Fourth Quarter 2024

Positive Shifts in Orange County Office Market as Leasing Activity Gains Momentum

Sublease space declines, and smaller properties drive sales as the market adjusts.

This trend toward smaller, more manageable properties suggests that preferences among owner/users and investors are changing in response to the economy.

MARKET OVERVIEW

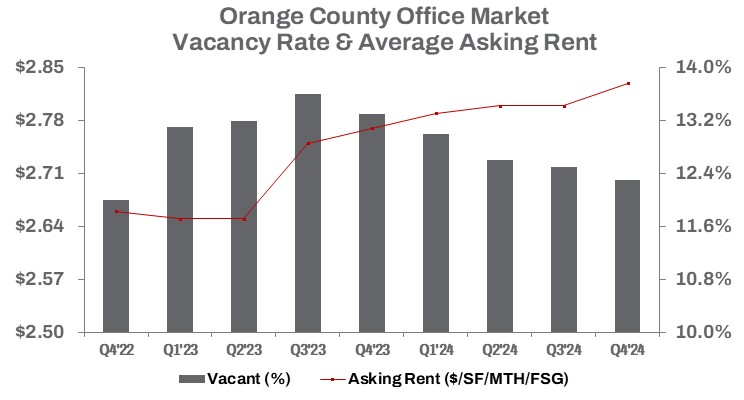

During the fourth quarter of 2024, the Orange County office market demonstrated a healthy performance, with occupied office space increasing by 353,370 square feet quarter over quarter. This solid growth reduced the vacancy rate to 12.3%, reflecting a 100-basis-point decline year-over-year, with more than 110 million square feet of occupied office space recorded.

The gradual shift from remote work to in-office arrangements supported another quarter of positive net absorption, totaling approximately 1.3 million square feet year-to-date. Subleasing continued to play a critical role, contributing to positive net absorption for the fifth consecutive quarter. Available sublease space decreased slightly by 2.1% quarter over quarter and dropped significantly year-over-year, falling 11.9% to 3.4 million square feet—declining at a faster rate than direct office space availability. On a direct basis, office space availability decreased by 2.8% quarter over quarter and fell 4.4% year-over-year to approximately 21.2 million square feet.

By the end of 2024, the Orange County office market had recorded approximately 3.9 million square feet in sales volume, a 33.2% decline from 2023, with average sale prices down 23.4% quarter over quarter to $212 per square foot. Despite lingering challenges in achieving a full post-pandemic return to the office, occupancy rates are gradually improving. The average asking rent increased by $0.03 quarter over quarter to $2.83 per square foot on a full-service gross basis, reflecting a 2.2% year-over-year rise. Leasing volume reached 1.8 million square feet in Q4—21.1% below Q3—but helped push the year-to-date total up by 1.0% compared to the same period last year, nearing 8.6 million square feet. This growth was driven by lease renewals and rising demand, supported by motivated landlords offering concessions and flexible lease terms.

TRENDS TO WATCH

Direct leasing activity for office space in Orange County gained momentum in 2024, with a 5.0% year-to-date increase compared to 2023. Tenants leased approximately 7.9 million square feet of office space on a direct basis, a trend expected to allow landlords to maintain steady asking rents with confidence moving forward. However, the high cost of tenant improvement construction presents challenges for owners, creating opportunities for tenants willing to adapt to available sublease space—particularly amid a flight to quality office space. The Airport submarket, home to the largest concentration of Class A office space, is well-positioned to capture this demand, holding 57.4% of the county’s available sublease space, or 1.5 million square feet. Asking rent for sublease space in the Airport submarket is $2.06 per square foot on a full-service gross basis—30.7% or $0.82 lower than direct space—highlighting potential savings for tenants seeking the right office space.

Amid a significant supply of available office space, signs of a positive shift are emerging, as tenants increasingly turn to subleasing for greater value. With the average asking rent for sublease space in Orange County at $1.96 per square foot—30.7%, or $0.87, lower than direct space—this trend offers tenants valuable opportunities to optimize costs and secure favorable deals in the coming quarters. For those seeking the best value, the South submarket stands out, with sublease asking rents averaging $1.89 per square foot—35.7%, or $1.05, lower than direct space in that submarket. This difference in asking rents between sublease and direct space reflects a broader trend to stimulate office demand as sublessors near lease expirations and seek to recapture sunk costs.

On the sales side, the fourth quarter of 2024 reflected continued shifts, with a 33.2% year-to-date decrease in square footage sold compared to the previous year, totaling 3.9 million square feet. Over the same period, the average building size sold dropped significantly by 25.0%, from 48,098 square feet in Q4 2023 to 36,074 square feet this quarter. Sales volume declined by 30.1%, closing the year at nearly $742 million. This trend toward smaller, more manageable properties suggests that preferences among owner/users and investors are changing in response to the economy. The sharp declines in sales volume and average building size indicate a market in transition, with investors likely holding out for more favorable conditions and refining their acquisition criteria. These changes underscore a period of adjustment, as both investors and tenants adapt their strategies to shifting market conditions.