Year-End Review – Market Outlook 2025

SoCal Commercial Real Estate Market Outlook 2025: Key Charts and Insights

Vacancy and rent trends indicate that the commercial real estate markets are stabilizing, with vacancies peaking and rents nearing their trough.

As Southern California’s commercial real estate markets approach year-end 2024, trends across the industrial, multifamily, retail, and office sectors are beginning to stabilize.

As Southern California’s commercial real estate markets approach year-end 2024, trends across the industrial, multifamily, retail, and office sectors are beginning to stabilize. Looking ahead to 2025, these markets are expected to continue evolving, with regional variations shaping trends and creating new opportunities within each sector. Chris Jackson, CEO of NAI Capital Commercial, foresees that most markets in Southern California “will see more growth,” except the City of Los Angeles, due to Measure ULA.

Industrial Market

Southern California’s industrial market, once characterized as tight just three years ago, has loosened significantly by year-end 2024. Vacancy rates have steadily risen due to a combination of new construction and natural attrition. The double-digit rent growth seen in previous years has slowed, reflecting the abundance of industrial space now available. Chris expects the overall commercial real estate market to evolve in 2025, with an uptick in investment and owner/user sales due to lower interest rates. “We expect vacancy to stabilize and activity to increase in the first quarter,” he says.

Challenges and Outlook

When discussing potential challenges, Chris notes the uncertainty surrounding trade restrictions, though he finds it difficult to predict their exact effect: “We see the possibility of trade restrictions causing some issues, but it’s difficult to tell at this point.” On interest rates, he adds, “With rates coming down, people now know what to expect, so that’s behind us,” which is expected to strengthen market activity in 2025.

Chris anticipates strong overall market activity, with the industrial and retail sectors leading the way in growth. “The industrial market in 2025 is expected to experience significant growth and transformation driven by supply chain trends, increased construction activities, and evolving demand dynamics,” he predicts. Chris believes companies that invest in technologies and adapt to changing consumer behaviors will be well-positioned to thrive. This includes diversifying suppliers, increasing local sourcing, and adopting advanced technologies like AI and blockchain to improve transparency and efficiency.

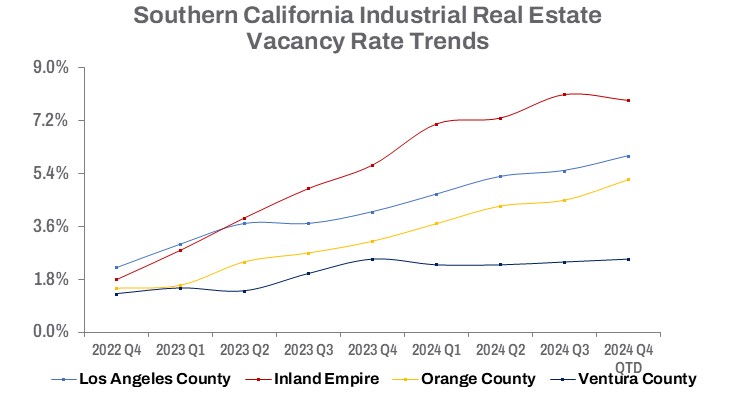

Industrial Real Estate Vacancy

- Los Angeles County: The industrial market, spanning over 902.1 million square feet, recorded a 6.0% vacancy rate, equating to 54.5 million square feet of vacant space. This reflects a 10.3% increase in vacant space quarter-over-quarter (QoQ) and a 48.5% rise year-over-year (YoY).

- Inland Empire: The industrial market, totaling 742.9 million square feet, recorded a 7.9% vacancy rate, reflecting 58.4 million square feet of vacant space. This marks a 0.8% improvement in vacant square feet quarter-over-quarter (QoQ) but a 45.3% increase year-over-year (YoY).

- Orange County: Out of 222.6 million square feet of industrial space, the vacancy rate was 5.2%, equating to 11.5 million square feet of vacant space. This represents an 14.6% QoQ increase, and a 68.0% YoY rise in vacancy.

- Ventura County: The smallest market, with 50.5 million square feet of industrial space, had the lowest vacancy rate at 2.5%, corresponding to 1.3 million square feet of vacant space. This is a 4.3% increase QoQ and a 0.1% year-over-year change.

