Third Quarter 2025

Retail Recovery Strengthens Across Orange County in Q3 2025

Sales volume doubled year-over-year as leasing activity normalized and the countywide vacancy rate reached 3.7%.

Retail fundamentals held firm as renewed absorption highlights market resilience despite economic uncertainty.

MARKET OVERVIEW

Orange County’s retail sector continued its steady recovery through the third quarter of 2025, with leasing activity moderating as retailers and landlords navigated persistent macroeconomic uncertainty. Despite an improving vacancy rate and solid positive absorption, tenant demand remained cautious, reflecting broader consumer and capital market headwinds.

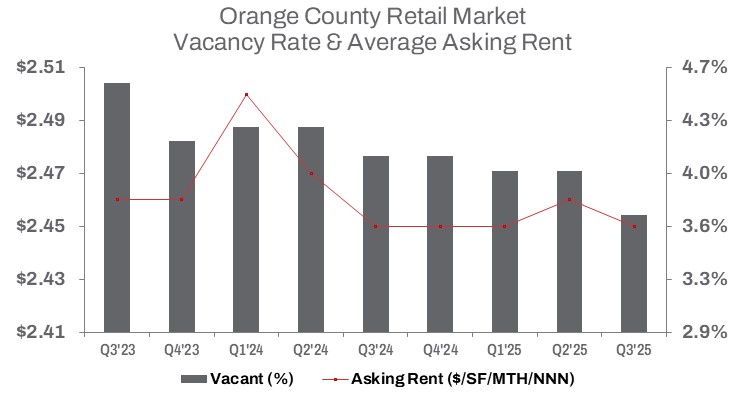

Vacant retail space decreased slightly to 5.29 million square feet, reflecting gradual absorption of available inventory. The countywide vacancy rate inched down to 3.7%, representing a 30-basis-point decline from the previous quarter and a 40-basis-point drop year-over-year, signaling stabilization after several quarters of volatility. Net absorption totaled 389,975 square feet in Q3, marking a sharp turnaround from negative absorption earlier in 2025. Year-to-date absorption climbed to 171,917 square feet, bolstered by significant occupancy gains in the Central submarket, which recorded 445,601 square feet of annual net absorption.

Leasing volume slowed compared to earlier in the year as tenants reassessed expansion plans in light of higher financing costs and inventory pressures. Smaller-format retailers and service-based tenants drove most new leases, while big-box demand continued to lag. Asking rents remained largely stable at approximately $2.45 per square foot per month, consistent with Q2 levels and unchanged from a year ago. Sublease availability declined 6.0% quarter-over-quarter to 254,000 square feet, though it remains modestly elevated compared to pre-pandemic levels.

Sale volume moderated in the third quarter following a strong start to 2025, totaling 982,479 square feet of completed transactions. Despite the slowdown, year-to-date sales volume remains more than double the pace set in 2024. The average sale price rose slightly to $557 per square foot, up 33.2% year-over-year. Cap rates increased 10 basis points quarter-over-quarter but remain down 10 basis points year-over-year at 4.7%, reflecting how sellers and investors are weighing opportunities in light of evolving demand and financing conditions.

Construction activity remained limited, with only 45,692 square feet delivered during the quarter. This aligns with the regional slowdown in new development, reflecting developers’ cautious approach in response to elevated interest rates and tighter lending conditions.

One notable transaction underscored renewed owner-operator interest in large-scale retail assets: Regency Centers acquired a five-property shopping center portfolio totaling 630,000 square feet in South Orange County from Westar and Rancho Mission Viejo Company for $357 million, or $567 per square foot.

TRENDS TO WATCH

Bankruptcies and restructuring continued to reshape the retail landscape in early 2025, as several national chains—including At Home (which filed for Chapter 11 and closed 26 stores nationwide by September), Big Lots, Joann Fabrics, and Party City—announced closures that altered the regional tenant mix.

Despite these national headwinds, optimism returned this quarter, highlighted by the successful leasing of former Rite Aid locations. Rite Aid’s completed nationwide closure program created highly desirable spaces that have quickly been absorbed. Two notable examples include a 21,445-square-foot space at Tustin Ranch Plaza, 13151 Jamboree Road in Tustin, and a 14,061-square-foot freestanding building at 1035 N. Magnolia Avenue in Anaheim. The Anaheim property will be occupied by PremierOne Plus MSO, highlighting the growing trend of medical service organizations—or “medtail”—repurposing well-located retail vacancies.

Beyond the repurposing of pharmacy sites, the market also saw activity in the specialty retail segment. In Costa Mesa, Anaheim Feed & Pet Supply subleased a 13,940-square-foot former grocery store. These transactions underscore ongoing demand for high-traffic, prominent locations within strong demographic trade areas, particularly those benefitting from synergy with nearby retailers and shopping centers.

Despite economic headwinds, Orange County’s retail fundamentals remain comparatively healthy. Limited new supply, resilient consumer spending, and strong demographic continue to support gradual market progress. Looking ahead, success will depend on strategic repositioning, adaptive reuse, and tenant diversification as the region’s retail landscape continues to evolve.