First Quarter 2025

Ventura County Office Market in Transition as Leasing and Sales Momentum Builds

Leasing volume doubles quarter over quarter, sublease rents remain attractive, and buyers target lower-priced assets.

This shift toward opportunity-driven acquisitions is expected to persist, reflecting evolving investor preferences in response to current economic conditions.

MARKET OVERVIEW

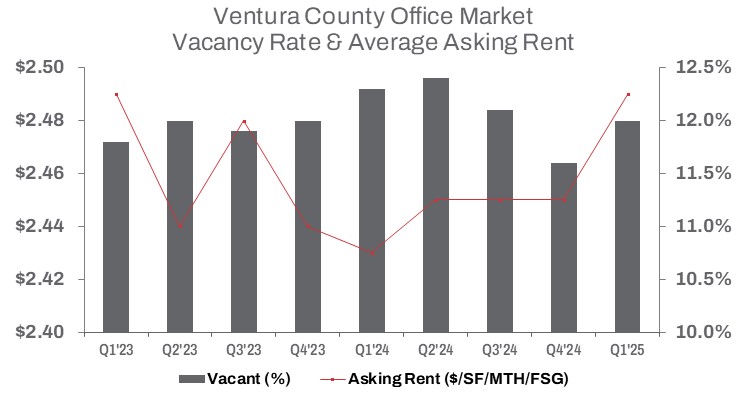

The Ventura County office market’s recovery continues, though challenges remain in boosting occupancy levels. Sublessors and landlords, responding to subdued demand and elevated vacancy rates, have adjusted asking rents—a strategy that has begun to yield positive results. In Q1 2025, vacant office inventory declined by 103,815 square feet compared to Q1 2024, suggesting the market is hovering near the bottom of this cycle, with occupancy fluctuating quarter to quarter.

Year over year, vacant direct office space decreased by approximately 1.6%, while sublease space dropped by 10.8%, signaling gradual progress toward pre-pandemic occupancy levels. Sublease asking rents fell sharply by 6.5% from last year, while direct space rents strengthened, rising by $0.06 to $2.47 per square foot on a full-service gross basis over the same period.

Vacancy rates trended downward from this time last year, with the overall rate falling 30 basis points to 12.0%. This marks a shift in the trajectory of vacant office space, driven by evolving dynamics around remote work and space utilization strategies. Leasing volume has picked up, increasing 31.6% year over year and more than doubling from the previous quarter.

Since Q1 2021, when the market was grappling with the fallout of pandemic-driven disruptions, direct vacant office space has decreased by just 29,957 square feet. While vacant sublease space remains 144,592 square feet above Q1 2021 levels, it has seesawed for several quarters as tenants take advantage of sublease opportunities offered by motivated sublessors with competitive terms to offload excess space.

TRENDS TO WATCH

Tenants seeking value will find opportunities in buildings with vacant sublease space. As we move into the second half of 2025, subleasing activity in Ventura County remains steady, with tenants subleasing 20,636 square feet in Q1 2025—bringing the year-over-year total to 85,116 square feet, a 56.6% increase compared to the same period in 2021. However, the pace at which tenants offload excess square footage is expected to ebb and flow in the coming months.

While the region still has a significant amount of available sublease space, inventory is gradually shrinking. Sublease availability rose 17.1% quarter over quarter but declined 13.4% year over year. This trend is especially apparent in the East submarket, where available sublease space increased to 529,431 square feet—up quarter over quarter, but down 10.0% from the same time last year.

Looking ahead, sublease activity will continue to present cost-saving opportunities. The average asking rent for sublease space in Ventura County stood at $2.17 per square foot—11.7% ($0.32) lower than direct space—positioning tenants to secure favorable deals in the quarters to come. As landlords remain cautious and limit concessions to protect rental income, competition from sublessors is likely to drive further rent adjustments and deal incentives.

On the sales side, 2025 began with a notable shift in market dynamics. Total square footage sold jumped from just 41,228 square feet in Q4 2024 to 536,085 square feet in Q1 2025.

A standout transaction this quarter was the investment acquisition of the Westlake Village City Center – West Building at 31111 Agoura Road. Westlake Village Corporate Center LLC purchased the 64,146-square-foot office building from Pacifica Westlake Village LP for $7.5 million, or approximately $117 per square foot. At the time of sale, the property was only about 38% occupied. The buyer was drawn to the asset’s pricing and long-term upside potential.

Meanwhile, the average sale price across the market rose 6.8% to $319 per square foot—though still 18.5% below year-ago levels, as buyers and sellers continue to adjust expectations to get deals done.

This shift toward opportunity-driven acquisitions is expected to persist, reflecting evolving investor preferences in response to current economic conditions. The rise in both sales volume and average sale price points to a market in transition—one in which investors remain selective, refining acquisition strategies while awaiting more favorable conditions. These trends signal a continued period of adjustment, with both investors and tenants adapting to a changing landscape in the months ahead.