The Inland Empire, a key logistics hub of both regional and national significance, has faced notable challenges in the industrial market, driven by economic factors and supply chain disruptions. According to John Boyer, Executive Managing Director of NAI Capital Commercial’s Inland Empire office, 2025 will bring its own set of challenges and opportunities. In this brief Q&A, he shares his insights on the following questions:

Q1: How do you expect the industrial market in the Inland Empire to perform in 2025, considering supply chain trends, construction, and demand?

“For the obvious recessionary reasons, 2024 saw industrial rates drastically down between 40% to 60% from the ‘high water mark’ years of 2020 to 2022.” John notes. Adding to the challenge was an influx of unstoppable construction projects, which contributed to vacancy rates approaching double digits. “Without getting into the political conversation, and a new administration taking control, I suspect that 2025 will show signs of recovery but not at the same pitch and velocity of the high-water mark years. Generally speaking, through my experience of weathering five recessions and or administration changes, it will take about two years for the incumbent administration to implement their policies to notice any significant changes. The unknown at this point is how the current administration’s proclamation of imposing tariffs to China, Canada and Mexico will affect the Inland Empire’s logistical base.

Q2: How do you anticipate interest rate fluctuations will affect property values, leasing/sales activity, and investor sentiment in 2025?

The primary reason for the drastic change in the industrial market was the Fed’s raising the interest rates. Until such time that interest rates stabilize and are reduced by 2 to 3 basis points, I foresee the values across the board continue to decline.

Q3: What are the most significant challenges and opportunities you expect the Inland Empire industrial market to face in 2025?

We must compress the vacancy factor to healthy levels. We all know that a healthy vacancy factor is about 6% and with vacancy exceeding double digits, rates will continue a downward trajectory until we get to healthy levels. At the top of the market years, vacancy rates were sub-2%, and in some sub-markets sub-1%, this was the driver of record rates for leasing, sales and land sales, and this was the result of the over-inflated industrial market in the Inland Empire.

Southern California’s industrial sector, particularly in the Inland Empire, stands at a critical juncture. As economic and policy shifts unfold in 2025, stakeholders will need to navigate challenges while identifying opportunities to adapt to a rapidly changing landscape.

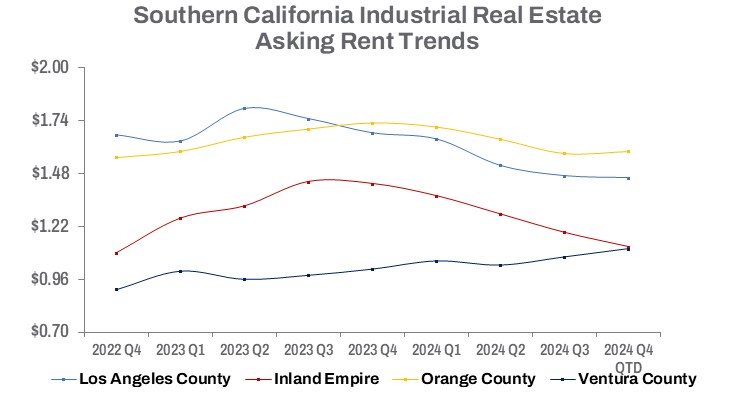

Industrial Real Estate Rents

- Los Angeles County: Average asking rents declined to $1.46 per square foot (NNN), down 0.7% QoQ and 13.1% YoY.

- Inland Empire: Average asking rents dropped to $1.12 per square foot (NNN), reflecting a 5.9% QoQ decline and an 21.7% YoY decrease.

- Orange County: Average asking rents edged up 1 cent QoQ at $1.59 per square foot (NNN) but saw an 8.1% YoY decline.

- Ventura County: The only market with rent growth, average asking rents rose to $1.11 per square foot (NNN), a 3.7% QoQ increase and a 9.9% YoY increase.

Southern California’s multifamily market, once characterized by exceptionally low vacancies just three years ago, has evolved significantly by year-end 2024. Vacancy rates have fluctuated across the region, shaped by changing economic conditions and shifts in rental demand. While rent growth remains positive in many areas, it has moderated compared to the robust increases seen in previous years.

