Orange County’s Industrial Market Sees Leasing and Sales Velocity Fluctuate

Opportunities Abound as the Market Continues to Evolve for Tenants and Investors

MARKET OVERVIEW

Orange County’s industrial market is experiencing a notable shift away from the previously high demand for warehouse space, resulting in an increasing amount of vacant excess space entering the market. Sublease space has witnessed a significant 107% increase compared to the previous quarter and an even more substantial 227% increase compared to a year ago. As of the first quarter of 2024, the total vacant sublease space amounts to 1.2 million square feet, marking a 37% increase compared to the level observed during the Great Recession in Q1 2008.

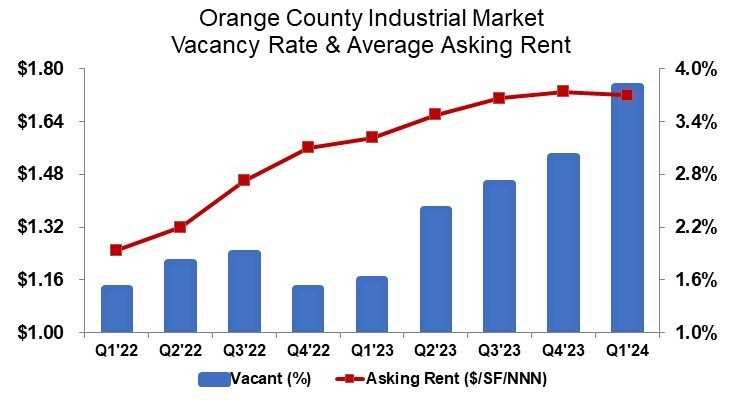

Leasing volume has declined by 28.3% compared to the previous quarter, totaling approximately 2.2 million square feet. Over the past five quarters, the industrial market has seen the addition of 5.1 million square feet of vacant space, accompanied by 3.2 million square feet of completed construction. As demand shifted, the vacancy rate has risen by 220 basis points from a year ago, reaching 3.8%, reflecting the increased supply.

Rising rents, the primary driving force behind new construction, have moderated slightly this quarter. The average asking rent dipped from its all-time high to $1.72 per square foot triple-net, marking a 1-cent decrease from the previous quarter but remaining 8.2% higher than Q1 2023. Since the depths of the pandemic shutdown in Q2 2020, the average rent has climbed by 68.6%. However, development has begun to change as industrial space under construction shows a 27.8% decrease compared to the previous quarter, experiencing a year-over-year decline of 61.1%. The sales volume declined by 51.6% compared to the previous quarter, starting the year with less than half a million square feet sold.

Orange County Industrial Market Q1 2024 Statistics:

TRENDS TO WATCH

The industrial real estate market in Orange County is undergoing notable shifts, affecting both landlords and tenants. Slower leasing velocity presents challenges for landlords and sublessors with vacant space, while tenants are gaining leverage in negotiating favorable deals. Particularly noteworthy is the increasing trend of companies offering excess warehouse capacity for sublease, resulting in a significant rise in available sublease space. This surplus provides companies seeking warehousing solutions with a diverse array of options, reflecting a market witnessing a surge in warehousing capacity as e-commerce companies adapt to evolving demand.

Meanwhile, industrial building sales are impacted by elevated prices and interest rates, projecting a lower growth rate. Quality space continues to hold a premium status, with the average price per square foot rising by 3.2% quarter over quarter and 2.7% year over year, underscoring market strength. Despite these challenges, there remains a fundamental desire for ownership among users and investors in Orange County. Market pricing is anticipated to stabilize in the latter half of the year as opportunities are pursued.

The region’s industrial market remains robust, evidenced by sustained demand for large distribution warehouses reflected in the new development pipeline. The majority of buildings under construction exceed 50,000 square feet, with an average size closer to 100,000 square feet, predominantly available for lease rather than sale. However, due to the abundance of options, preleasing is expected to slow. As of the end of the first quarter, approximately 81% of warehouse space under construction remained unleased. Additionally, none of the buildings available for sale prior to completion have been sold, indicating a transition towards balanced market conditions from the previous frenzy.