The Owner-User Edge in the ‘One Big Beautiful Bill’ Is Driving SoCal’s Office Recovery

One Year After the One Big Beautiful Bill, Owner-Users Are Driving Southern California’s Office Recovery

As investors continue to navigate leasing risk and elevated vacancies, private businesses are capitalizing on repriced assets and favorable tax treatment.

Owner-user office acquisition volume jumped 67.8% year over year in Q1 2026, outpacing the broader market.

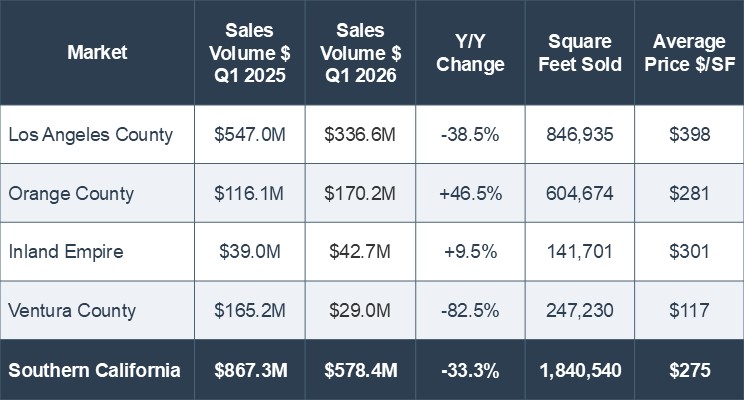

Southern California’s office market remains one of the most challenged asset classes in commercial real estate. In Q1 2026, total sales volume reached $578.4 million across 1.84 million square feet sold, down 33.3% and 31.9% year over year, respectively. Buyers and sellers continue to navigate elevated vacancies, remote work normalization, and a prolonged repricing cycle that has reset office valuations across the region.

Average pricing across Southern California declined 16.6% year over year to $275 per square foot, underscoring how significantly asset values have reset from peak levels. Ventura County experienced some of the sharpest weakness in the region, with dollar volume falling 82.0% year over year to $29.0 million and average pricing declining to $117 per square foot. However, the results were heavily influenced by the sale of a 209,404-square-foot high-vacancy office property that was originally constructed as an industrial building and later converted to office when it made economic sense. The asset sold to a developer for approximately $19 million, or $91 per square foot. Excluding that transaction, Ventura County sales volume would have declined 93.8% year over year to approximately $10 million, while average pricing would have recalculated to $264 per square foot, representing a 31.7% year-over-year decline. Orange County offered a rare counterpoint, with dollar volume rising 46.5% year over year to $170.2 million, suggesting select submarkets are finding a clearing price that is bringing buyers back to the table.

Yet beneath this broad reset, a more nuanced trend is emerging. Office may be the worst-performing major commercial real estate asset class, but within the distress, a distinct demand driver is gaining momentum. Rather than institutional capital pursuing yield, private businesses are increasingly acquiring office properties to secure occupancy, operational control, and the improved after-tax economics created by the One Big Beautiful Bill Act. The divergence between investors and owner-users is where the market’s most consequential shift is taking place.

Market Trends: Bonus Depreciation Fuels an Owner-User-Led Recovery

The return of 100% bonus depreciation under the One Big Beautiful Bill, enacted July 4, 2025, is approaching its one-year anniversary with early signs of meaningful impact on Southern California’s office market. With Independence Day 2026 just weeks away, the evidence suggests the legislation is beginning to deliver on its promise for private businesses, as owner-users have emerged as an increasingly active buyer group even as investors remain selective.

