Orange County Commercial Real Estate Average Sale Size Drops in Q3 2024

Smaller-Dollar Deals Dominate Orange County CRE Sales

Industrial sector remains resilient as office, retail, and multifamily shift to smaller deals amid interest rate uncertainty

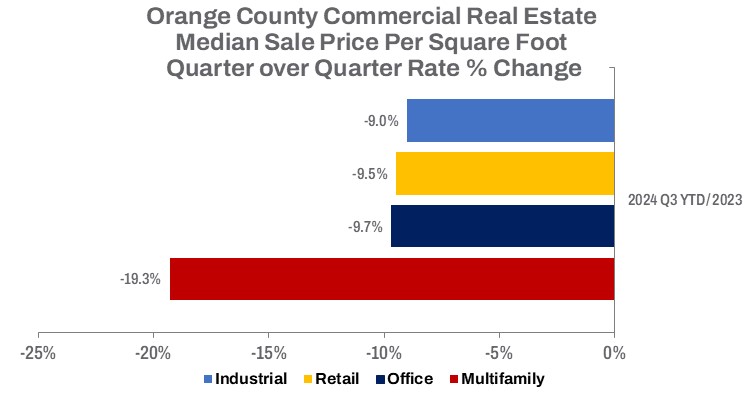

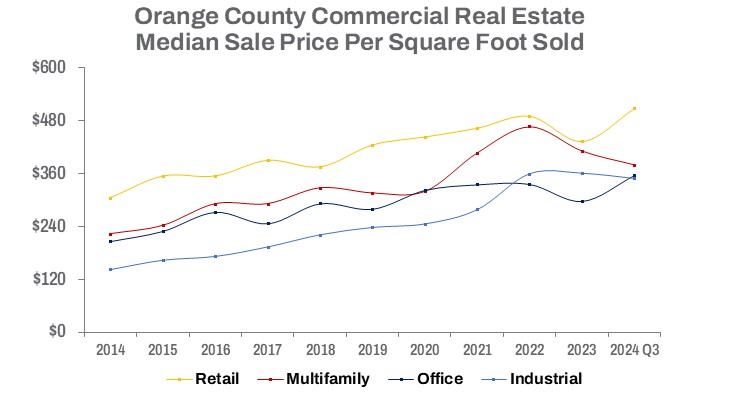

Median sales prices are down year-over-year

Images highlighting top retail, multifamily, office, and industrial sales in Orange County, Q3 2024

Images highlighting top retail, multifamily, office, and industrial sales in Orange County, Q3 2024

