What the Fed’s Year-End Rate Cut Means for CRE Pricing and Deal Flow in 2026

Federal Reserve Delivers Year-End Rate Cut as Los Angeles County CRE to Enter 2026 in Reset Mode

Lower debt costs are expected to steady valuations after three years of volatility, with Industrial and Retail leading early momentum as easing rates support broader stabilization across asset classes.

The Fed’s year-end rate cut provides a welcome boost, helping stabilize pricing and revive deal flow heading into 2026.

Managing Director of Research and Public Relations at NAI Capital Commercial

The Federal Reserve officially cut interest rates by 25 basis points at its final meeting of 2025, lowering the federal funds rate to 3.50%–3.75%. This marks the third consecutive cut this year and reinforces the shift toward easier monetary policy as the central bank works to balance a cooling labor market and slow-moving inflation.

For Los Angeles County’s commercial real estate markets—already navigating three years of pricing adjustments and compressed deal activity—the cut brings welcome relief entering 2026. Reduced borrowing costs are expected to help stabilize valuations, narrow bid-ask spreads, and gradually revive investment momentum across asset classes.

The market sentiment shift is immediate. When asked about the impact of the Fed’s series of rate cuts, including this final one for the year, Chris Jackson, CEO of NAI Capital Commercial, shared his outlook after considering the following question: As borrowing costs begin to ease following the Fed’s year-end rate cut, how do you see investor sentiment, pricing expectations, and transaction activity evolving across the investment sales market in 2026?

Chris commented, “The investment market has heated up, and they are looking for investment opportunities again. I expect to see cap rates drop a little and activity continue to rise.”

How We Got Here After Three Years of Volatility

-

March 2022–July 2023: The Fed raised interest rates 11 times, bringing the benchmark rate to 5.25%–5.50% to fight the 40-year inflation peak of 9.1%.

-

Late 2024: The Fed reversed course, cutting rates in September (-50 bps), November (-25 bps), and December (-25 bps).

-

2025: Additional cuts in September and October brought rates to 3.75%–4.00%.

-

December 2025: The latest -25 bps cut lowered the rate to 3.50%–3.75%, despite delayed federal economic data caused by the record-long government shutdown

The move signals the Fed’s commitment to supporting labor market stability while acknowledging that inflation progress has stalled. Since 2022, the Federal Reserve’s rate hikes have significantly impacted commercial real estate markets in Los Angeles County.

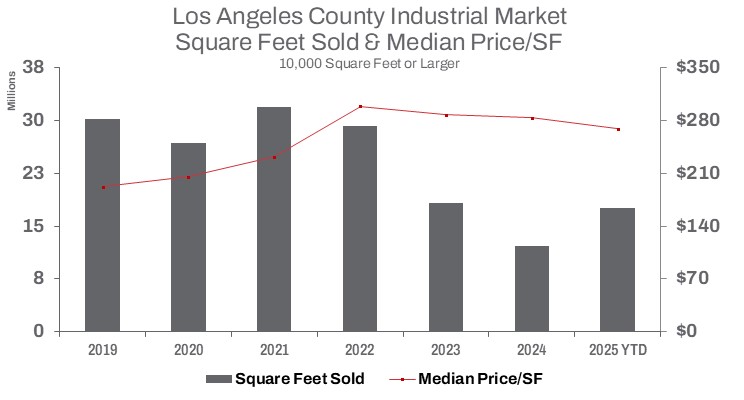

INDUSTRIAL

Los Angeles County Industrial Market (10,000 Square Feet or Larger)

Sales activity rebounds, though pricing continues to reset.

- Square Feet Sold YTD: 17.8M SF (+44.1% from 2024)

- Median Price/SF: $269 (-5.2% from 2024)

- Since 2022: Sale Volume -39.9%, Pricing -10.1%

Impact of the rate cut: Improved borrowing conditions should bolster both user demand and investor underwriting. Expect more transactions to clear in 2026 as financing becomes more accessible and cap rates stabilize.

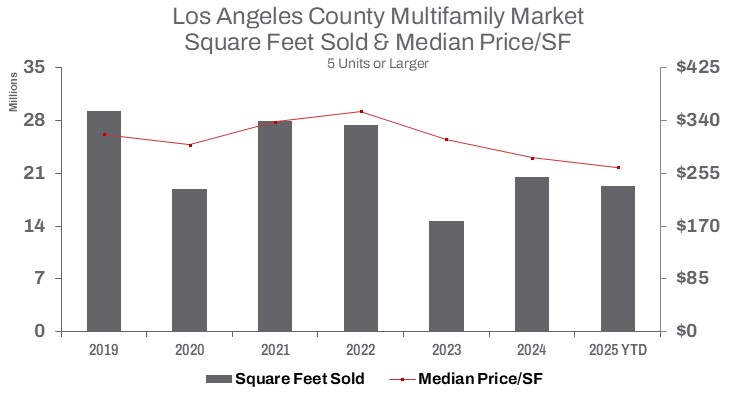

MULTIFAMILY

Los Angeles County Multifamily Market (5 Units or Larger)

Investors remain cautious as higher operating expenses and regulations weigh on values.

