Fourth Quarter 2025

Orange County Office Market Gains Traction as Vacancy Falls and Investment Rebounds

Positive absorption, declining sublease space, and rising sales activity signal steady improvement.

OC’s office market is turning a corner as occupancy grows and investment activity accelerates.

MARKET OVERVIEW

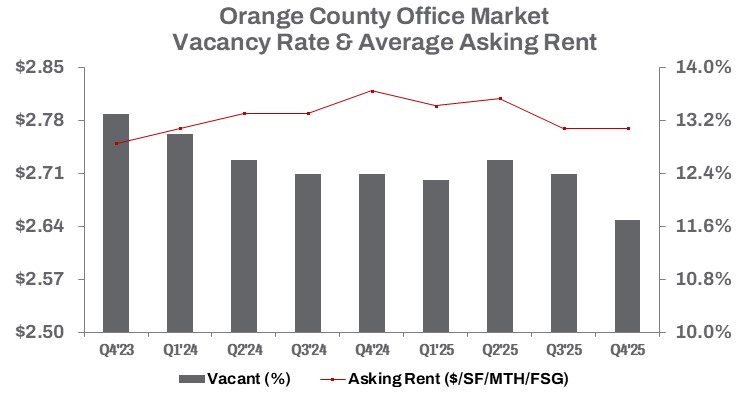

During the fourth quarter of 2025, the Orange County office market delivered a solid performance, with occupied office space increasing by 1,042,440 square feet quarter over quarter. This growth pushed the vacancy rate down to 11.7%, marking a 70-basis-point year-over-year decline and bringing total occupied inventory to nearly 138 million square feet.

A gradual shift from remote to in-office work supported another quarter of positive net absorption, which reached approximately 837,547 square feet year-to-date. Sublease activity continued to play a meaningful role in the market’s recovery. Available sublease space declined 3.2% quarter over quarter and fell 20.4% year over year to roughly 2.7 million square feet, decreasing at a faster pace than direct availability. Direct available space also moved lower, down 3.4% quarter over quarter and 6.7% year over year to about 19.7 million square feet.

By year-end 2025, the market recorded approximately 5.7 million square feet in office sales volume, a 33.3% increase from 2024. Average sale prices rose 8.4% quarter over quarter to $285 per square foot, signaling renewed investor interest. While the market has not fully returned to pre-pandemic occupancy levels and remains about 3.5% below its Q4 2019 benchmark, conditions continue to improve.

Average asking rents held flat quarter over quarter at $2.77 per square foot on a full-service gross basis, representing a modest 1.8% year-over-year decline. Leasing volume approached 2.0 million square feet in the fourth quarter, down 15.3% from Q3, bringing the year-to-date total to roughly 8.2 million square feet, about 15% below the same period last year. Demand remained driven largely by renewals and selective expansions, supported by landlords offering concessions and flexible lease structures.

TRENDS TO WATCH

Orange County’s office market is entering 2026 in a period of recalibration, with tenants and investors focusing on long-term value as pricing and capital structures continue to adjust. Direct leasing activity slowed in 2025, declining 14.7% year to date compared with 2024. Tenants leased approximately 7.7 million square feet on a direct basis during the year, still enough to generate 611,614 square feet of positive net absorption. This modest but meaningful absorption has helped stabilize fundamentals and is expected to support steady asking rents in the near term. Investors are taking note, with many positioning for longer-term opportunities as values reset and debt costs remain elevated.

On the investment side, transaction patterns continue to evolve. The average building size traded decreased 14.8%, from 36,965 square feet in late 2024 to 31,600 square feet in Q4 2025, while total sales volume increased 13.2% to approximately $1.6 billion. The shift toward smaller, more manageable assets suggests that owner-users and private investors are refining acquisition strategies in response to higher financing costs and evolving workplace needs. With values reset and capital repriced, buyers are pursuing selective acquisitions, recapitalizations, and repositioning strategies as fundamentals gradually improve.

Recent transactions illustrate these dynamics. At the FLIGHT at Tustin Legacy campus, Alcion Ventures sold a majority interest in a ten-building portfolio totaling 474,724 square feet to Glendon Capital for $199 million, or about $419 per square foot. Lincoln Property Company retained its ownership stake and continues to operate the campus, which was roughly 85% leased at closing. The structure of the transaction highlights a growing preference for strategic recapitalizations that preserve operational control while introducing new capital at adjusted valuations.

Sale-leaseback activity has also emerged as a tool for occupiers seeking liquidity while maintaining long-term occupancy. The HdL Companies completed a sale-leaseback of Brea Place, its 79,528-square-foot headquarters building, to a private investor for $19.45 million, or roughly $245 per square foot. The property was fully occupied at closing with a weighted average lease term of about 5.5 years, reflecting investor demand for stable cash flow supported by credit tenancy.

Value-driven acquisitions continue as well. In Orange, Granite Properties sold a four-building, 394,000-square-foot campus to MGR Real Estate for $89 million, or approximately $226 per square foot. Although pricing reflected a significant discount to replacement cost, it remained above the prior year’s quarterly average, signaling long-term confidence in Orange County’s leasing fundamentals. The campus, originally built in 1988 and renovated in 2025, was about 84% leased at the time of sale. The buyer plans to maintain operations while refining the tenant mix and implementing targeted improvements.

As 2026 begins, Orange County’s office sector remains in transition. Leasing has moderated but continues to produce positive absorption, while investment activity is increasingly defined by smaller transactions, recapitalizations, and owner-user or sale-leaseback structures. With values reset and financing costs still shaping decision-making, both tenants and investors are expected to remain selective. These dynamics point toward a market focused on stability, operational performance, and long-term positioning as the next phase of recovery takes shape.