Executive Vice Presidents Kevin Kawaoka, CCIM, and Tim Steuernol of NAI Capital Commercial’s Multifamily Services Group are optimistic about the multifamily sector’s prospects for 2025.

Tim explains, “There is renewed optimism in the multifamily market and an expected increase in transaction volume for 2025. Demand for rental housing in Southern California will remain constant due to the lack of supply for affordable places to live and the high cost of single-family housing. With interest rates still elevated, the market will need to evolve to a state of acceptance. Sellers must understand the market has shifted—values are not what they were two years ago—while investors will be eager to place capital in a more stabilized market.”

Kevin adds, “With the outcomes of Prop 33 and Prop 34, alongside interest rates continuing to decline, the fundamentals are strong for the Los Angeles multifamily investment sector.”

Despite these positive indicators, challenges remain. Limited supply and the widening affordability gap between renting and owning continue to define the market. Kevin notes, “The gap continues to be the backbone for strong rent levels,” citing the California Association of Realtors’ forecast of a 4.6% increase in the median home price statewide to $909,400 in 2025. “This affordability gap further positions multifamily rentals as a practical choice for many residents, fueling sustained demand.”

Developers also face hurdles. “The biggest challenge will be growing the supply of affordable multifamily housing,” Kevin explains. “Planning departments struggle to streamline development processes. The more supply we build, the better off everyone will be, as we are far from keeping pace with the demand pipeline.”

Tim highlights additional concerns, including the debt markets and public policy issues affecting cities like Los Angeles. “Investors have been bogged down in recent years by increased operational costs, rising interest rates, and overbearing policy issues that limit NOI growth and stifle investment. Opportunities will arise as owners of multifamily assets decide to sell, understanding today’s values, while buyers anticipate future appreciation as interest rates decline and rent growth accelerates.”

Opportunities are emerging despite these challenges. Kevin points to promising trends: “As prices in certain areas have come down, developers are locking down sites for future multifamily projects. Some apartment investors are finding discounts on buildings at 20% or more, purchasing at well below replacement cost.” Additionally, companies calling employees back to the office have sparked investor interest in central business districts, betting on a resurgence in these areas.

Looking ahead, Kevin expects declining interest rates to stimulate multifamily investment. “Predictions of a decline in interest rates are likely to spark renewed interest in multifamily investments. Reduced borrowing costs will create opportunities for developers and investors to pursue new projects and acquisitions, potentially boosting transaction activity beyond 2024 levels.” With Propositions 33 and 34 no longer immediate concerns, Kevin foresees property values rising as cap rates compress, signaling steady growth for Los Angeles’ multifamily sector in 2025.

Tim concludes, “Interest rates are a major driver of property values,” shaping sales activity and investor sentiment. As the market adjusts, sales activity is expected to become more robust as investors eagerly look to re-enter the market and deploy capital.”

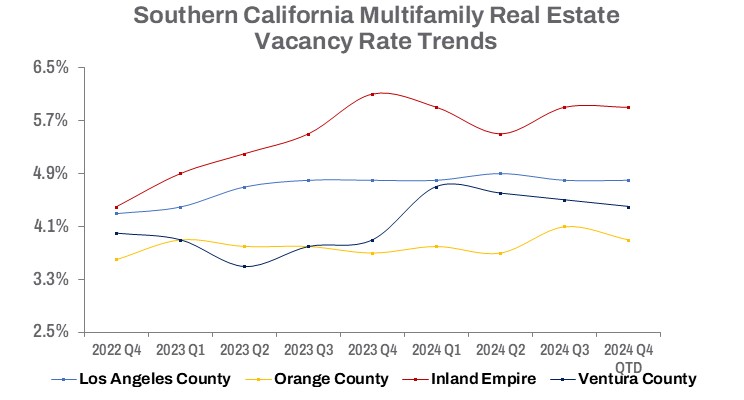

Multifamily Real Estate Vacancy

- Los Angeles County: With 1,227,369 existing rentable units, the multifamily market recorded a 4.8% vacancy rate, reflecting a 0.4% quarter-over-quarter (QoQ) decrease and a 0.6% year-over-year (YoY) increase in vacant units.

