Third Quarter 2025

Orange County Office Market Reaches Turning Point in Q3 2025

Recovery is confirmed as vacancy tightens, net absorption swings positive, and asking rents stabilize.

Leasing and occupancy gains point to renewed tenant confidence as the market stabilizes and investors favor smaller, high-quality assets.

MARKET OVERVIEW

The Orange County office market showed clear signs of stabilization and gradual improvement during the third quarter of 2025. Q3 activity generated 474,201 square feet of positive net absorption, successfully reversing the year-to-date total into positive territory at 28,903 square feet.

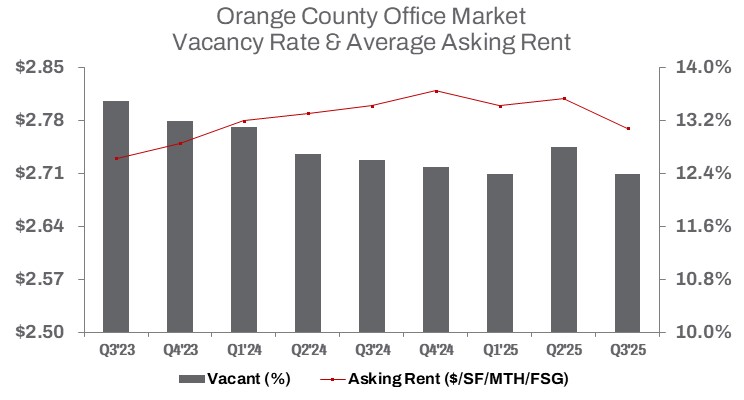

This positive momentum drove the overall vacancy rate down 40 basis points quarter-over-quarter to 12.4%, an improvement of 20 basis points from one year ago. The market currently has 19.3 million square feet of vacant office space, down slightly from the previous quarter.

However, the recovery remains tempered by vacant sublease space, which increased 9.4% quarter-over-quarter to total 1.9 million square feet, despite remaining 1.9% lower year-over-year. On a direct basis, office space vacancy remains 18.8% higher than the Q3 2020 rate, underscoring the enduring structural impact of the pandemic on space utilization. Nevertheless, the market is trending positively as new leasing successfully outpaced newly vacated supply additions, resulting in shrinking direct vacancy and showing further signs of stabilization.

On the construction side, no new office projects were completed during the quarter, keeping year-to-date completions at 176,711 square feet. Space under construction continues to decline, totaling 414,308 square feet, down 11.1% year-over-year. Developers continue to exercise caution, focusing on build-to-suit and pre-leased projects rather than speculative construction.

Leasing activity modestly moderated, with 1.99 million square feet leased during Q3, down 4.2% quarter-over-quarter. Year-to-date leasing totaled 5.86 million square feet, reflecting an 18.0% decline from the same period last year. The average asking rent across the county edged down to $2.77 per square foot full-service gross, a 1.4% decline quarter-over-quarter and a 1.1% decrease year-over-year.

Office sales volume fell sharply in Q3, totaling 681,768 square feet, a drop of 58.5% quarter-over-quarter. Despite this sharp slowdown, the year-to-date square footage remains substantial at 3.54 million square feet, up 39.1% from the prior year. However, the total year-to-date sales dollar volume reached only $759.6 million, representing a 9.1% annual decline.

This disparity suggests a flight to quality and smaller transactions. The average building size sold in Q3 shrank to 24,349 square feet, a 39.2% decline quarter-over-quarter and 4.0% year-over-year. Reflecting demand for premium product, the median sale price climbed to $367 per square foot, while the average sale price rose to $263 per square foot, indicating that smaller, higher-quality assets continue to attract investor interest.

TRENDS TO WATCH

As market conditions continue to shift, tenants are gaining leverage. The ongoing surplus of available office space—combined with limited new construction—has prompted landlords to offer more competitive terms, including rent reductions, flexible lease structures, and higher tenant improvement allowances. Sublease availability, while elevated, has begun to stabilize at 2.85 million square feet, down 18.1% year-over-year. The slower pace of new sublease listings points to growing stability, with tenants increasingly opting to occupy rather than offload space. While overall asking rents softened slightly, the decline in rents appears to be fueling tenant demand within key submarkets. Rents in the South submarket—a regional hub of quality suburban office space—declined 4.9% quarter-over-quarter and 3.9% year-over-year. This price adjustment likely served as a demand catalyst in the South submarket. The submarket went on to capture the majority of Q3’s net absorption, pushing the county’s year-to-date total positive. This strong activity suggests that tenants are prioritizing value-driven opportunities in well-located, suburban, amenity-rich buildings that support hybrid work models.

Investment activity remains constrained as higher interest rates and underwriting scrutiny limit transaction volume. Investors continue to favor smaller, more efficient assets over larger, less adaptable properties. However, pricing has held relatively steady as motivated buyers focus on quality over size.

Looking ahead, the Orange County office market is expected to maintain measured stability through the end of 2025. The combination of modest rent adjustments, declining direct vacancy, and steady leasing activity indicates that the market is gradually recalibrating toward equilibrium after several years of post-pandemic adjustment.