- Square Feet Sold YTD: 19.3M SF (-6.2% from 2024)

- Median Price/SF: $265 (-5.4% from 2024)

- Since 2022: Sale Volume -29.5%, Pricing -25.2%

Impact of the rate cut: As the most rate-sensitive sector, multifamily may experience a gradual thaw. Lower debt service costs could help narrow the pricing gap between buyers and sellers, while easing refinancing challenges for existing owners.

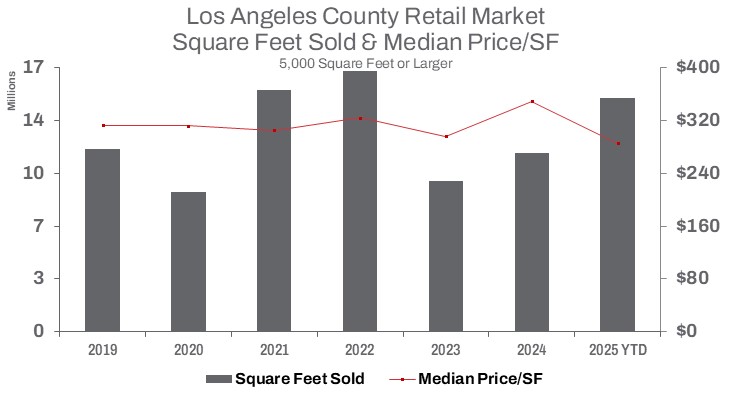

RETAIL

Los Angeles County Retail Market (5,000 Square Feet or Larger)

Transaction volume surges, driven by a deep price correction.

- Square Feet Sold YTD: 15M SF (+30.3% from 2024)

- Median Price/SF: $286 (-18.1% from 2024)

- Since 2022: Sale Volume -10.6%, Pricing -11.8%

Impact of the rate cut: Retail continues to show resilience, bolstered by tenant stability and consumer spending. Improved financing terms following the cut may draw additional investors into neighborhood centers, value-oriented retail, and well-located freestanding assets.

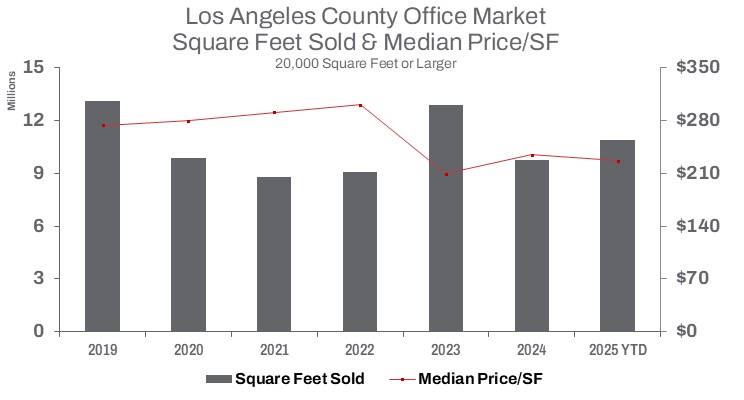

OFFICE

Los Angeles County Office Market (20,000 Square Feet or Larger)

Sales volume edges higher, but pricing remains under significant downward pressure.

- Square Feet Sold YTD: 10.9M SF (+11.5% from 2024)

- Median Price/SF: $227 (-3.3% from 2024)

- Since 2022: Sale Volume +20.3%, Pricing -24.6%

Impact of the rate cut: Office continues to face the most structural challenges, but lower rates offer modest relief to owners confronting refinancing deadlines and rising operating costs. Stabilized assets in strong submarkets are likely to see the most benefit heading into 2026.

What This Rate Cut Means for CRE Investors

The December rate cut is expected to:

✔ Lower borrowing costs for acquisitions, construction loans, and refinancing

✔ Improve cap rate stability after three years of upward movement

✔ Increase liquidity and transaction volume, particularly in Industrial and Retail

✔ Support pricing stabilization in 2026 after widespread corrections

✔ Encourage capital deployment from investors who have been waiting on the sidelines

While today’s cut provides momentum going into the new year, the Fed signaled it may pause further cuts in early 2026 until labor and inflation data become more reliable.

Crucially, the Fed’s decision provides a critical opportunity for lenders to restructure deals and widen the pool of financeable projects. Kyle Nagy, President of NAI CommCap Advisors, points out, “The rate cut could ease debt service pressure and widen the pool of financeable projects in 2026. With lower rates, lenders can offer better leverage, potentially interest only payments, and more favorable debt structures.”

Bottom Line: With the latest rate cut now in effect, Los Angeles County’s commercial real estate market enters 2026 on firmer footing. Pricing across all major sectors continues to adjust, but improved financing conditions offer a critical tailwind for investors, owners, and lenders following three years of volatility. Momentum is expected to build gradually, with Industrial and Retail leading activity and Multifamily and Office gaining stability as debt markets normalize.