- Orange County: Out of 311,602 rentable units, the vacancy rate was 3.9%, a 4.1% QoQ drop but an 6.7% YoY increase in vacant units.

- Inland Empire: The market, with 234,134 rentable units, posted a 6.1% vacancy rate, marking a 1.8% QoQ increase but a 1.1% YoY decline in vacant units.

- Ventura County: The smallest market, with 50,673 rentable units, had a 4.3% vacancy rate, down 1.6% QoQ but up 16.9% YoY in vacant units.

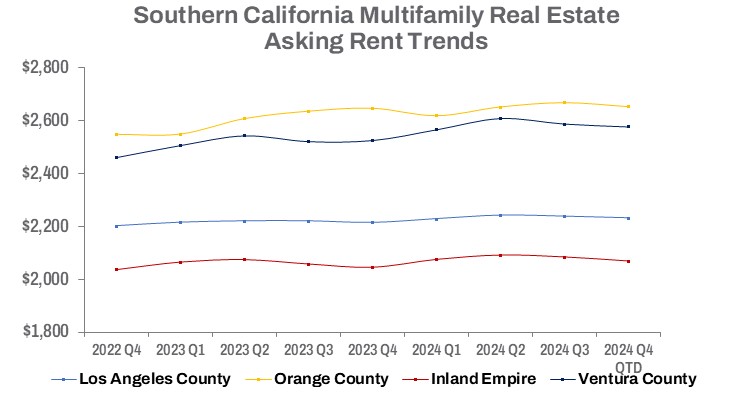

Multifamily Real Estate Rents

- Los Angeles County: Average asking rents reached $2,232 per unit, reflecting a 0.3% QoQ decrease but a 0.8% YoY increase.

- Orange County: Average asking rents were $2,654 per unit, down 0.6% QoQ but up 0.2% YoY.

- Inland Empire: Asking rents averaged $2,070 per unit, a 0.7% QoQ drop but a 1.1% YoY increase.

- Ventura County: Average asking rents rose to $2,578 per unit, showing a 0.4% QoQ decline but a 2.1% YoY increase.

Southern California’s retail market has undergone significant changes since the pandemic shutdown four years ago, reaching a ‘new normal’ by year-end 2024. Vacancy rates have fluctuated across the region, influenced by shifting consumer behaviors, economic conditions, and evolving demand for retail spaces. While rent growth remains positive, it has slowed due to inflation and challenges like retailer bankruptcies and rising vacancies.

In this Q&A, Executive Vice President Sheri Messerlian of NAI Capital Commercial Services Group shares her perspective on the retail market’s performance, the impact of interest rates, and the challenges and opportunities ahead in 2025.

Q1: With retail spaces continuing to adapt to changing consumer habits, how do you foresee the retail market performing in 2025?

The retail real estate landscape of 2024 reflected a dynamic interplay between consumer values, limited supply, and shifting demand. I expect these same trends to continue in 2025, with smaller and smarter demand for retail space. There is a trend of major big-box retailers, such as Target and Walmart, opening smaller concept stores, where they feel the move toward smaller stores is a key part of retail’s evolution.

The main takeaway is that retail property owners and operators are becoming more open to flexibility and willing to adapt to tenants’ needs.

One major trend that contributed to retail real estate in 2024 was the lack of new retail construction due to high costs and restrictive governmental regulations. I expect retail developers and investors to be open to redesigning and redeveloping existing spaces to attract more tenants and shoppers. This will be especially true in prime trade areas, which are experiencing record-high occupancy levels and asking rents due to strong demand.

Another trend I foresee is that neighborhood shopping centers in densely populated urban and suburban areas will continue to perform well. Despite the growth of e-commerce, brick-and-mortar stores still have plenty of room to succeed, as e-commerce accounts for only about 15% of all retail sales. As a result, this asset class is expected to experience steady performance, with unchanging vacancy rates and moderately positive rent growth for neighborhood and community shopping centers.