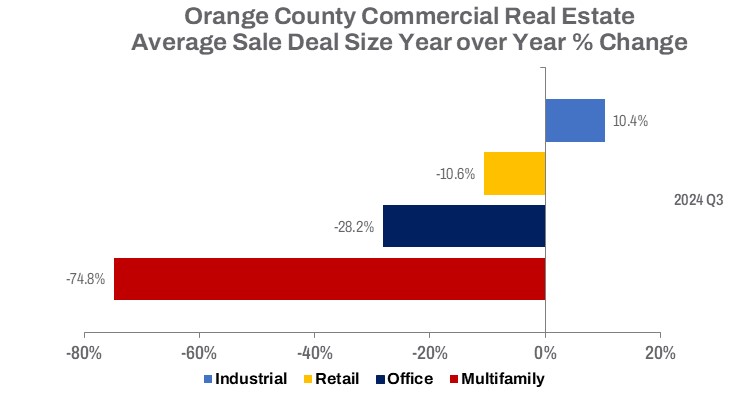

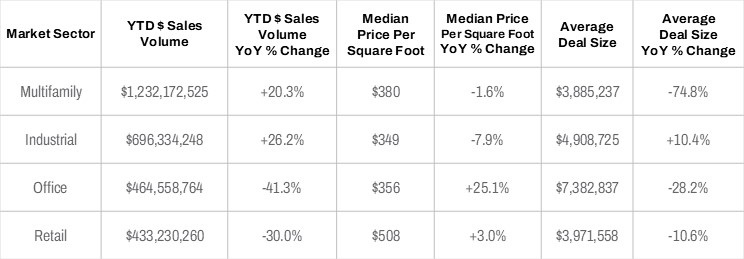

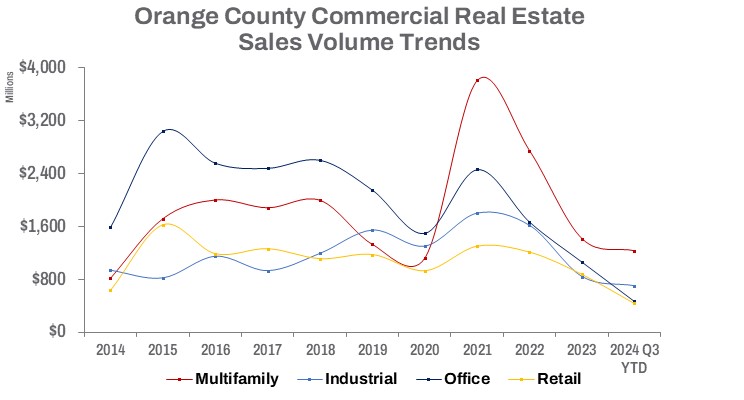

In Q3 2024, combined sales of office, industrial, retail, and multifamily properties in Orange County’s commercial real estate market saw a notable year-to-date decline of 7.9%, totaling $2.8 billion. The average deal size dropped 41.7%, driven by smaller transaction sizes, rising borrowing costs, and heightened economic uncertainty. A widening spread between asking and selling prices highlights ongoing market recalibration, although industrial properties bucked this trend, the only sector showing growth in deal size. Meanwhile, large multifamily transactions saw a steep drop.

Elevated borrowing costs have continued to weigh on commercial real estate sales. In September, after last year’s series of rate hikes, the Federal Reserve reduced the federal funds rate by 50 basis points, followed by another 25-basis point cut in November, as inflation approaches the Fed’s 2% target. Meanwhile, the national unemployment rate has increased from 3.7% to 4.1% this year, suggesting potential softness in the job market and supporting the case for additional rate cuts—albeit at a gradual pace to avoid reigniting inflation.

Industrial building sales, though resilient, declined by 44.9% quarter-over-quarter, impacted by falling lease rates, higher borrowing costs, and a slowing economic outlook, which has led owner-users, small businesses, and investors to reconsider buying or selling. Despite recent pullbacks, year-to-date sales volume marked a 26.2% increase over last year, approaching $700 million. The median sale price per square foot for industrial buildings dropped by 9.0% quarter-over-quarter and fell by 7.9% year-over-year. While the average deal size declined 55.9% quarter-over-quarter, it showed a 10.4% year-over-year increase, averaging $4.9 million in the third quarter.

Orange County Commercial Real Estate Market Statistics – Q3 2024

Orange County’s industrial market growth also faces potential obstacles from AB 98, signed into law by Governor Newsom on September 29. Effective January 1, 2025, the law introduces regulations that may limit warehouse development, impacting local employment and growth—and increasing the value of existing infill properties. In one of the largest industrial sales this quarter, Bain Capital, a leading private investment firm, partnered with L.A.-based Staley Point Capital to acquire a fully leased, 161,738-square-foot manufacturing building in North Orange County for $30.1 million. Built in 1959 and once owned by Hughes Aircraft Company, the property last sold in 1997 for $2.5 million, reflecting significant appreciation.

Interest rates and regulation are significant factors influencing investment decisions, with borrowing costs remaining crucial as the Fed focuses on controlling inflation. Commercial real estate sales have slowed from their breakneck pace as interest rates adjust.

In Q3, the Orange County multifamily market registered only one sale of a building with over 100 units: The Arbors, a 160-unit apartment complex at 1100-1200 E Fairhaven Ave in Santa Ana, North Orange County, which sold for $40.75 million in August. This transaction highlights significant appreciation for the seller, who originally purchased the property in 2013 for $28 million. However, deals of this size have been on the decline, with four sales recorded in Q1, three in Q2, and four at the same time last year.

Despite increased borrowing costs adding financial risk, the multifamily sector continues to experience demand in certain asset classes, though growth prospects appear less optimistic. In Q3, multifamily sales volume reached $1.23 billion, reflecting a 20.3% increase year-to-date compared to last year. However, this marks a 49.9% decline from the previous quarter, signaling that strong investor demand earlier this year has cooled. Lower sales volumes have put downward pressure on prices, with the median sale price per square foot for multifamily buildings declining by 19.3% quarter-over-quarter and 1.6% year-over-year. Investors, responding to rising borrowing costs, price adjustments, and regulatory challenges like rent control, led to a 64.5% quarter-over-quarter and 74.8% year-over-year drop in the average deal size, now at $3,885,237.

With Proposition 33 officially rejected by California voters, multifamily investors in Orange County and across California may breathe a sigh of relief. The measure, which aimed to repeal the Costa-Hawkins Rental Housing Act and expand rent control, had the potential to significantly reshape the multifamily market. Proponents argued it would strengthen tenant protections, while critics warned it might worsen the housing shortage by discouraging new development, ultimately impacting affordability. With Proposition 33 defeated, existing rent control limitations under Costa-Hawkins will remain in place, preserving the current regulatory landscape.

