Orange County Industrial Market Sees Declining Rent with Rising Vacancy

Lower Leasing Velocity and a Significant Increase in Sublease Space Shaping Market Dynamics

MARKET OVERVIEW

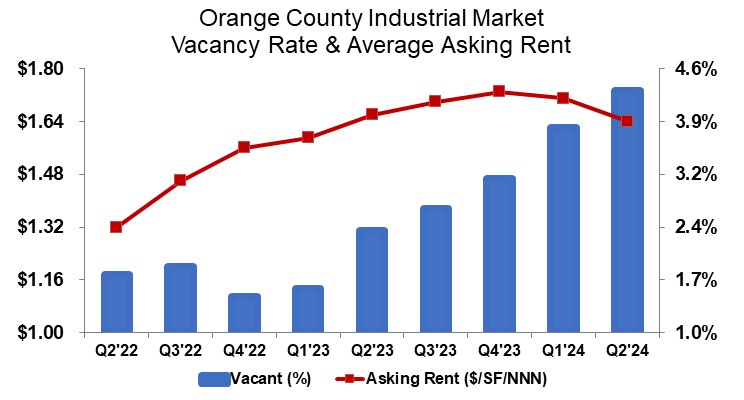

In Q2 2024, the rise in vacancy of industrial space in Orange County continued, contributing to a 190-bps increase in the vacancy rate year over year, now standing at 4.3%—50 basis points higher than Q1 2024. Over the past two years, Orange County has added approximately 6.4 million square feet of completed construction to the market, while absorption has resulted in a negative 1 million square feet during the same timeframe, indicating a shift in the industrial market’s trajectory.

Space under construction, while down by 59.5% compared to last year, rose by 39.0% from the prior quarter. Moreover, completed construction as of the first half of 2024 inched up 2.2% compared to 2023 and increased by 11.1% quarter over quarter, adding 1.2 million square feet in 2024. Developers, racing to meet the demand for warehouse space spurred by e-commerce, have significantly increased capacity. However, the once robust rent growth, which was the primary driver for new construction, has slowed, with the average asking rent in Q2 dropping by 4.1% from the previous quarter to $1.64/SF triple net, softening by 1.2% from Q2 2023.

Orange County Industrial Market Q2 2024 Statistics:

Opportunities, driven in part by pent-up demand, drove year-to-date sales volume on a square foot basis up by 26.6% from last year, with the average price per square foot rising by 13.8% from this time last year. On the leasing side, slowing demand has impacted leasing volume, which is down by 10.1% quarter over quarter and 24.6% year over year, with 4.1 million square feet year to date—the weakest first half of the year since 2007 heading into the Great Recession.

TRENDS TO WATCH

Tenants are gaining leverage to negotiate favorable deals, causing concern for landlords due to lower leasing velocity. The market will be driven by the increase in options for e-commerce warehousing as companies seek flexible solutions to meet evolving demand. Companies actively reducing excess warehouse space have led to a significant increase in available sublease space, up by 50.5% quarter-over-quarter and 39.2% higher than Q2 2023, totaling approximately 3.3 million square feet—just shy of the all-time high in 2009. This abundance of industrial space indicates that companies with warehousing requirements will have a variety of options as cargo throughput at the ports remains strong. According to the latest figures from the Ports of Los Angeles and Long Beach, combined inbound TEU cargo volumes—a significant driver of warehouse space demand in SoCal—increased by 17% year-to-date as of May 2024.

While the growth rate is expected to be lower, elevated prices and interest rates will affect industrial building sales, though quality space will still command a premium. Sales dollar volume shot up 46.2% from the previous quarter, with opportunity driving the market. Reflecting this trend, Rexford Industrial Realty Inc., a Los Angeles-based REIT and one of the most active buyers of industrial real estate in OC over the past few years, paid $94.3 million for a 278,572-square-foot distribution facility in Fullerton. The average sale price per square foot at $338 was 9.4% below the average for this quarter. Despite this, the average price per square foot rose 23.2% quarter over quarter and registered a 13.8% year-over-year increase to $373 per square foot. The combination of elevated interest rates and slowing demand will continue to have a settling effect on pricing heading into the second half of the year.