First Quarter 2025

Orange County Retail Market Shows Signs of Recovery Despite Mixed Leasing Trends in Q1 2025

Vacancy declined and investment surged, helping offset a drop in leasing activity, as momentum strengthened in the Central and North submarkets.

The retail market will continue adjusting rents to backfill vacant spaces.

MARKET OVERVIEW

While the broader economy remains steady, Orange County’s retail market continues to navigate ongoing challenges. Demand for space has created mixed but generally positive trends, with excess inventory gradually being absorbed.

Retail bankruptcies in 2024 led to the closure of several well-known chains; however, some retailers seized the opportunity to secure prime locations. As a result, net absorption increased by 56,858 square feet quarter-over-quarter, adding 195,067 square feet since Q1 2024. Total vacant space declined from its Q4 2020 peak, beginning 2025 with approximately 5.6 million square feet—an encouraging sign of gradual recovery since the pandemic.

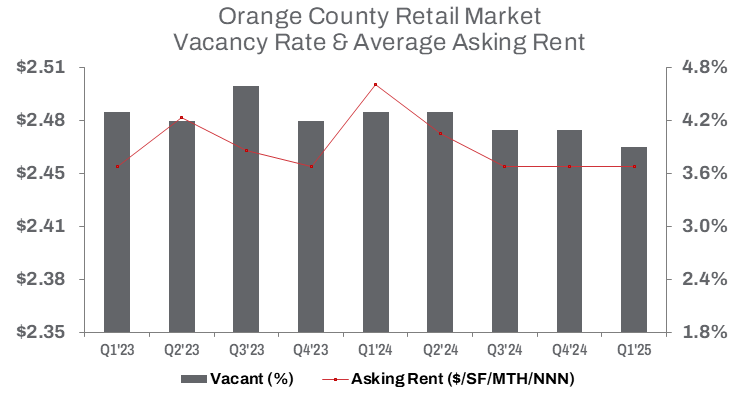

Despite modest occupancy gains, landlords continued to offer concessions, and asking rents remained flat quarter-over-quarter at $2.45 per square foot triple net, down 2.0% year-over-year. Investor activity picked up sharply, driving the average retail sale price up 11.0% from the previous quarter to $514 per square foot. Key transactions included:

Blackstone’s acquisition of Retail Opportunity Investments Corp. for $4 billion, encompassing 419 properties nationally—32 of which were located in Orange County, totaling 916,637 square feet.

PGIM’s purchase of DJM Capital Partners’ interest in Bella Terra, a 1.77 million-square-foot lifestyle center in Huntington Beach, which also includes the 467-unit Residences at Bella Terra.

These transactions helped fuel a surge in investment activity, with retail square footage sold during Q1 surpassing 2.2 million square feet—more than four times the volume from the previous quarter and more than double the total from Q1 2024.

Leasing activity was mixed, declining 19.8% quarter-over-quarter. However, renewals and sublease deals helped stabilize the vacancy rate. Year-over-year leasing volume rose 28.0%, signaling continued demand.

TRENDS TO WATCH

The retail market will continue adjusting rents to backfill vacant spaces, with mixed results across the region as retailers seek prime locations in densely populated areas.

In Central Orange County—home to Disneyland and the county’s most tourism-driven retail market—vacant retail space is the lowest in the region, totaling just 769,297 square feet. The submarket recorded 59,443 square feet of positive net absorption in Q1 2025, a sharp turnaround from negative 48,961 square feet in Q4 2024 and negative 41,466 square feet in Q1 2024. Direct asking rents rose 3.9% quarter-over-quarter and 7.1% year-over-year to $2.40 per square foot triple net. Renewed interest has driven competition among tenants, contributing to rising rents.

In North Orange County—home to Knott’s Berry Farm and another major tourism-retail destination—vacant space declined at the fastest rate in the region. The submarket posted 64,720 square feet of positive net absorption in Q1 2025, building on 41,103 square feet in Q4 2024 and rebounding from negative 113,089 square feet in Q1 2024. Direct asking rents increased 2.3% quarter-over-quarter and 1.8% year-over-year to $2.25 per square foot triple net—the lowest in Orange County. Like Central Orange County, the North submarket is experiencing rising tenant demand and growing rent pressure.

In contrast, South Orange County—anchored by the Irvine Spectrum Center and nearby new housing developments—has the highest vacant retail space in the region, totaling approximately 1.5 million square feet. The submarket recorded 51,381 square feet of negative net absorption in Q1 2025, a steeper decline than the 16,464 square feet lost in Q4 2024 and 7,392 square feet in Q1 2024. Direct asking rents fell 2.2% quarter-over-quarter and 9.5% year-over-year to $2.68 per square foot triple net. Weaker tenant demand has weighed on rents, in contrast to the more competitive conditions in the Central and North submarkets.

As competition for prime retail space remains strong in key areas, market volatility is likely to persist. Landlords, tenants, and investors will continue to compete aggressively for well-positioned properties as the sector advances in its recovery.