Meanwhile, retail bankruptcies have risen due to increased labor and supply chain costs, with California’s minimum wage hike to $20 per hour posing a particular challenge for fast-food establishments. Since the wage increase in April, these franchises have adjusted by reducing worker hours, impacting investment in net-leased properties. Despite ongoing recovery for retailers, year-to-date sales volume of retail real estate remains 63.7% below 2020’s low.

Retail building sales, as brick-and-mortar stores continue their recovery, recorded close to $433 million in year-to-date sales volume—still 53.4% below 2020’s pandemic low. The retail sector has a long way to go to reach “normal” levels, with mixed outlooks across product types. While the median sale price per square foot deceased by 9.5% quarter-over-quarter it rose by 3.0% year-over-year, retail is reflecting low-volume sales performance, making it the lowest-performing asset class in Orange County with sales volume year to date down 30% from Q3 2023.

Still, well-capitalized retailers are finding opportunities under the current market conditions. In August, Costco Wholesale Corporation acquired a building adjacent to its Costco location in Garden Grove for $12 million, or $401 per square foot. The 29,935 square foot retail building is occupied by Office Depot. The seller, Harvest Capital, Inc., bought the asset in 2017 for $9,180,000, or $307 per square foot. Office Depot, which merged with OfficeMax in 2013, has been closing stores over the past decade.

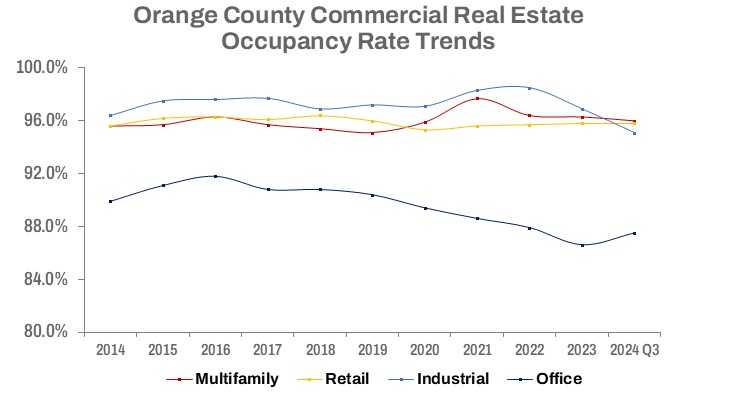

The office market in Orange County continues to face a slow recovery, with landlords offering substantial concessions—such as rent reductions and tenant improvement allowances—to attract tenants, which is further eroding market values and pushing some investors to become sellers as values slip. While a surge in office deals pushed sales volume up by 58.6% from the previous quarter, year-to-date office building sales still fell by 41.3% compared to Q3 2023, totaling $464.6 million. The median sale price per square foot also declined by 9.7% quarter-over-quarter.

Brian Childs, Executive Managing Director of NAI Capital Commercial’s Orange County office, observed, “Office lease rates have remained fairly static over the last year even though office vacancy has been inching up. There is very little appetite for office investors to purchase office properties outside of distress buyers. This has created a situation where owner-users and government entities with deep pockets can purchase office properties at reduced prices.”

Reflecting current market conditions, the quarter’s top office sale was the 157,455-square-foot Jamboree Business Center in Irvine, purchased by the Chinese company TP-Link for $40.6 million, or $258 per square foot, in an owner-user transaction.

Brian further highlighted that while the number of owner-user sales has decreased, the size of properties being acquired by these buyers has grown. “Examples include Microvention’s purchase of 45 Enterprise in Aliso Viejo, a 243,000-square-foot Class A high-rise built in 2008, for $44 million or $182 per square foot and New American Funding’s acquisition of the 208,000-square-foot Class A high-rise at 1 MacArthur Place in Santa Ana for $31 million $149 per square foot. Larger businesses appreciate the control over their office environments, making building location, size, and amenities critical factors driving these sales.”

While the labor market has shown resilience, with Orange County’s unemployment rate dropping to 4.1% in September 2024 from 4.5% in August, recent U.S. Labor Department data indicates slower-than-expected job growth, with only 12,000 jobs added in October. Nationally, unemployment remains at a three-month low of 4.1%, accompanied by accelerated wage growth. The economy expanded at a solid 2.8% annual rate last quarter, driven largely by consumer spending—a key driver of economic growth. Although hiring has slowed, employers are retaining workers, which supports wage gains and consumer spending.

Following the Federal Reserve’s 25 basis point rate cut in November, the likelihood of another cut in December remains possible but uncertain, with economic signals suggesting stronger growth, higher inflation, and a more cautious pace for future rate reductions. While a ‘wait-and-see’ approach from the Fed seems likely, downward pressure on deal sizes continues to challenge the commercial real estate market. As Orange County’s commercial real estate sector adapts to these shifting dynamics, investors remain focused on regulatory developments and economic fundamentals that will shape the market as 2024 concludes and 2025 comes into view.