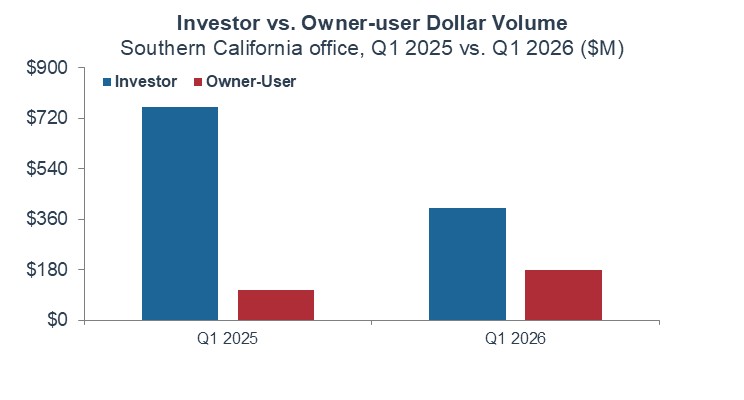

While investors remained cautious during the first quarter, the rate of owner-user acquisitions accelerated as improved tax treatment enhanced the economics of ownership. The result is a market increasingly defined by two distinct buyer groups pursuing very different strategies.

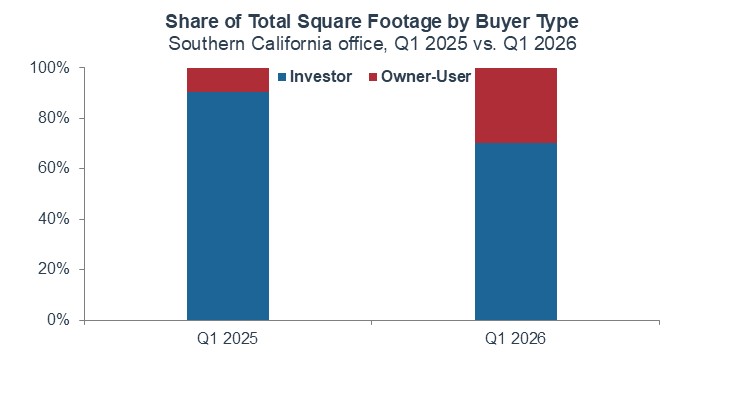

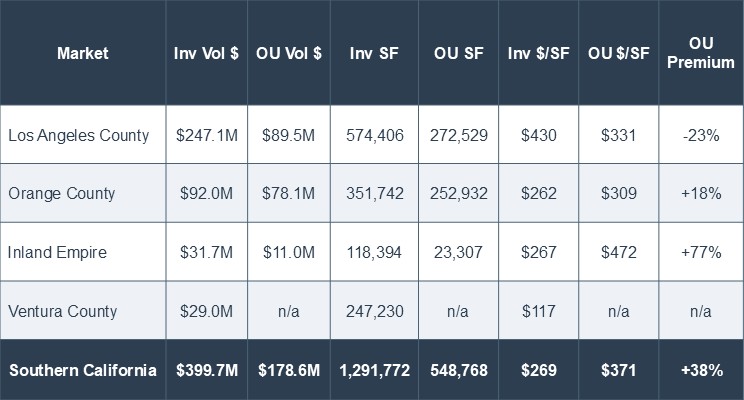

Investor sales volume totaled $399.7 million in Q1 2026, down 47.5% from $760.9 million a year prior, on 1.29 million square feet sold. Owner-user sales volume reached $178.6 million, up 67.8% from $106.4 million over the same period, on 548,768 square feet sold. Owner-users accounted for nearly 30% of total square footage traded in Q1 2026, up from approximately 10% a year prior, while investors declined from roughly 90% to 70% of total market activity over the same period. The shift reflects a meaningful compositional change in who is buying Southern California office, even as investors retained the majority of square footage traded.

The divergence was particularly pronounced in Los Angeles County, where investor sales volume fell 51.0% year over year while owner-user volume surged 109.2%. Orange County posted gains for both buyer groups, though owner-user activity continued to outpace investor demand on a relative basis.

The differing motivations of each buyer pool help explain the trend. Investors continue to evaluate office assets through the lens of leasing risk, elevated vacancies, refinancing challenges, and uncertain long-term demand. Owner-users, by contrast, are focused on occupancy costs, operational control, long-term space certainty, and tax advantages, a fundamentally different calculus.

