Second Quarter 2025

Orange County’s Retail Market Recovery Remains Uneven in 2025

Leasing demand softens, construction slows, and bankruptcies rise, but strategic investments and adaptive reuse point to new opportunities.

Retail vacancies remain elevated while investor confidence diverges—caution defines new development, but well-located assets still draw interest.

MARKET OVERVIEW

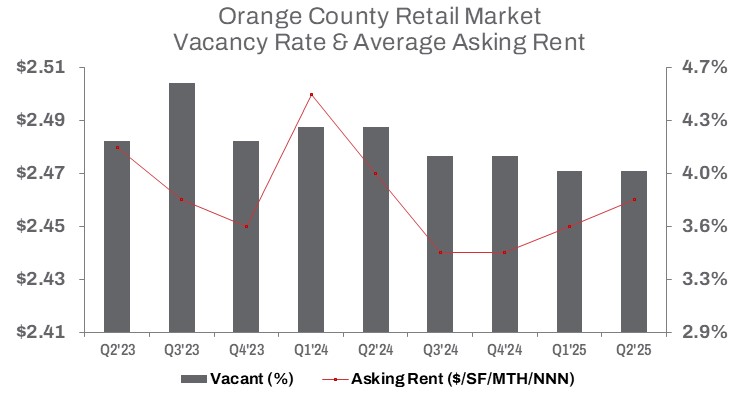

Orange County’s retail recovery in 2025 remains prolonged and uneven, with economic shifts slowing demand for space. Landlords report modest progress as retailers cautiously return to brick-and-mortar locations, constrained by macroeconomic pressures. The retail sector faces significant challenges, including layoffs, bankruptcies, and closures, while fluctuating tariffs heighten economic uncertainty, impacting retail markets. Vacant retail space dropped by 454,000 square feet from Q2 2024, totaling 5.6 million square feet, yet occupancy lags 1.4 million square feet behind Q2 2020, when pandemic-era vacancies surged. The vacancy rate held steady at 4.0%, unchanged quarter-over-quarter but down 30 basis points year-over-year.

Negative net absorption in Q1 and Q2, though minimal, has dampened landlord confidence. Asking rents averaged $2.46 per square foot, up 1 cent from Q1 but down 1 cent year-over-year. Leasing activity fell 31.6% quarter-over-quarter, though year-to-date volume reached nearly 1.5 million square feet, up a mere 0.7% from 2024’s first half. Vacant sublease space increased 1.7% from the previous quarter but remained 1.2% below year-ago levels, indicating limited net change and holding steady above 500,000 square feet.

On the investment side, average sale prices fell 2.3% from Q1 but rose 0.6% year-over-year to $495 per square foot. Sales volume totaled $535 million year-to-date, a 124% surge from the first half of 2024. Meanwhile, retail space under construction declined 13.1% year-over-year, signaling caution in new development.

TRENDS TO WATCH

Consumer spending continues to bolster Orange County’s retail market, prompting investors, retailers, and developers to recalibrate strategies around evolving demand. While challenges persist, interest in well-located assets remains steady.

Occupancy pressures and economic headwinds have forced landlords to offer concessions and reduce asking rents, with some investors selling assets to avoid further price declines. For example, rising interest rates, persistent inflation, and increased tariffs have driven retailers like At Home to file for Chapter 11 bankruptcy, closing 26 stores nationwide by September 30, 2025, including locations at 2505 El Camino Real in Tustin and 2200 Harbor Boulevard in Costa Mesa. At Home’s closures, following six shuttered stores in the past year, align with struggles faced by other big-box retailers like Big Lots, Joann Fabrics, and Party City in 2025. Yet, certain retailers are successfully rebounding from bankruptcy. A blockbuster real estate deal has seen 119 properties housing JCPenney stores across 35 states, including 19 in California and three in Orange County, sold for a staggering $947 million in an all-cash transaction. The sale, under a long-term triple-net master lease with Penney Intermediate Holdings LLC, transfers ownership of the buildings to a new landlord in a move seen as a massive vote of confidence in the future of JCPenney’s 650-store network and brick-and-mortar retail in markets like Orange County.

Opportunistic investors are capitalizing on the current pricing environment. For instance, North Orange County Space Investment Partners, a Southern California-based real estate investment firm, acquired a 395,703-square-foot community retail center at 1375 Harbor Blvd. in Fullerton for $118.5 million—the largest retail asset sale in Orange County in eight years. However, total sales volume fell 53.7% from Q1, with just 1.03 million square feet sold, signaling a slowdown after a robust start to 2025. Still, year-to-date square footage sold surged 301.8% compared to the first half of 2024.

The evolving retail landscape is creating new opportunities. As consumer preferences shift, innovative concepts like experiential retail and mixed-use redevelopment are gaining traction. Developers are embracing lifestyle-oriented designs, integrating entertainment, dining, and cultural elements. Landlords are repositioning older assets with creative tenant mixes tailored to modern shoppers. Forward-thinking players who adapt to these trends will thrive as Orange County’s retail market continues to transform.