Third Quarter 2024

Inland Empire Retail Market Shows Mixed Progress as Vacancy Rates Edge Up

Investor Demand Drives 30% Increase in Average Deal Size, Reflecting Retail Market’s Adaptation to Economic Shifts.

While retail space absorption continues to face challenges, it has surpassed pre-pandemic occupied space levels.

MARKET OVERVIEW

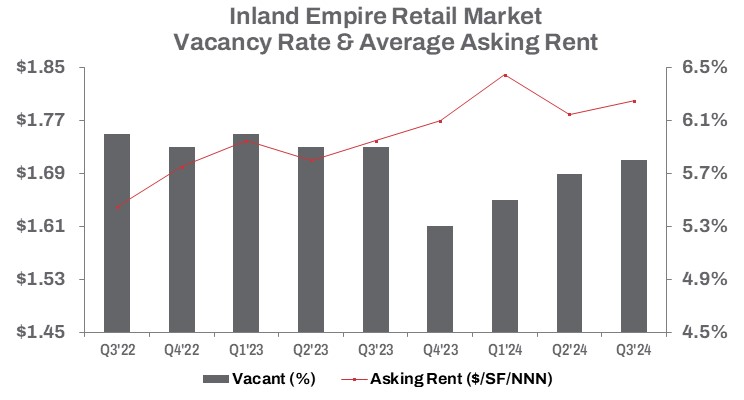

The Inland Empire retail market continues to show mixed progress as it nears its fourth year post-pandemic. In Q3 2024, the sector saw a slight increase in vacancy rates, edging up to 5.8%, a 10-basis-point rise quarter-over-quarter and 10 basis points higher compared to the same period last year. Leasing volume experienced a notable 23.9% decrease quarter-over-quarter, though it remained positive year-to-date, up 5.7% from 2023, totaling 2.4 million square feet.

A wave of bankruptcies among major retail chains—including 99 Cents Only Stores, Rite Aid, Big Lots, and The Franchise Group Inc. (owners of The Vitamin Shoppe, Pet Supplies Plus, and Buddy’s Home Furnishings)—has further strained the market. These closures, driven by declining revenues and escalating supply chain and labor costs, have become more frequent.

Adding to these pressures, California’s new $20/hour minimum wage for fast-food workers, implemented on April 1, 2024, has intensified challenges for retailers. The wage hike, which represents an 18% increase in average hourly pay, comes with annual increases capped at the lesser of 3.5% or the U.S. CPI for Urban Wage Earners. The California Fast Food Council has indicated its intention to seek a 3.5% increase in 2025. The law that created the panel allows for adjustments to the pay level once a year.

While retail space absorption continues to face challenges, it has surpassed pre-pandemic occupied space levels by over 4.1 million square feet since Q2 2020. Total vacant retail space, though still elevated, stood just below 8.9 million square feet in Q3 2024. This reflects the sector’s ongoing struggle to adapt to post-pandemic consumer behavior and evolving economic conditions. High inflation and stiff competition have dampened consumer spending at retail chains.

Big Lots’ bankruptcy in September 2024 will result in hundreds of store closures nationwide, including locations in the High Desert submarket’s Apple Valley and Hesperia, as well as Murrieta within the South Inland Empire submarket. Big Lots joins other retailers, such as Red Lobster, Rite Aid, and Bed Bath & Beyond, in a growing list of companies filing for bankruptcy. According to CoreSight Research, U.S. retailers have announced more than 7,100 store closures through November 2024—a staggering 69% increase compared to the same period in 2023.

The challenging economic environment, compounded by rising costs and the ongoing cost-of-living crisis, leaves the Inland Empire retail market facing uncertain challenges.

TRENDS TO WATCH

As the economy evolves, demand for retail space continues to shift. Despite challenges, investor interest in prime locations remains strong. In Q3 2024, the average sale price for retail space decreased to $306 per square foot, down from $345 per square foot in the previous quarter. This decline was partially driven by the August 20, 2024, sale of the Promenade Temecula by Seritage Growth Properties to AXS Opportunity Fund LLC. The 118,520-square-foot regional mall sold for $24 million, equating to $202.50 per square foot.

Fueling market activity, the average asking rent for direct space rose by 3.4% year-over-year, helping to narrow the gap between asking and bid prices. Sales volume, measured on a square footage basis, increased by 30.7% year-to-date compared to the prior year, reflecting heightened activity in retail property transactions as investors seize opportunities.

Retail building sales, buoyed by the ongoing recovery of brick-and-mortar leasing, recorded more than $568 million in year-to-date sales volume— up 32.0% from the 2020 pandemic low but 8.3% below the same period last year. The retail sector continues to face hurdles in returning to ‘normal’ levels, with divergent trends between sales and leasing. The median sale price per square foot rose 3.4% quarter-over-quarter and 0.5% year-over-year, reaching $294 in Q3, reflecting a stabilizing and rebalancing sales environment.

Despite elevated borrowing costs, price adjustments driven by investor demand led to a 30.0% quarter-over-quarter increase in the average deal size, which reached $3,266,500 in Q3 2024. In comparison, the average deal size in Q3 2020 was 43.9% lower, at $1,832,566, with a median sale price per square foot of $258. These figures suggest that the retail sales market is adapting to shifting economic conditions.

The collapse of the Kroger-Albertsons merger, which would have been the largest U.S. supermarket merger in history, has eliminated a significant potential market disruption. As new economic challenges emerge, demand for retail space hangs in the balance. Investors are making strategic acquisitions of prime real estate, prioritizing the transformation of outdated spaces into dynamic community hubs that align with the evolving needs of today’s consumers. This focus will drive organic growth over time, while the backfilling of vacant retail spaces helps sustain stable occupancy levels.