Tenants Gain Leverage in L.A. Office Market, Sublessors and Landlords Compete with Rent Concessions

Record High Sublease Availability Drives Rent Reductions, Outpacing Direct Space Market Growth

MARKET OVERVIEW

The L.A. County office market’s recovery is hindered by weak demand, unoccupied new construction a, and continuous rise in vacant space. Landlords, wary of adjusting asking rents despite elevated vacancy rates, face challenges in spurring occupancy. In Q2, 30.2% of completed office construction added to the inventory since 2020 remains vacant. Additionally, the market grapples with a significant influx of sublease office spaces.

The evolving landscape of remote work and space utilization strategies drives a constant accumulation of vacant office space. This quarter’s increasing vacancy rates propelled the overall vacancy rate up by 150 bps compared to the previous year, reaching 16.9%. Since January 2024, the market has added close to 2.4 million square feet of vacant space, with 30% of that being offered for sublease, culminating in a record high of 66.7 million square feet of vacant office space. Remarkably, vacancy has consecutively increased each quarter since Q2 2020 at the start of the pandemic, rising 62%. The amount of vacant space on the market remains well above the peak reached during the Great Recession. Vacant sublease space has accumulated, experiencing the addition of approximately 300,000 square feet on average each quarter over the past two years, reaching 7.6 million square feet this quarter—surpassing levels not seen since the Dot-Com Bust.

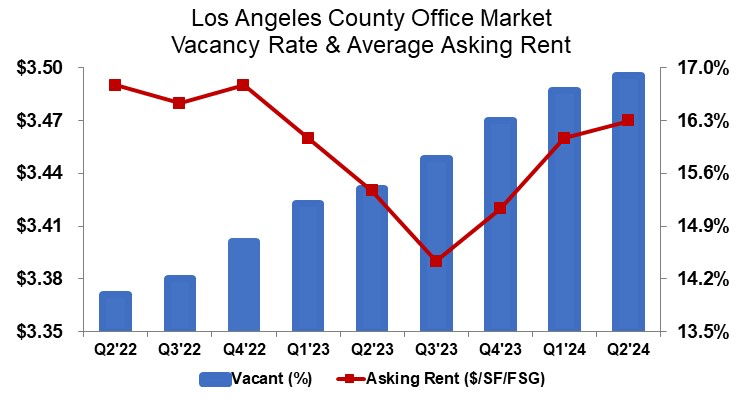

Los Angeles County Office Market Q2 2024 Statistics:

Despite the record level of space coming onto the market year over year, asking rents on a direct basis remain stubbornly elevated, flat from last year at $3.47/SF on a full-service gross basis. Leasing volume for the first half of this year is down 16.1% compared to the first half of 2023 and down 18.5% quarter over quarter, indicating that leasing volumes remain on a downward trend, possibly approaching a trough. The pressure remains on landlords to offer concessions, such as lower rents, free rent, and flexible term commitments.

TRENDS TO WATCH

While the surge in available office space is driven by the evolving landscape of remote work and space utilization strategies, office demand will require lower rents to drive occupancy. Tenants continue to have leverage in negotiating favorable deals. The abundance of office space will compel landlords and sublessors to meet tenant demands.

With available sublease space at an all-time high, sublessors are beginning to drop rents. The average asking rent for sublease spaces has started a noticeable descent, with the average rent in Q2 dropping by 5.8% from the previous year to $2.95/SF full-service gross, down 2.6% from Q1 2024. The rate at which sublease space has come on the market, increasing by 5.6% quarter-over-quarter, has outpaced direct space, which only increased by 0.5% over the prior quarter.

In the Central submarket, which includes LA’s tallest office buildings in Downtown, the average sublease rent in Q2 dropped by 13.6% from the previous year to $2.99/SF full-service gross, down 3.4% from Q1 2024. In the West submarket, which holds more than a third of all the sublease space in the region, the average sublease rent in Q2 dropped by 3.3% from the previous quarter to $4.36/SF full-service gross. This is a surprising 1.4% increase from last year due to more expensive sublease space coming on the market over the last year, pushing up the average, as the West—home to Silicon Beach—commands higher rents in the region.

Sublessors actively seeking to fill their excess office space will offer significant rent concessions, competing with landlords for a shrinking pool of active tenants in the market. Currently, in this market, tenants pursuing office space hold the advantage, while landlords actively strive to uphold property values. These factors drive the dynamics in the office market.