Q2: How do you anticipate interest rate fluctuations will affect property values, sales activity, and investor sentiment in 2025?

Interest rates play a pivotal role in the real estate market, influencing buyer behavior, pricing, and overall supply and demand dynamics. In 2024, most sales in commercial real estate were financed either by all-cash buyers or SBA loans for owner-users, as investors were highly interest-rate-sensitive, which suppressed real estate prices to some degree.

However, with expectations of lower interest rates for 2025, I foresee more investors entering the market, increased construction supply, and a rise in mixed-use developments that would provide more affordable housing and new retail spaces.

Q3: What are the most significant challenges and opportunities you expect the retail market to face in 2025?

The fundamentals of the retail real estate market are positive net absorption, rising rents, and lower vacancies, which are largely driven by the lack of new supply. Retail space deliveries have reached record lows over the past four years. The opportunities for 2025 mainly lie in meeting the demand for affordable housing and retail space through mixed-use construction. With anticipated lower interest rates and the impact of California’s SB 9 and 10, there will be increased opportunities for higher-density mixed-use projects, which will greatly affect retail real estate supply to meet growing demand.

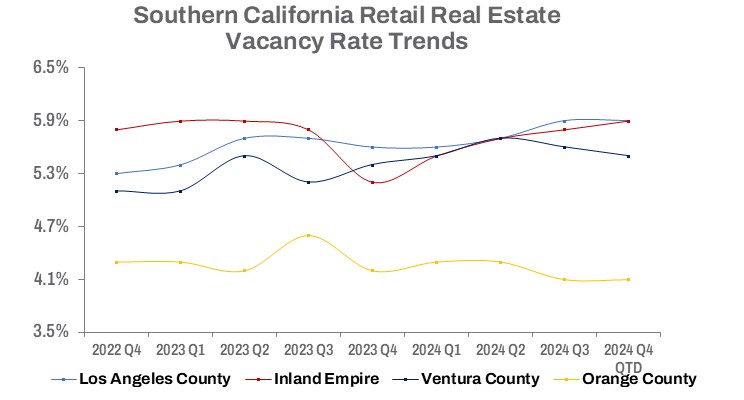

Retail Real Estate Vacancy

- Los Angeles County: The retail market, with 317,607,916 square feet of total rentable building area (RBA), recorded a 5.9% vacancy rate, reflecting a 0.4% quarter-over-quarter (QoQ) decrease and a 5.4% year-over-year (YoY) increase in vacant space.

- Inland Empire: With 152,595,711 square feet of total RBA, the vacancy rate was 5.9%, showing a 2.7% QoQ increase and a 13.4% YoY rise in vacant space.

- Orange County: Out of 142,028,997 square feet of total RBA, the vacancy rate held steady at 4.1% QoQ, reflecting a 1.6% YoY decrease in vacant space.

- Ventura County: The retail market, with 43,928,653 square feet of total RBA, posted a 5.5% vacancy rate, down 1.1% QoQ and up 3.0% YoY in vacant space.

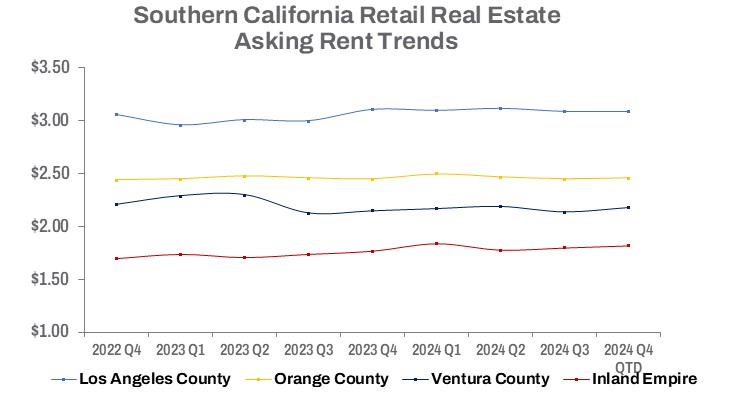

Retail Real Estate Rents

- Los Angeles County: Average asking rents were $3.09 per square foot (NNN), remaining flat QoQ but showing a 0.6% decrease YoY.

