Orange County Q1 2021 CRE Market Outlook

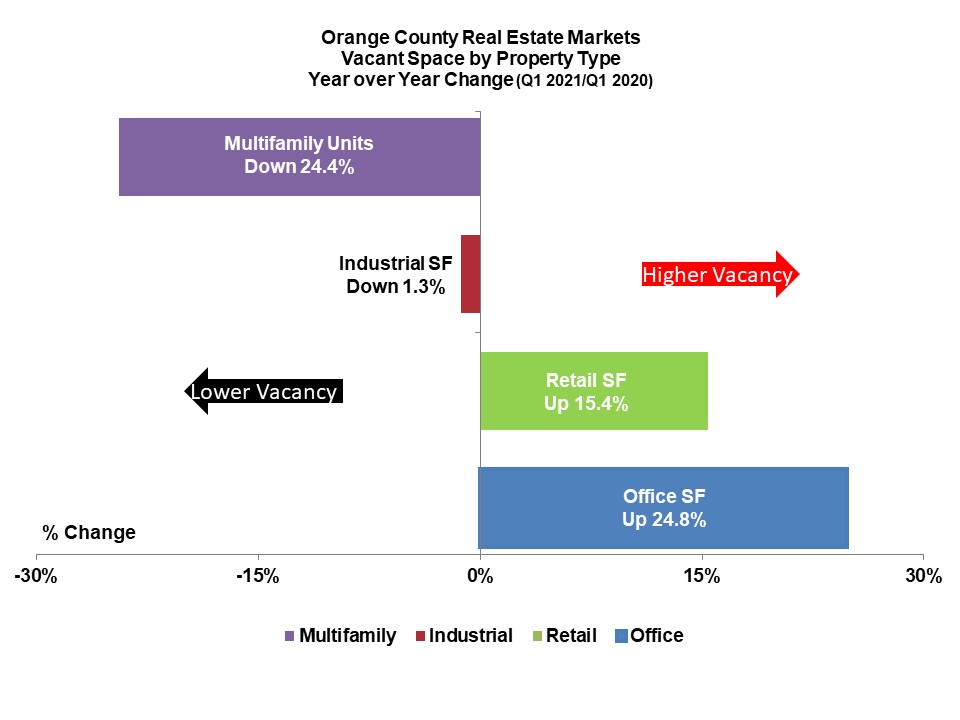

A year into the pandemic, commercial real estate markets in Orange County had an uneven performance. Vacancy declined in multifamily and industrial markets over the past year, while office and retail striving to reopen from the Covid-19 shutdown suffered from growing vacancy in Q1 2021.

Vacant multifamily units decreased 24.4% from Q1 2020 to Q1 2021, dropping the vacancy rate to a level not seen since Q1 2007. A lack of affordability for single-family homes and a tight supply of housing continued to drive demand in the multifamily rental market. The median price of a house sold in Orange County reached an all-time high of $820,000 in February 2021.

Industrial vacant space decreased 1.3% in Q1 2021, dropping back to pre-pandemic levels. While the acceleration of online shopping and ecommerce growth during the pandemic boosted demand for warehouse and distribution space in the region, Orange County’s industrial market responded with an insignificant 664,000 square feet of new inventory added to the industrial base since Q1 2020.

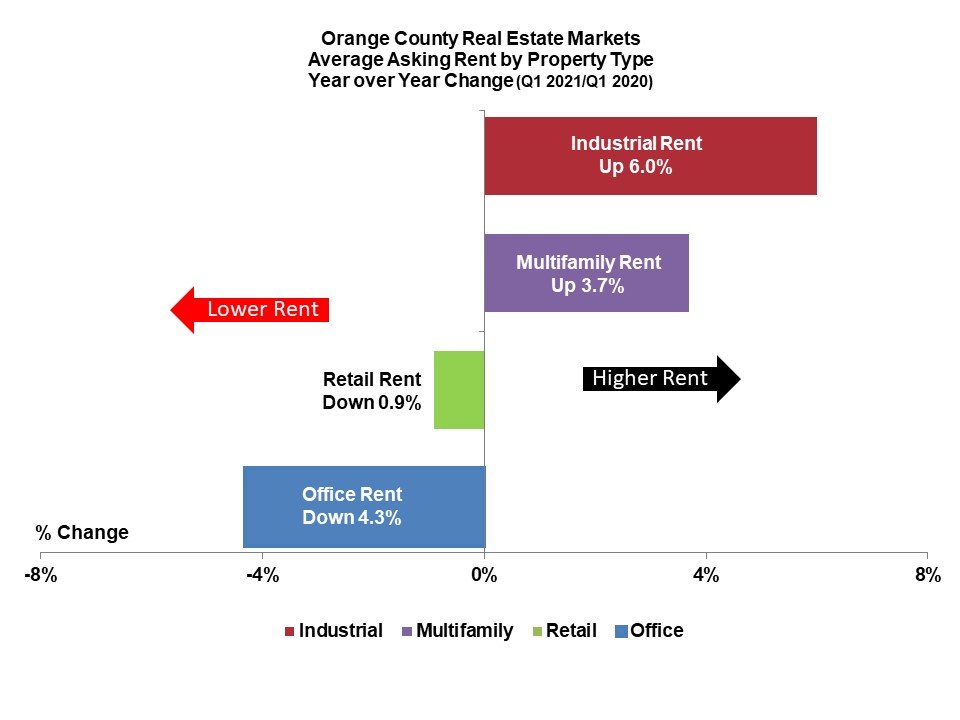

The average asking rent for office space in Orange County responded the quickest to the adverse effects of the pandemic shutdown, falling 4.3% from the prior year. Motivated landlords, as demand plummeted, decreased rents to compete for tenants and maintain occupancy.

Retail landlords resisted a wholesale drop in rent despite the growing vacancy caused by the pandemic shutdown. The vacancy rate registered 4.4% in Q1 2021. Landlords, hopeful they have seen the worst in this downturn, on average dropped the asking retail rent 0.9% in Q1 2021 from Q1 2020. During the Great Recession the vacancy rate hit a high of 6.7% in Q3 2010 and the average asking rent then declined 11% from Q3 2009.

Orange County’s constrained industrial market conditions produced the highest rent growth in the region, up 6.0% from Q1 2020.

Multifamily saw a 3.7% rent growth streak, driven by a shortage of affordable housing. The market absorbed 6,625 units between Q1 2021 and Q1 2020, compared to a lower 4,466 units of newly completed units added to the market over the same time.

Strong demand, constrained supply, rising rent, and declining vacancy characterized the industrial and multifamily markets. Uncertain demand and rent cuts, in contrast, typified office and retail markets.