The restoration of 100% bonus depreciation may be particularly impactful for owner-users because it allows qualifying improvements and building components to be expensed immediately, reducing after-tax ownership costs. Combined with SBA or conventional financing and repriced office valuations, the incentive to purchase rather than lease has become increasingly attractive for many private businesses.

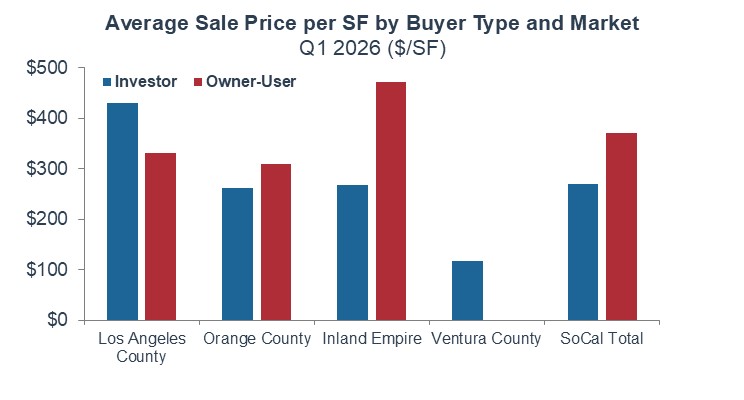

Transaction metrics reinforce this shift. Across Southern California, owner-users paid an average of $371 per square foot compared with $269 per square foot for investors, a 38% premium that reflects both the typical size-price relationship in office markets and the current cycle, in which cautious investors are underwriting to yield while owner-users are pricing to occupancy value, operational needs, and favorable tax treatment.

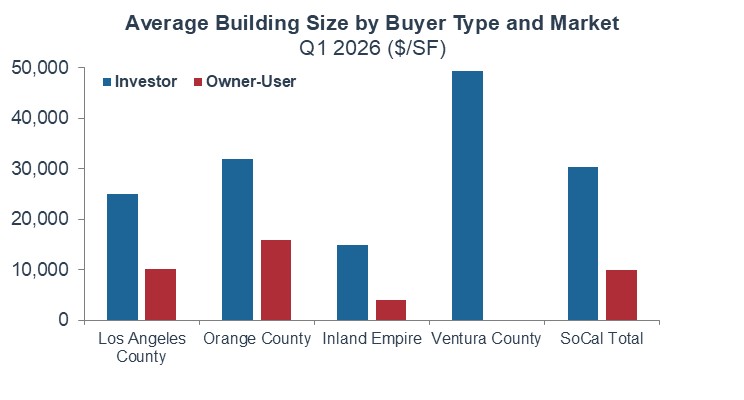

The Inland Empire offers one of the clearest illustrations. Owner-users acquired buildings averaging 3,885 square feet at $472 per square foot, while investors purchased significantly larger properties averaging 14,799 square feet at $267 per square foot. The combination of a 3.8-times size differential and a 77% pricing premium underscores the degree to which private businesses are willing to pay for occupancy-driven benefits.

Investor activity, meanwhile, remains concentrated in a smaller pool of higher-quality opportunities. Los Angeles County illustrates this dynamic clearly, where investors averaged $430 per square foot compared with $331 for owner-users, reflecting selective acquisition of higher-quality assets in premier submarkets rather than broad market re-entry. Although average pricing increased in some markets, declining transaction volume and smaller average deal sizes reinforce that investors are remaining highly selective rather than broadly re-entering the market.

No owner-user transactions were identified in Ventura County in Q1 2026, consistent with a thin-liquidity market confined to institutional-scale investor trades. As repriced inventory continues to absorb and private businesses grow more familiar with the tax benefits available under the One Big Beautiful Bill, owner-user demand may re-emerge gradually in the county.

Southern California’s office market remains challenged, but owner-users are currently driving the recovery in transaction momentum, even as investors retain the majority of dollar volume traded. Whether investors return in greater numbers will likely depend on stabilizing vacancy rates and improved visibility into leasing fundamentals. Until then, private businesses acquiring space for their own operations may remain the market’s most reliable source of transaction growth, gradually absorbing repriced inventory one building at a time.