- Inland Empire: Average asking rents reached $1.82 per square foot (NNN), up 1.1% QoQ and 2.8% YoY.

- Orange County: Asking rents averaged $2.46 per square foot (NNN), reflecting a 0.4% increase QoQ and YoY.

- Ventura County: Average asking rents were $2.18 per square foot (NNN), up 1.9% QoQ and 1.4% YoY.

Southern California’s office market, for the past several years, has witnessed the accumulation of vacant office space, driven by the evolving landscape of remote work and space utilization strategies.

This shift in tenant priorities is reflected in insights shared by Michael Arnold, Executive Vice President and Founder of the Tenant Consulting Group at NAI Capital Commercial. Drawing from his tenant consultations, Michael emphasizes that tenants will continue to seek “flights to quality” in assets, with amenity-rich properties playing a critical role in real estate decision-making processes. As companies reevaluate their workplace strategies, the “hub and spoke” model appears to be fading, with most firms now seeking a minimum of 3–4-day work weeks. Many of the companies his team is consulting with remain uncertain about their long-term business outlook over the next 5–10 years, which is why they are incorporating flexibility into their leases.

He adds: “Tenants with a clear vision or direction for their business will undoubtedly benefit from the distress in the market.” Landlords continue to offer significant concessions, though they may not openly “advertise” them. By navigating these opportunities, tenants can achieve the best outcomes in today’s office market.

While tenants navigate current market challenges, landlords and submarkets are responding differently. Tina LaMonica, SIOR, Executive Vice President of NAI Capital Commercial in the Pasadena office, highlights that the market is poised for a slow recovery. “As businesses continue to incentivize employees to come in, we may see more people in the office,” she notes. Landlords remain wary of adjusting asking rents, instead focusing on leasing incentives and concessions for tenants in response to shifting market conditions and tenant preferences as rental rates stabilize.

Looking ahead to 2025, Tina expects certain submarkets to outperform others. Known for its proximity to amenities and availability of quality office space, “Century City will continue to do well, while DTLA will experience a very slow recovery due to its history of high vacancy. Suburban markets are likely to recover faster than DTLA.” The most significant challenges, according to Tina, include companies downsizing and relocating out of state, which could further hinder the office market’s recovery.

Meanwhile, in the Hollywood market—a hub for the media and entertainment industry—Vice President Jared Swedelson of NAI Capital Commercial sees a nuanced picture of recovery and opportunity. He explains, “While the media and entertainment sector has historically been the backbone of the Hollywood office market, the prolonged strikes of 2023–2024, coupled with shifting content creation trends that prioritize ‘quality over quantity,’ have left a significant impact. Many production companies have scaled back expansion plans or downsized, creating a ripple effect on leasing demand.”

Hybrid work trends further complicate recovery, as tenants continue to downsize their footprints while seeking high-quality, flexible office spaces. Vacancy rates remain elevated, particularly among traditional and older properties. However, there is growing optimism for a rebound, with the media and entertainment sector regaining momentum and other industries—such as fitness studios and design firms—showing increased interest in repurposed creative spaces traditionally dominated by entertainment tenants.

In contrast to Hollywood’s entertainment-driven dynamics, Orange County offers a relatively stable outlook for its office market in 2025. Brian Childs, Executive Managing Director of NAI Capital Commercial’s Orange County office, notes that limited new office construction and continued conversions away from office use have created positive net absorption, offsetting the challenges of the post-COVID leasing environment. “Office lease rates and vacancies will remain static in 2025,” he explains. “There is limited new office construction and continued conversion away from office use, creating positive net absorption in the office sector. This lack of construction and reduction in the overall office base offsets any office leasing hangover post-COVID. We are looking at a fairly balanced office market moving forward.”

Brian highlights specific submarkets he expects to outperform due to limited availability: “Smaller suburban markets such as Newport Center, Brea, Cypress, and San Clemente will lead the way. Conversely, submarkets with larger concentrations of available Class A office space—such as the Airport Area, Costa Mesa, South Santa Ana, and Orange—will continue to fight for positive absorption.”

