Fourth Quarter 2024

Orange County’s Retail Market Sees Signs of Recovery Despite Bankruptcies and Shifting Demand

Occupancy gains and rising sales prices signal stability, but concessions and market volatility persist.

With competition for prime retail space expected to remain strong, market volatility is likely to increase.

MARKET OVERVIEW

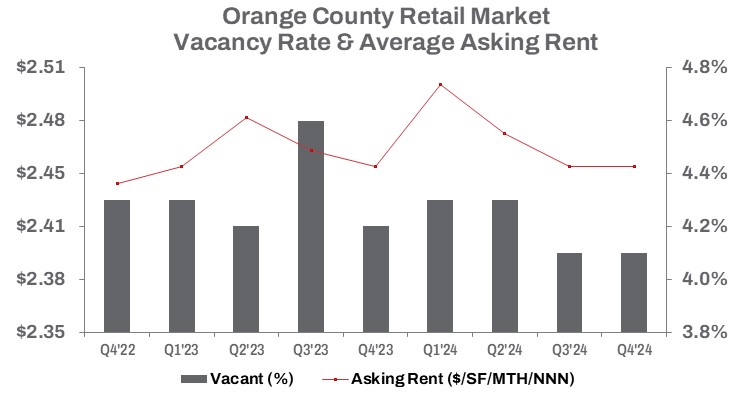

While the economy remains steady, Orange County’s retail market continues to face challenges. Demand for retail space has driven mixed but broadly positive trends, with excess inventory gradually being absorbed.

Retail bankruptcies in 2024 led to the closure of several well-known chains, but some retailers capitalized on the opportunity to secure prime locations. As a result, retail occupancy increased by 62,691 square feet quarter-over-quarter but remained nearly 610,000 square feet below Q4 2023 levels. Total vacant space declined from its Q4 2020 peak, ending 2024 at 5.8 million square feet—an encouraging sign of gradual recovery since the pandemic.

Despite modest occupancy gains, landlords continued offering concessions, while asking rents remained flat year-over-year at $2.45 per square foot triple net. Some investors shifted toward selling, pushing the average retail sale price up 8.5% from the previous quarter to $468 per square foot. This increase was driven by notable transactions, including:

Home Ranch Commons, a 60,737-square-foot neighborhood center in Yorba Linda, which sold for $570 per square foot.

Santa Margarita Marketplace, a 29,342-square-foot community center in Rancho Santa Margarita, which sold for $776 per square foot.

A surge in transactions fueled a 14.8% increase in square footage sold during Q4, surpassing 434,200 square feet. However, total sales volume for 2024 remained 41.2% lower than in 2023, totaling approximately 1.7 million square feet.

On the leasing side, activity jumped 46.0% quarter-over-quarter, with renewals and subleases helping stabilize the vacancy rate. Year-to-date leasing volume for 2024 was 5.9% higher than the previous year.

TRENDS TO WATCH

Landlords and sublessors will likely continue adjusting rents to improve cash flow and fill vacant spaces. South Orange County, which holds 1.5 million square feet of available retail space—the most in the region, saw a 2.8% year-over-year decline in direct asking rents, dropping to $2.75 per square foot triple net. This decline has sparked some demand, with sublessors offering competitive lease terms.

Despite being home to Orange County’s most prestigious retail market, the Airport submarket recorded 8,043 square feet of negative absorption in 2024. While this represents only a marginal change from 2023, it contributed to a 10-basis-point increase in the vacancy rate, which rose to 3.1%. High-priced retail space saw reductions, while sublease inventory declined 39.9% year-over-year. Property owners are expected to continue offering incentives to attract tenants, though filling larger vacated spaces remains challenging. However, expanding retailers are actively pursuing well-located vacancies, particularly those available for sublease or returned to landlords following retail bankruptcies.

The Airport submarket, home to South Coast Plaza and Fashion Island, serves as a bellwether for Orange County retail. The submarket saw a 4.7% quarter-over-quarter drop in average asking rents and a 13.2% year-over-year decline for direct space, closing 2024 at $2.62 per square foot triple net. Limited sublease availability will likely keep the vacancy rate below the regional average.

Retailer bankruptcies, and the evolving economic landscape, will continue to create both challenges and opportunities. Craft and sewing retailer Joann is moving toward liquidation following its second bankruptcy in less than a year. Pending court approval, all remaining locations will begin going-out-of-business sales, underscoring the difficulties brick-and-mortar retailers face in a shifting consumer landscape.

Joann’s closure affects six locations in Orange County, totaling 146,117 square feet. With competition for prime retail space expected to remain strong, market volatility is likely to increase. Landlords, tenants, and investors will aggressively compete for well-positioned properties as the sector continues its recovery.