First Quarter 2025

Orange County Office Market Repositions as Leasing Slows, Sale Prices Rise

Smaller deals and rising sublease demand are shaping the early 2025 office market in Orange County, as vacancy continues to decline.

The ongoing shift from remote work to in-office arrangements supported cumulative positive net absorption.

MARKET OVERVIEW

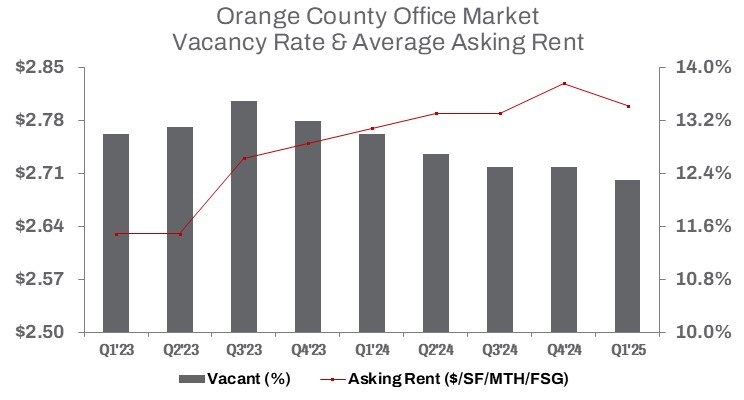

During the first quarter of 2025, the Orange County office market showed signs of improvement, with 101,380 square feet of positive net absorption quarter over quarter. This growth reduced the vacancy rate to 12.3%, a 70-basis-point decline year over year, bringing total vacant space down to approximately 18.1 million square feet at the start of the year.

The ongoing shift from remote work to in-office arrangements supported cumulative positive net absorption of approximately 700,000 square feet since Q1 2024. Sublease activity remained a significant driver, accounting for 74.5% of the quarter’s net absorption. Vacant sublease space declined 3.8% quarter over quarter and 10.7% year over year to about 1.9 million square feet—falling at a faster rate than direct space availability. Direct vacant space decreased by 1.0% quarter over quarter and 5.4% year over year to approximately 17.3 million square feet.

Office sales volume reached approximately 1.8 million square feet in Q1, down 26.6% from the prior quarter. However, the average sale price climbed 24.1% to $240 per square foot, rebounding from the distressed sales seen in Q4 2024.

While challenges remain in achieving a full post-pandemic recovery, occupancy continues to improve gradually. The average asking rent declined slightly by $0.03 quarter over quarter to $2.80 per square foot on a full-service gross basis, yet still stood 1.1% higher than a year ago.

Leasing activity totaled approximately 1.8 million square feet in Q1—down 26.6% from Q4 2024 and 24.4% year over year—marking the lowest first-quarter leasing volume on record. Still, leasing managed to contribute positively to overall market performance, driven by renewals and increased demand, with landlords offering concessions and flexible terms to secure tenants.

TRENDS TO WATCH

Direct leasing activity in Orange County’s office market lost momentum in Q1 2025, with tenants leasing approximately 1.6 million square feet on a direct basis—a 31.0% decline quarter over quarter and 23.8% below Q1 2024. This slowdown is expected to place downward pressure on asking rents and shake landlord confidence moving forward. However, high tenant improvement costs continue to challenge owners, creating opportunities for tenants willing to adapt to existing sublease space— especially as the flight to quality continues.

The Airport submarket, which holds the largest share of Class A office space, is well positioned to capture this demand. It accounts for 44.1% of Orange County’s vacant sublease inventory—approximately 850,000 square feet. Asking rents for Class A sublease space in the Airport submarket average $1.93 per square foot on a full-service gross basis—$1.26 (or 39.5%) lower than direct space—highlighting notable savings for cost-conscious tenants seeking quality space.

Across Orange County, the average asking rent for Class A sublease space is $1.89 per square foot—$1.24 (or 39.6%) below direct space—indicating a growing trend toward subleasing as tenants pursue greater value. The South submarket offers some of the best deals, with Class A sublease rents averaging $1.83 per square foot—$1.30 (or 41.5%) less than direct asking rents in the same area. This pricing gap reflects a broader market push to stimulate demand, as sublessors look to recapture costs before lease expirations.

On the sales side, market activity continued to shift. Roughly 1.2 million square feet traded in Q1 2025—a 32.1% drop from Q4 2024 and 6.3% below the year-ago quarter. The average building size sold declined by 11.4%, from 36,936 square feet to 32,736 square feet. Total sales volume fell 23.7% quarter over quarter, totaling just over $228 million to start the year.

These figures point to a growing preference among investors and owner-users for smaller, more manageable properties. The sharp declines in both sales volume and average building size signal a market in transition, with buyers refining acquisition strategies and waiting for more favorable conditions. Together, these shifts underscore a broader recalibration, as both tenants and investors adapt to evolving economic and market realities.