As for challenges and opportunities, Brian notes that the high cost of tenant improvement construction remains a significant obstacle for owners in competitive office markets. However, he also sees opportunities for tenants with flexible requirements: “The high cost of tenant improvement construction will create challenges for owners, but it provides opportunities for tenants willing to adapt to available space.”

Looking forward, these dynamics suggest that Orange County’s office market will continue to evolve as landlords and tenants adapt to the post-pandemic realities of hybrid work and shifting space needs.

As Southern California’s office market continues to adapt to post-pandemic realities, tenant behavior, submarket strengths, and landlord strategies will define the trajectory of recovery in 2025.

Office Real Estate Vacancy

- Los Angeles County: The office market, with 398,274,890 rentable square feet, recorded a 17.0% vacancy rate, reflecting a 0.3% quarter-over-quarter (QoQ) increase and a 4.5% year-over-year (YoY) rise in vacant space.

- Orange County: Out of 157,182,672 rentable square feet, the vacancy rate held steady at 12.6% QoQ, reflecting a 6.1% YoY decrease in vacant space.

- Inland Empire: With 65,968,687 rentable square feet, the vacancy rate was 5.5%, while vacant space increased by 3.0% QoQ but decreased by 5.9% YoY.

- Ventura County: The office market, with 29,463,421 rentable square feet, posted an 11.7% vacancy rate, reflecting a 1.8% QoQ decrease and a 1.2% YoY decline in vacant space.

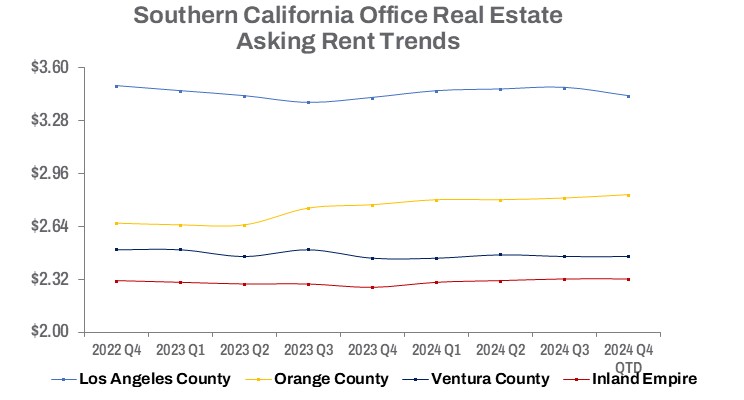

Office Real Estate Rents

- Los Angeles County: Average asking rents were $3.43 per square foot (FSG), reflecting a 1.4% decrease QoQ and 0.3% YoY.

- Orange County: Asking rents averaged $2.83 per square foot (FSG), reflecting a 0.7% QoQ increase and a 2.2% YoY rise.

- Inland Empire: Average asking rents were $2.31 per square foot (FSG), down 0.4% QoQ but up 1.8% YoY.

- Ventura County: Asking rents remained steady at $2.46 per square foot (FSG), with no change QoQ or YoY.

As Southern California’s commercial real estate market stabilizes heading into 2025, vacancy rates have likely peaked, and rents are nearing their troughs across key sectors, positioning the market for a balanced recovery. The industrial market has loosened, driven by new construction and natural attrition, but the outlook remains stable for long-term demand as businesses continue to expand. In multifamily, while vacancy rates fluctuate due to economic conditions, including rent fatigue and government overregulation, investor demand remains strong, particularly in high-demand areas.

Retail vacancies and rents have been impacted by shifting consumer behaviors and retailer bankruptcies, but demand is increasingly focused on smaller, more efficient retail spaces, creating opportunities for agile businesses. Meanwhile, the office sector is gradually adjusting, with vacancies steadily declining as occupiers refine their hybrid work models, setting the stage for a more sustainable office market.

Looking ahead, the Southern California market appears poised for a recovery driven by adaptive strategies and evolving demand across sectors. The trends highlighted in these key charts and insights reveal a region in transition, responding to economic pressures and changing market dynamics. While challenges persist, the opportunities in 2025 are expected to outweigh them, positioning the region for a stable and balanced recovery.