMI). These affordability restrictions began in 2002 and are scheduled to expire in 2032.

Another key deal was The REVO apartments, located at 1912 S. Jacaranda Street in Anaheim, which were included in a multi-state stabilized portfolio sale to Griffis Residential. REVO comprises 332 units and traded for $152.19 million, or $460,693 per unit, making it the highest-priced asset in the portfolio on a per-unit basis and underscoring the relative strength of Orange County pricing.

The broader transaction included stabilized multifamily communities in Texas and Washington, totaling 1,421 units across the portfolio. The buyer indicated plans for only minimal upgrades across the assets, and the reported cap rate for the overall sale was 4.75%.

Together, these transactions point to continued resilience at the upper end of the market, even as overall deal activity remains constrained by higher borrowing costs. The average deal size fell to $5.4 million in 2025, a 44.6% decline from 2024 and 59.8% below the 2022 peak of $13.5 million, when interest rates were significantly lower. While rents have stabilized and inflation has moderated, slower rent growth is expected to weigh on pricing as investors remain selective, prioritizing long-term fundamentals and well-positioned assets as market conditions evolve.